Mar 20, 2026

ACH Payments: How They Work and How to Run Them Well in 2026

By Fraxtional LLC

ACH payments are the default “bank transfer” rail for the United States used for payroll, recurring bills, B2B payouts, account funding, and countless behind-the-scenes money movements. The scale is still growing: in 2025, the ACH Network processed 35.2 billion payments totaling $93 trillion, and Same Day ACH reached 1.4 billion payments totaling $3.9 trillion.

For fintech leaders, ACH isn’t hard because the concept is complex. It’s hard because day-to-day reality includes cut-off windows, returns, fraud patterns, sponsor-bank scrutiny, and new operating rules that tighten expectations across the network.

Overview

- ACH payments are the backbone of US bank transfers - The ACH network powers payroll, bill payments, subscriptions, and B2B transfers, processing tens of billions of transactions annually across the US banking system.

- Understanding the ACH process is essential for reliable payment operations - Every transaction moves through defined roles - Originator, ODFI, ACH Operator, and RDFI, with file-based processing windows that determine when payments settle.

- Operational complexity increases significantly as payment volumes scale - At higher volumes, issues like return rates, authorization management, fraud monitoring, and sponsor-bank expectations become core operational metrics rather than occasional exceptions.

- Upcoming 2026 Nacha rule updates will raise expectations for fintech teams - New requirements around fraud monitoring, updated Company Entry Descriptions such as PAYROLL and PURCHASE, and revised funds availability timelines will require operational and compliance updates.

- Fraxtional helps fintech teams scale ACH programmes responsibly - By providing fractional compliance leadership, policy development, and independent risk oversight, Fraxtional helps organisations meet sponsor-bank expectations while managing fraud risk, returns, and evolving Nacha rules.

What Are ACH Payments?

ACH payments are electronic bank-to-bank transfers made through the Automated Clearing House (ACH) network. They’re used for everyday money movement, such as direct deposit, bill payments, subscriptions, loan repayments, and business disbursements without going through card networks.

The two main types of ACH payments

- ACH credit (push payment): money is sent to someone (e.g., payroll deposits, payouts, refunds).

- ACH debit (pull payment): money is collected from someone (e.g., recurring subscriptions, loan instalments, utility bills).

How ACH moves money

ACH works through a defined chain of roles:

- The Originator (your company or your customer) initiates the payment instruction.

- The ODFI (Originating Depository Financial Institution) is the originator’s bank (often a sponsor bank in fintech programmes).

- An ACH Operator receives the file, sorts it, delivers entries to the correct receiving banks, and settles between institutions.

- The RDFI (Receiving Depository Financial Institution) is the receiver’s bank, which posts the transaction to the end account.

There are two national ACH operators in the US: the Federal Reserve (FedACH) and the Electronic Payments Network (EPN).

How Do ACH Payments Work In Practice?

ACH payments follow a defined path between banks, the ACH operators, and (often) a processor or programme manager in the middle. At scale, what matters most is understanding who touches the payment, when settlement happens, and how exceptions (like returns) flow back through the network.

The key participants in an ACH transfer

Even if you never see these labels in your product UI, they shape how the transaction behaves:

- Originator: The business initiating the payment (or debit request).

- ODFI (Originating Depository Financial Institution): The Originator’s bank (in fintech programmes, this is typically the sponsor bank).

- ACH Operator: The network operator that receives ACH files, edits/sorts them, delivers entries to receiving banks, and settles between institutions. The US has two national ACH operators: the Federal Reserve Banks (FedACH) and the Electronic Payments Network (EPN).

- RDFI (Receiving Depository Financial Institution): The Receiver’s bank.

- Receiver: The account holder receiving a credit or whose account is being debited.

What happens behind the scenes (from initiation to posting)?

In production, ACH processing is best thought of as a file-based workflow with scheduled processing windows.

1. The payment instruction is created (credit or debit)

- ACH credit: you send money to someone (payroll, payouts, refunds).

- ACH debit: you collect money from someone (subscriptions, repayments, bill pay). Most fintechs create these entries via a processor/TPSP, but the underlying chain still routes through the ODFI → ACH Operator → RDFI path.

2. Entries are packaged into an ACH file and submitted by the ODFI

The ODFI (or its channel/processor on its behalf) submits a batch/file in the standard ACH file format (often referred to as a “Nacha file”).

3. The ACH Operator sorts, routes, and settles

The operator’s job is to sort entries so each one reaches the correct RDFI. Operators also handle interbank settlement by crediting/debiting participating institutions’ settlement accounts.

4. The RDFI posts the transaction to the Receiver’s account

Once the RDFI receives the entry, it posts it (either crediting or debiting the account), and the Receiver sees the result in their account, subject to the bank’s posting routines and funds-availability requirements.

What happens when an ACH payment can’t be completed

At higher volumes, you should expect exceptions; it’s part of the rail.

- If an ACH transaction can’t be completed, the receiving institution generates a standardized return code indicating the reason (e.g., insufficient funds, closed account, invalid details, or authorization-related issues) and sends it back through the ACH Network.

- In many cases, the typical return timeframe is two banking days, while some scenarios (such as certain unauthorized consumer debits) may have longer timeframes this is why return handling and customer communication need clear rules and automation.

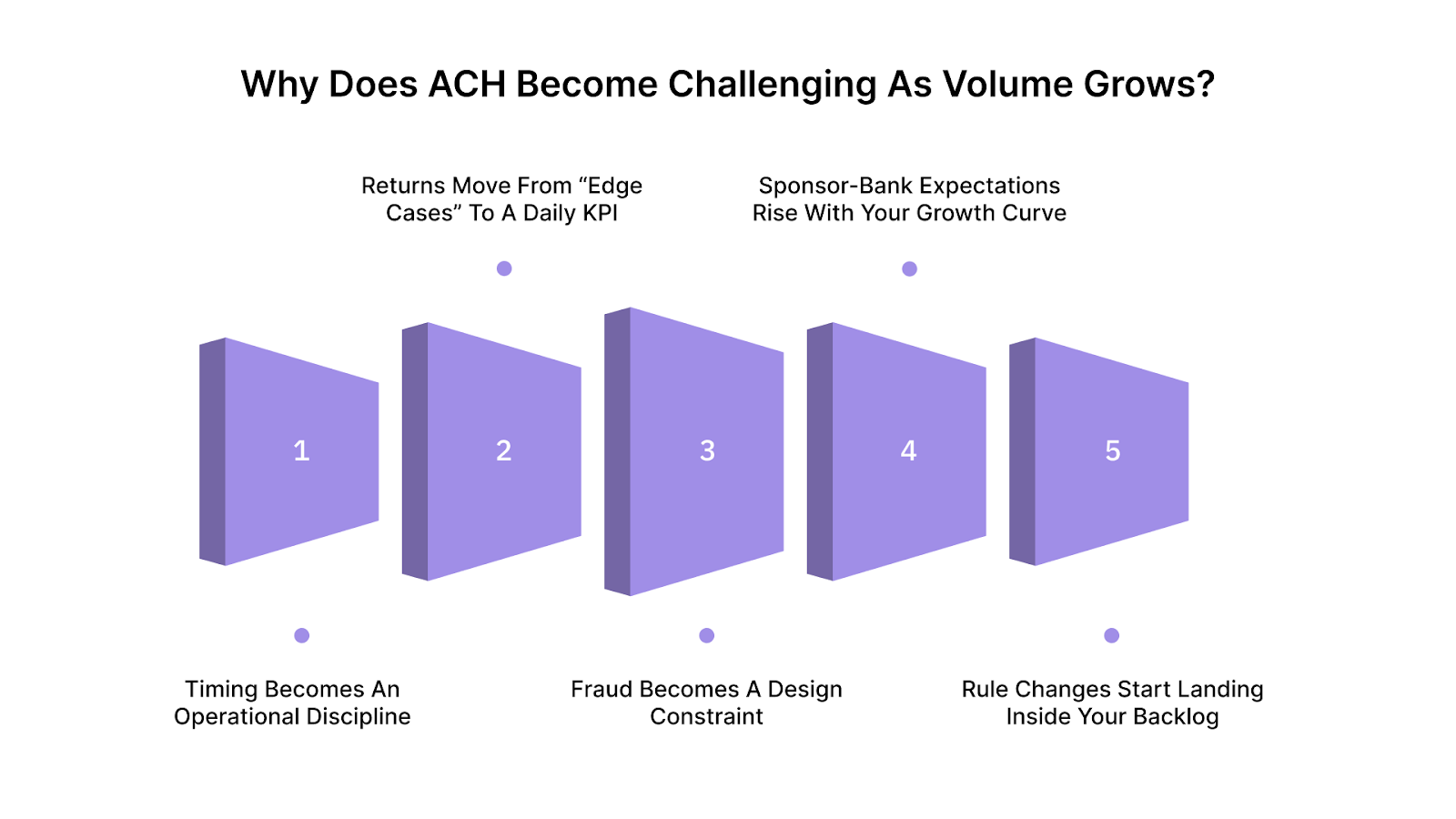

Why Does ACH Become Challenging As Volume Grows?

ACH looks straightforward at low volume. The complexity shows up when you move from “a few transfers” to “a payments programme” with thousands of entries, multiple use cases, and a sponsor bank watching performance.

1) Timing becomes an operational discipline, not a customer promise

ACH runs on processing windows and cut-offs, so small workflow delays can compound quickly at scale. A missed file cut-off can push settlement by a full business day, which in turn drives support tickets, refunds, and reconciliation cleanup.

2) Returns move from “edge cases” to a daily KPI

At higher volume, you will see more:

- invalid account details,

- closed accounts,

- insufficient funds,

- authorization disputes (especially for debits).

The issue isn’t that returns exist; it’s that return patterns become a measurable signal of onboarding quality, authorization hygiene, and fraud exposure. Banks and processors should pay attention because sustained deterioration in return rates can indicate a structural risk in the programme.

Nacha also defines risk thresholds used to identify elevated risk, for example, an unauthorized return rate threshold of 0.5% for specific unauthorized debit return codes.

3) Fraud becomes a design constraint

As volumes and customer segments broaden, fraud attempts shift from opportunistic to systematic, with payroll redirection, vendor impersonation, and account takeover patterns. These are exactly the kinds of scenarios Nacha is targeting with its 2026 rule updates on fraud monitoring.

4) Sponsor-bank expectations rise with your growth curve

Many fintech teams interpret increased oversight as simply “more questions” and “more approvals,” but what's actually happening is a governance shift. As throughput grows, banks typically want clearer evidence of:

- exception handling (returns, disputes, corrections),

- control ownership across teams and vendors,

- remediation plans when metrics move in the wrong direction.

This is less about paperwork and more about giving all stakeholders confidence that the programme remains safe as scale increases.

5) Rule changes start appearing in your backlog

At a small scale, teams often treat Nacha updates as “compliance news.” At the programme scale, they become implementation work, field-level changes, monitoring requirements, QA, and coordination with processors and sponsor banks.

For example, Nacha’s New Rules include 2026 updates covering fraud monitoring and new standardized Company Entry Descriptions (e.g., PAYROLL and PURCHASE) that can affect how common ACH flows must be labelled and monitored.

If you’re seeing higher return rates, changing fraud patterns, or more sponsor-bank questions as you grow, Fraxtional can help. We pressure-test your ACH controls, provide compliance leadership, and prioritize impactful fixes to keep your programme bank-ready at scale.

ACH Transfers vs Bank Transfers: What’s The Difference?

In payments operations, ACH is a specific type of bank transfer that behaves differently from other rails, such as wire transfers and, in some contexts, real-time rails.

Key Benefits Of Running ACH Payments Well

When ACH is treated as a core payment rail supported by clear ownership, monitoring, and strong exception handling, it becomes more than just a low-cost transfer method. Well-run ACH programmes improve cash-flow predictability, reduce operational friction from returns and disputes, and strengthen credibility with sponsor banks and partners as transaction volumes scale.

Lower cost with broad reach across US bank accounts

One of the biggest advantages of ACH is its ability to move funds across the US banking system at relatively low cost compared with card networks or wire transfers. Because nearly every US bank account can receive or send ACH payments, it provides broad coverage for payroll, vendor payments, subscriptions, and B2B transfers.

For organisations running high-volume payments, such as payroll providers, SaaS platforms, and marketplaces, this combination of reach and lower processing costs can significantly improve payment economics over time.

Strong fit for predictable, operational payments

ACH is designed for routine and repeatable payment flows, making it particularly well suited for operational use cases like payroll deposits, subscription billing, loan repayments, insurance payouts, and supplier disbursements.

These payment types typically benefit from scheduled processing and predictable settlement cycles. With the expansion of Same Day ACH, businesses now have additional flexibility for time-sensitive payments without moving entirely to faster but more expensive rails.

Better resilience through reversibility and structured exception handling

Unlike some real-time payment rails, ACH includes structured return and correction processes that allow institutions to resolve errors or disputes through established procedures. This framework can provide operational resilience when payments fail due to insufficient funds, incorrect account details, or authorization disputes.

However, the benefits only appear when organisations maintain strong operational playbooks. Clear return-handling processes, automated monitoring, and well-defined escalation paths help teams respond quickly to exceptions while maintaining return-rate thresholds and compliance expectations.

Over time, this operational discipline reduces payment friction, improves customer experience, and builds confidence with sponsor banks that the programme can scale safely.

A useful comparison for UK/EU/Canada operators

If you operate across regions, it’s worth anchoring expectations:

- UK: Bacs Direct Credit runs on a three-day cycle (input → processing → entry), which shapes payroll and supplier-payment planning.

- EU (Euro area): SEPA Credit Transfer is the standard euro credit transfer scheme across SEPA countries (with separate instant schemes where available).

- Canada: Canada’s retail batch system (ACSS/USBE) underpins domestic batch clearing for many payment types.

The point isn’t that these systems are the same as ACH—they aren’t. Rather, the takeaway is that batch payment rails everywhere reward disciplined operations and expose weak or unrealistic timelines.

Nacha Rule Updates To Build Into Your 2026 Roadmap

Nacha’s new rules page is the most reliable place to track changes, when they occur, and why.

Fraud monitoring requirements (phased in during 2026)

- Phase 1 becomes effective March 20, 2026 and is part of Nacha’s risk management package focused on reducing fraud success rates and improving recovery.

- Phase 2 expands requirements later in 2026 (effective June 19, 2026, with practical next-banking-day timing noted in the rule materials).

What this means operationally: fraud monitoring isn’t “nice-to-have” if you want stable bank relationships it becomes a documented expectation with clear deadlines.

New company entry descriptions: Payroll and Purchase

Nacha adds defined Company Entry Descriptions:

- PAYROLL for certain payroll-related credits, and

- PURCHASE for certain e-commerce purchase debits, effective March 20, 2026.

Funds availability for non-Same Day ACH credits (effective September 18, 2026)

Nacha states that this update eliminates a prior receipt condition, so funds are available at 9:00 a.m. (RDFI local time) on the settlement date for non-Same Day credit entries.

For fintechs, this can influence customer experience promises for payroll, benefits, insurance payouts, and other credit flows.

How Fraxtional Strengthens ACH Compliance and Risk Management

As ACH volume grows, sponsor banks and partners typically expect more than “we have a processor.” They want clear ownership, documented controls, and evidence that risk is actively managed. Fraxtional’s model is built for this stage, providing embedded, senior risk and compliance leadership that works as part of your team.

Here’s how that applies to an ACH programme:

- Sponsor bank readiness (and smoother onboarding): Fraxtional supports fintechs end-to-end from first contact through approval backed by compliance preparation, policy support, and internal reviews aligned to bank expectations.

- Named compliance leadership without a full-time hire: If a bank requires accountable leadership, Fraxtional can provide fractional leaders ready to act as a named CCO or BSA Officer, helping you meet governance expectations while you scale.

- Faster policy and procedure build-out: ACH programmes live or die on documented processes (monitoring, exception handling, vendor oversight, escalation). Fraxtional explicitly supports policy and procedure work and fast turnaround on compliance documentation, often the bottleneck in bank diligence.

- Executive-led AML oversight that supports partnerships and audits: For fintechs where ACH is part of a broader payments product, Fraxtional embeds a “battle-tested” Chief AML Officer and positions this as support for securing partnerships and passing audits.

- Independent assurance when you need credibility: When banks, investors, or regulators want proof that controls work (not just that they exist), it offers independent audit services to uncover blind spots and strengthen internal controls, helping organisations move faster with stakeholders.

- Operationalizing rule changes into a real plan: New network expectations (including Nacha updates) create implementation work, monitoring, control testing, documentation, and coordination across your bank + processor. Fraxtional’s embedded leadership + policy/audit capabilities are designed to carry that load while your product team keeps shipping.

If your business is scaling ACH and needs stronger sponsor-bank confidence, cleaner return performance, and a clear plan for the 2026 Nacha updates, Fraxtional can provide fractional risk and compliance leadership to build the controls, documentation, and operating cadence without hiring a full-time executive team.

Conclusion

ACH payments remain a foundational payment rail for payroll, billing, and high-volume money movement across the United States. But as transaction volumes grow, ACH stops being just a payment feature and becomes an operational discipline involving returns management, fraud monitoring, and evolving Nacha rules.

Fintech teams that treat ACH as a structured operating model, with clear controls, monitoring, and governance, are far better positioned to scale safely and maintain strong sponsor-bank relationships. With the right processes in place, ACH can remain one of the most reliable and cost-efficient ways to move money.

FAQs

Standard Entry Class (SEC) codes indicate the type of ACH entry and, in many cases, how it was authorized (for example, consumer vs corporate, internet-initiated, etc.). Using the right SEC code helps keep processing, reporting, and risk controls consistent across banks and processors, especially as volume scales.

In practical terms, PPD is commonly used for consumer payments such as payroll direct deposit and consumer bill pay; CCD is used for corporate-to-corporate entries; and WEB is used for internet-initiated consumer debits (often used by fintechs for account-to-account funding or subscription collection). The right choice depends on who the recipient is and how the authorization was obtained, so it’s worth aligning with your ODFI/processor early.

Many programmes validate accounts before initiating live transfers to reduce returns and support smoother onboarding. Nacha rules allow prenotification entries (prenotes) for account validation before sending the first live credit/debit and also recognize use cases for re-validating certain accounts before renewed ACH activity.

For WEB entries, authorization is a core requirement and is governed by both the Nacha Operating Rules and Regulation E considerations. In practice, you’ll want a clean audit trail showing the customer’s agreement/assent (what they accepted, when, and how), plus any related authentication signals your flow relies on.

An IAT applies when an ACH payment is part of a transaction involving a financial agency outside the territorial jurisdiction of the US, which triggers additional information and screening considerations. Nacha’s rule update also clarifies that an IAT entry cannot be a Same Day entry, with the amendment effective 18 September 2026.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.