Apr 30, 2025

A 2026 Audit Checklist for FinTech & Regulated Teams

By Fraxtional LLC

Summarize the blog with AI

For many FinTech and regulated teams, audits still feel episodic. Reactive to a notice and followed by patching gaps. This approach no longer works.

Audits now come from multiple directions: regulators, sponsor banks, investors, and strategic partners. Each audit reflects not just compliance, but how well leadership manages risk. A clean audit signals control; repeated findings signal weakness.

This guide lays out a practical, leadership-focused audit checklist for 2026. It explains what regulated teams should review, why each area matters, and how strong audit preparation reduces friction long before an audit begins.

Quick Glance

- An audit checklist should test control performance, not document existence. Auditors care whether controls operate consistently, not whether policies are filed correctly.

- Risk changes faster than checklists. New products, partners, and geographies require audit checklists to evolve with the business.

- Repeat findings signal leadership breakdowns. Closing issues on paper without retesting keeps problems alive across audit cycles.

- Audit results influence banks and investors long after the audit ends. Findings shape partner trust, growth approvals, valuation confidence, and monitoring intensity.

- Audit readiness is a standing capability, not a last-minute effort. Teams that embed audit discipline into governance avoid surprises and scale with credibility.

What Actually is an Audit Checklist?

An audit checklist is more than just a list of documents for auditors. It's a strategic tool that ensures operational compliance and governance across industries. For FinTech, it focuses on areas like AML/BSA compliance and transaction monitoring.

In healthcare, it targets HIPAA data integrity and patient confidentiality, while retail audits center around PCI DSS compliance. In tech, the focus is on GDPR compliance and privacy protocols.

The best audit checklists help teams identify gaps months before external audits, reducing friction during regulatory reviews, bank evaluations, or investor diligence. A well-designed checklist:

- Reviews governance, not just compliance documents

- Tests if policies match day-to-day operations

- Helps leadership spot risk concentration and control issues

- Serves as a readiness filter before engaging with regulators or investors

Teams that use these tools early reduce duplicate findings and remediation cycles.

Also Read: Audit Procedures and Controls for Effective Risk Management

What Auditors Ask For: Key Questions

Auditors don't just check documents. They ask for explanations and proof of operation:

- Do your controls actually work? Auditors will want to test controls to see if they function in real-world scenarios, not just on paper.

- Is ownership clear? Who is responsible for implementing and maintaining controls? Unclear ownership often leads to findings.

- Can you show evidence? Documentation without evidence of control performance won’t pass muster. Auditors expect to see real-time logs, approval records, and audit trails that align with your policies.

- Do your risk assessments align with your business's growth and changes? Auditors will check if your risk framework has evolved with your products, partners, and geographies.

Now, let's understand the reasons audits go wrong and what gets us into this situation.

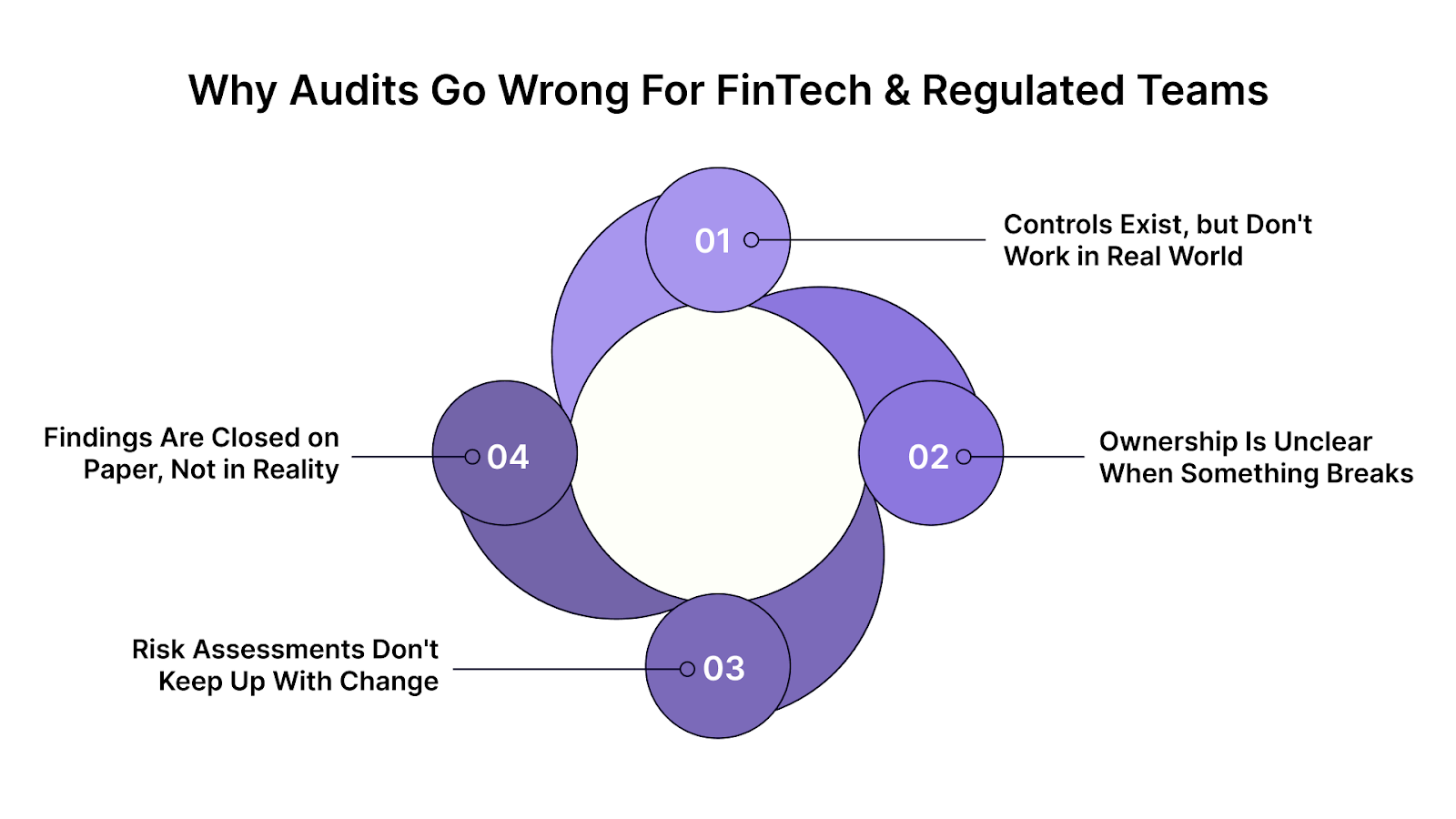

Why Audits Go Wrong for FinTech & Regulated Teams

Most audits don't go sideways because teams "forget a document." They go wrong because controls aren't operating consistently, and leadership can't defend what's happening in practice.

1) Controls Exist, but Don't Work in Real World

A typical audit finding is the gap between a control being documented and a control being effective. That matters because weak controls have real consequences.

The ACFE's 2024 fraud study found that 32% of cases involved a lack of internal controls, and 19% involved management override of existing controls. In other words, more than half of fraud cases trace back to control failures or bypass, not to missing policy language.

For FinTech audit readiness, the lesson is simple: auditors test whether controls operate, not whether they exist.

2) Ownership Is Unclear When Something Breaks

Fast-growing teams often have “shared responsibility” across product, ops, and compliance. Auditors read that differently: unclear ownership = weak governance.

Even frameworks widely used in regulated environments emphasize the timely communication of deficiencies to accountable parties, including senior leadership. When ownership isn't clear, issues don't get escalated or fixed fast enough.

3) Risk Assessments Don't Keep Up With Change

FinTechs expand into new states, new partners, new customer types, and new product lines. Controls built for the old model quietly become outdated. Regulated exam playbooks repeatedly tie control requirements back to risk assessment.

If your risk assessment doesn't reflect today's exposure, your control design won't either. This is one of the most preventable audit failures: the business evolves, but the risk baseline doesn't.

4) Findings Are Closed on Paper, Not in Reality

Repeat findings are a leadership signal. They tell stakeholders the organization can identify issues, but can't drive consistent remediation.

Practical audit guidance in large control frameworks describes how to maintain deficiency reporting and track remediation through completion and testing. When teams don't run a disciplined closure process, the same weaknesses return in the next cycle.

If these audit issues keep resurfacing or feel reactive, Fraxtional helps FinTech teams identify where governance gaps exist before auditors do. Work with experienced compliance leaders to stress-test controls, clarify ownership, and fix gaps while you still control the timeline.

How Regulators, Banks, and Investors Use Audit Results

Audit results aren't filed away. They get read as signals and reused in future decisions. In the future, the same finding may appear in three places: a bank partner review, an investor due diligence memo, and a regulator's follow-up plan.

What changes is how it's interpreted.

For Regulators

Regulators convert audit outcomes into supervisory actions. In banking, that often shows up as Matters Requiring Attention (MRAs) or similar supervisory items. Those don't disappear after the meeting ends.

For example, OCC guidance on examination scope highlights the need for quarterly follow-up for banks with open MRAs, violations, or enforcement actions.

What regulators look for isn't just the issue. It's whether you can show:

- clear ownership,

- a realistic remediation plan,

- evidence that controls now operate as intended.

For Sponsor Banks

Sponsor banks treat audits as proof of a fintech partner's ability to scale safely.

Bank exam handbooks explicitly emphasize that internal audit findings should be discussed with the audit committee or board, and that management should respond formally and in a timely way to significant adverse findings.

In practice, that means sponsor banks use audit results to decide:

- whether to expand programs,

- whether to restrict products,

- whether to require audit remediation before growth.

A clean audit doesn't just “look good." It reduces friction in ongoing monitoring.

For Investors

Investors don't read audit reports like auditors do. They read them like risk owners.

Audit findings can influence:

- valuation confidence,

- timing of capital deployment,

- and post-close remediation budgets.

In financial reporting contexts, auditors are required to communicate significant deficiencies and material weaknesses in writing to management and the audit committee.

That standard matters because it shapes how boards and capital providers interpret severity: some issues are "fix soon," others are "this can't be ignored."

All in all, audit results are not a scorecard but a trust instrument. Knowing how results are interpreted changes what your checklist needs to cover. Let’s see that ahead.

The Internal Audit Checklist FinTech Leaders Should Use in 2026

A proper audit checklist doesn't start with “what documents do we have?" It begins with “What would an auditor test to prove our controls actually work?"

This checklist is designed for FinTech and regulated teams that need to be ready for regulator scrutiny, sponsor bank monitoring, and investor diligence.

1. Governance and Ownership

- Named owner for each control area (not a shared mailbox)

- Escalation path for issues that affect customers, AML/BSA, fraud, or reporting

- Board or senior leadership visibility into audit findings and remediation status

- Issue tracking discipline: who owns the fix, due date, and proof of closure

Once a finding is logged, it often stays "alive" until it's fixed and validated. Findings create ongoing scrutiny, not a one-time conversation.

2. Policies and Procedures

- Policies are current, version-controlled, and approved by the right authority

- Procedures reflect how work actually happens (not idealized workflows)

- Clear alignment between policy → procedure → evidence

- "Last review" dates are real (and tied to business changes)

What auditors flag most often isn't missing policies. Its policies don't align with operations or cannot be consistently supported by evidence.

3. Risk Assessment and Controls

- Risk assessment reflects today's products, geographies, partners, and customer types

- Controls map clearly to the highest risks (not evenly spread across everything)

- Controls are written in a testable way: who does what, when, and how it’s evidenced

- Change management: new features or partners trigger risk re-evaluation, not just launch tasks

This is where "checklist audits" often fail: teams confirm the control exists, but can't show it's still appropriate for the current risk profile.

4. AML, BSA, Fraud, and Monitoring Oversight

- Ownership is clear for AML/BSA program decisions and fraud program decisions

- Transaction monitoring and fraud monitoring have documented tuning logic and review cadence

- SAR/alert handling has consistent escalation rules and evidence of review

- Vendor oversight is real: SLAs, performance reviews, and issue management are documented

Control breakdown is not hypothetical. It must be designed and protected in practice.

5. Data, Reporting, and Evidence

- Reports used for compliance decisions are traceable back to source systems

- Evidence is reproducible: someone else can re-run the report and get the same result

- Metrics have defined owners and definitions (no “everyone calculates it differently”)

- Audit trail is intact: approvals, exceptions, and remediation actions are documented

A quick test: if an auditor asked you to prove a control ran last quarter, could you do it in 10 minutes without Slack archaeology?

6. Findings and Closure Discipline

- Findings are categorized by severity and business impact

- Management responses include timeframes and owners

- Closure requires proof that the fix works, not just a status update

- Repeat findings are treated as governance failures, not “audit noise."

In regulated environments, closure quality matters as much as the original finding. Many audit frameworks emphasize formal, timely management responses and follow-up on significant adverse findings.

If your audit checklist feels comprehensive yet still produces findings, Fraxtional helps teams recalibrate checklists around real risk rather than templates. Review your current approach with compliance leaders who've seen what regulators and sponsor banks flag first.

How to Use an Audit Checklist Before, During, and After an Audit

A strong audit checklist is not something you "complete.” It's something you run like a cadence. The biggest difference between smooth audits and messy ones is whether teams can show consistent control performance, clear ownership, and disciplined closure.

Before the Audit: Use the Checklist to Reduce Surprises

1) Confirm scope and stakeholders early

External auditors are expected to align with audit committees on engagement terms and key audit matters. That's a reminder that audit expectations are set up front, and misalignment creates churn later.

Checklist actions:

- Document audit scope, period, systems, and responsible owners

- Create a single source of truth for evidence requests

- Identify “high scrutiny” areas (AML/BSA, vendor oversight, reporting accuracy)

2) Test controls, don’t just inventory them

The fastest way to fail an audit is to show a control exists but can’t prove it operated.

Checklist actions:

- Pull 2–3 samples per key control (recent, real, reproducible)

- Verify approvals, timestamps, and reviewer identity are auditable

- Identify controls that are being performed late or inconsistently

3) Pre-classify issues like an auditor would

Auditors differentiate severity. Under PCAOB standards, auditors must communicate in writing to management and the audit committee any significant deficiencies and material weaknesses. That's why teams should triage issues early before they reach that threshold.

Checklist actions:

- Log gaps with an owner, due date, and interim mitigation

- Separate “documentation clean-up” from “control failure."

- Escalate anything that could impact customer harm, AML/BSA, or reporting integrity

During the Audit: Use the Checklist to Control Narrative & Speed

1) Keep responses consistent and owned

Auditors care about clarity. Sponsor banks and investors care about consistency. Inconsistent answers are a signal of weak governance.

Checklist actions:

- One intake channel for requests, one tracker, one owner per request

- Standardize definitions (metrics, thresholds, review cadence)

- Prevent “shadow updates” to policies mid-audit without change control

2) Treat control deficiencies as management decisions, not admin work

When auditors identify control deficiencies, they expect an accountable management response, not just “we'll fix it."

Checklist actions:

- Respond with root cause, corrective action, and validation method

- Document interim controls if remediation will take time

- Track every open item and its evidence of closure

After the Audit: Use the Checklist to Prevent Repeat Findings

1) Run closure like a verification process

Findings don't truly close when the fix is shipped. They close when the fix is tested and proven. This matches how regulators think about issues, too.

Checklist actions:

- Define what “closed” means: fix implemented + evidence collected + retest passed

- Require proof that the control now operates reliably

- Track repeat findings as governance failures, not audit noise

2) Build monitoring into the normal operating rhythm

Modern control frameworks emphasize ongoing monitoring and the correction of control deficiencies as conditions change. That's what keeps audits from becoming fire drills.

Checklist actions:

- Set a quarterly internal review cadence for key controls

- Track KPIs like “controls performed on time” and “average remediation time"

- Roll learnings into governance routines, not a separate "audit project."

Even well-designed checklists fail when applied the wrong way. Let's look at some common mistakes and how to fix them.

Also Read: 5 Key Steps to Perform a Risk-Based Internal Audit

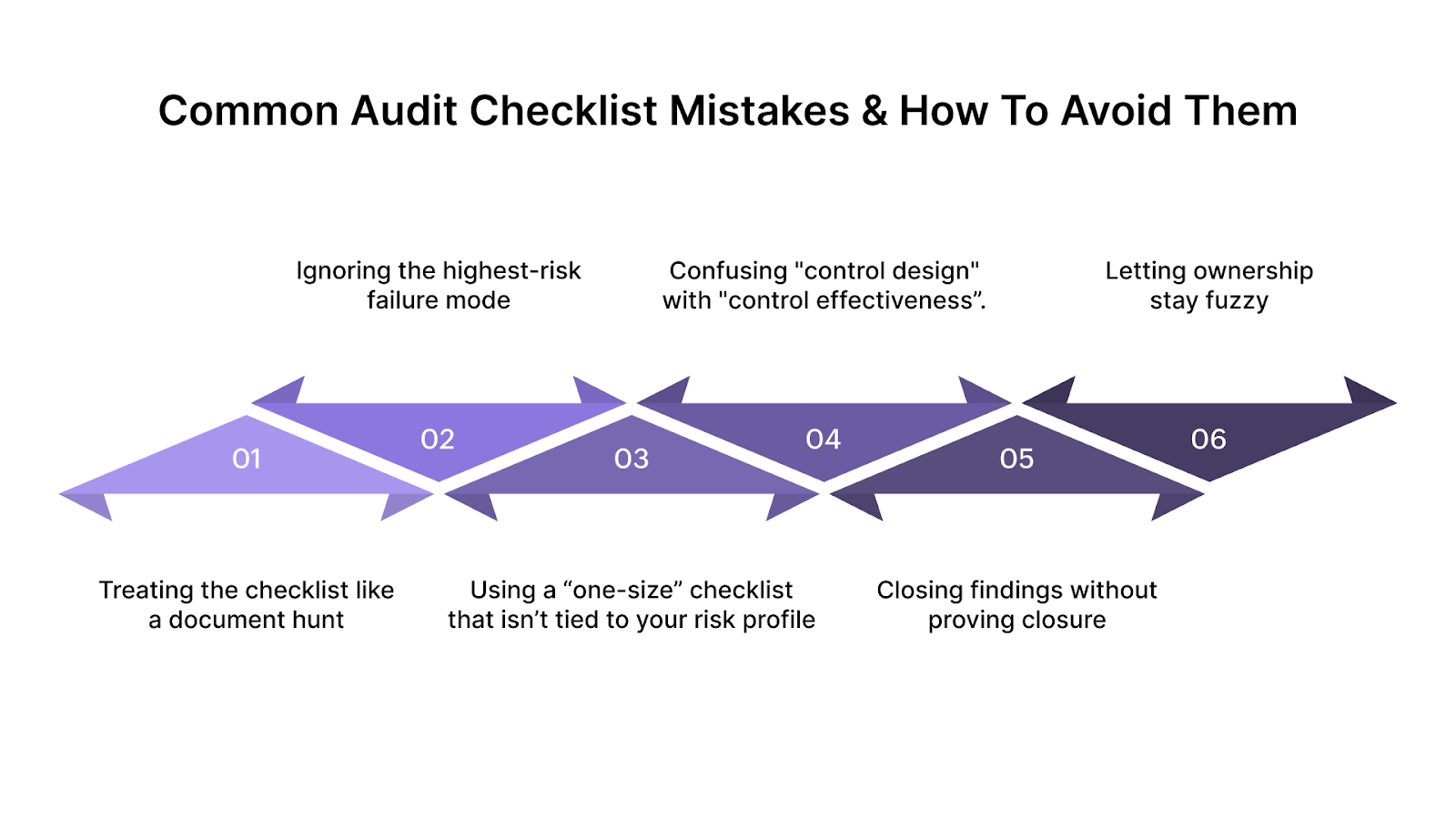

Common Audit Checklist Mistakes & How to Avoid Them

Most audit checklist problems aren't about effort. They're about what the checklist is designed to prove. Here are the mistakes that create avoidable findings for FinTech and regulated teams, plus the fix that actually holds up under scrutiny.

1) Treating the checklist like a document hunt

Audit standards put heavy weight on documentation that supports the work performed, and the conclusions reached. If evidence doesn't show execution and review, it won't carry.

- Fix: For every item, require proof of operation (samples, approvals, timestamps), not just existence.

2) Ignoring the highest-risk failure mode: weak internal controls

A checklist that doesn't pressure-test controls misses the most significant predictable cause of audit pain.

- Fix: Add checklist steps that test control durability: exceptions, overrides, access changes, and whether reviews actually happened.

3) Using a “one-size” checklist that isn’t tied to your risk profile

Generic checklists create busywork and miss what matters. In regulated environments, auditors and examiners scope work relative to risk.

- Fix: Start with your risk assessment. Then build the checklist around the top exposures (products, partners, geographies, customer types).

4) Confusing "control design" with "control effectiveness”.

Many teams document controls well, but don't validate that they operate reliably.

That's precisely the gap auditors tend to punish: evidence of consistent performance is different from a well-written policy.

Fix: For each key control, add:

- Sample testing (2–3 real examples),

- Evidence of reviewer sign-off, and

- A clear pass/fail standard.

5) Closing findings without proving closure

A status update is not a closure. Stakeholders look for validation.

Strong control frameworks emphasize ongoing monitoring and the detection and remediation of control deficiencies, not just logging them.

- Fix: Require “closure proof” in the checklist: fix implemented + retest completed + evidence stored.

6) Letting ownership stay fuzzy

When the checklist doesn't assign a single owner per area, audits become Slack archaeology and lead to inconsistent answers.

Auditors also distinguish severity (e.g., significant deficiency vs material weakness) and communicate those formally.

- Fix: One accountable owner per checklist section, with defined escalation rules for high-risk gaps.

With all these in mind, getting there consistently requires more than process. It requires leadership. This is where a partner like Fraxtional becomes essential.

How Fraxtional Turns Audit Checklists Into Real Assurance

Alt text:How Fraxtional Turns Audit Checklists Into Real Assurance

Audit checklists are only as strong as the leadership behind them. Fraxtional operates at the point where internal audit work must translate into credible governance, not just completed tasks.

Instead of treating audit preparation as a periodic exercise, Fraxtional treats it as an ongoing leadership function tied directly to risk, oversight, and accountability.

- Stabilizing Audit Ownership: Fraxtional's fractional compliance and risk leaders step in to ensure clear ownership across audit domains, consistent evidence production, and uninterrupted audit and remediation cycles.

- Aligning Checklists With Real Risk: Fraxtional recalibrates around actual exposure. That includes mapping checklist items to the company's current risk profile and prioritizing high-impact control areas.

- Keeping Findings From Becoming Repeat Findings: Fraxtional helps teams move beyond "status updates" by defining what true closure looks like, validating remediation through retesting, and embedding follow-up into governance routines.

- Translating Audit Output for Leadership: Fraxtional's leaders translate audit results into clear risk narratives for executives and boards, prioritized decision points, and defensible explanations for regulators, banks, and investors.

- Audit Readiness as a Standing Capability: Fraxtional's model gives companies senior oversight calibrated to the moment: accountable, experienced, and immediately effective, without locking into premature full-time headcount.

Partner with Fraxtional to turn audit preparation into a standing assurance capability that scales with growth and holds up under scrutiny.

Conclusion

Modern tools have made audits faster and more measurable, but they haven't changed what regulators, sponsor banks, and investors ultimately look for: clear ownership, defensible decisions, and consistent follow-through. A completed checklist without accountability is still a risk.

That's why audit readiness in 2026 isn't driven solely by documents. It's driven by how well teams connect controls to real risk, findings to closure, and evidence to judgment. Strong audit checklists keep systems organized. Strong leadership keeps them credible.

Fraxtional helps teams make that shift by pairing experienced compliance leadership with modern audit and governance tools, turning audit checklists into confidence under scrutiny.

FAQs

An internal audit checklist should be reviewed whenever the business changes materially and at least annually. New products, partners, geographies, or regulatory guidance should trigger immediate updates to avoid testing outdated controls.

Ownership should sit with a senior compliance or risk leader who has the authority to escalate issues. Shared ownership often leads to gaps, delays, and inconsistent responses during audits.

No. SOC 2 reports assess specific trust criteria, not full regulatory or operational risk. Regulators, sponsor banks, and investors still expect internal audits that reflect the company's full risk profile.

Auditors often flag missing evidence of control operation, unclear ownership, and weak remediation tracking. These issues matter more than formatting or checklist completeness.

Unresolved or repeated gaps can slow onboarding, limit program expansion, or trigger additional monitoring. Sponsor banks view audit discipline as a signal of a fintech's reliability in managing ongoing risk.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.