Mar 13, 2026

Guide To California Money Transmitter License Requirements

By Fraxtional LLC

Summarize the blog with AI

Are you planning to move customer funds or crypto in California and wondering where the regulatory line sits? Many FinTech and crypto teams launch fast, only to realize later that licensing questions can slow everything down.

That concern is not theoretical. In 2023, foreign transfers made up 9% of U.S. money transmission volume, with an average transaction of $370, showing how closely regulators watch cross-border flows. When even routine payments move globally, compliance becomes part of your daily operations, not a side task.

This blog walks you through how the money transmitter license in California framework works, from definitions to approval requirements. Stick till the end to learn the common mistakes that slow teams down and how to avoid them.

Key Takeaways:

- A California money transmitter license regulates businesses that move or hold customer funds.

- The license ensures legal operation while protecting customer funds and regulatory compliance.

- The licensing process includes pre-filing review, NMLS application, document submission, and surety bond posting.

- Most challenges come from incomplete filings, missing control person info, and gaps in AML or OFAC policies.

- Start preparation early and keep records organized to reduce delays and regulator follow-ups.

What Is A Money Transmitter Under California Law?

Under California law, a money transmitter is any business that receives money from one party and sends it to another, including digital, mobile, and online platforms. This covers wire transfers, mobile payments, and transfers between users or merchants.

If your platform handles customer funds in any way, a money transmitter license in California is required. Here is how common activities typically get classified:

Once you understand how broadly California defines money transmission, the licensing requirement becomes more predictable.

Why Is A California Money Transmitter License Required?

The license exists to protect customers and the financial system. When people trust you with their money, the state wants proof that you can manage that responsibility. Licensing creates that checkpoint.

Here are the main reasons the license is required.

- Consumer protection: You must show that customer funds are handled safely and kept separate from business expenses.

- Financial stability: California checks your net worth and liquidity to confirm you can meet withdrawals and payment obligations.

- Risk and compliance oversight: Your policies for anti-money laundering and record keeping must meet state standards.

- Ongoing accountability: Licensed firms must file reports and stay open to regulatory exams.

- Business credibility: Banks and investors usually require a valid license before they support your platform.

Without this approval, your company risks fines, shutdowns, or frozen banking access. With the purpose explained, you can now move ahead with preparing your application.

Also Read: KYC vs CDD vs EDD Key Differences Explained

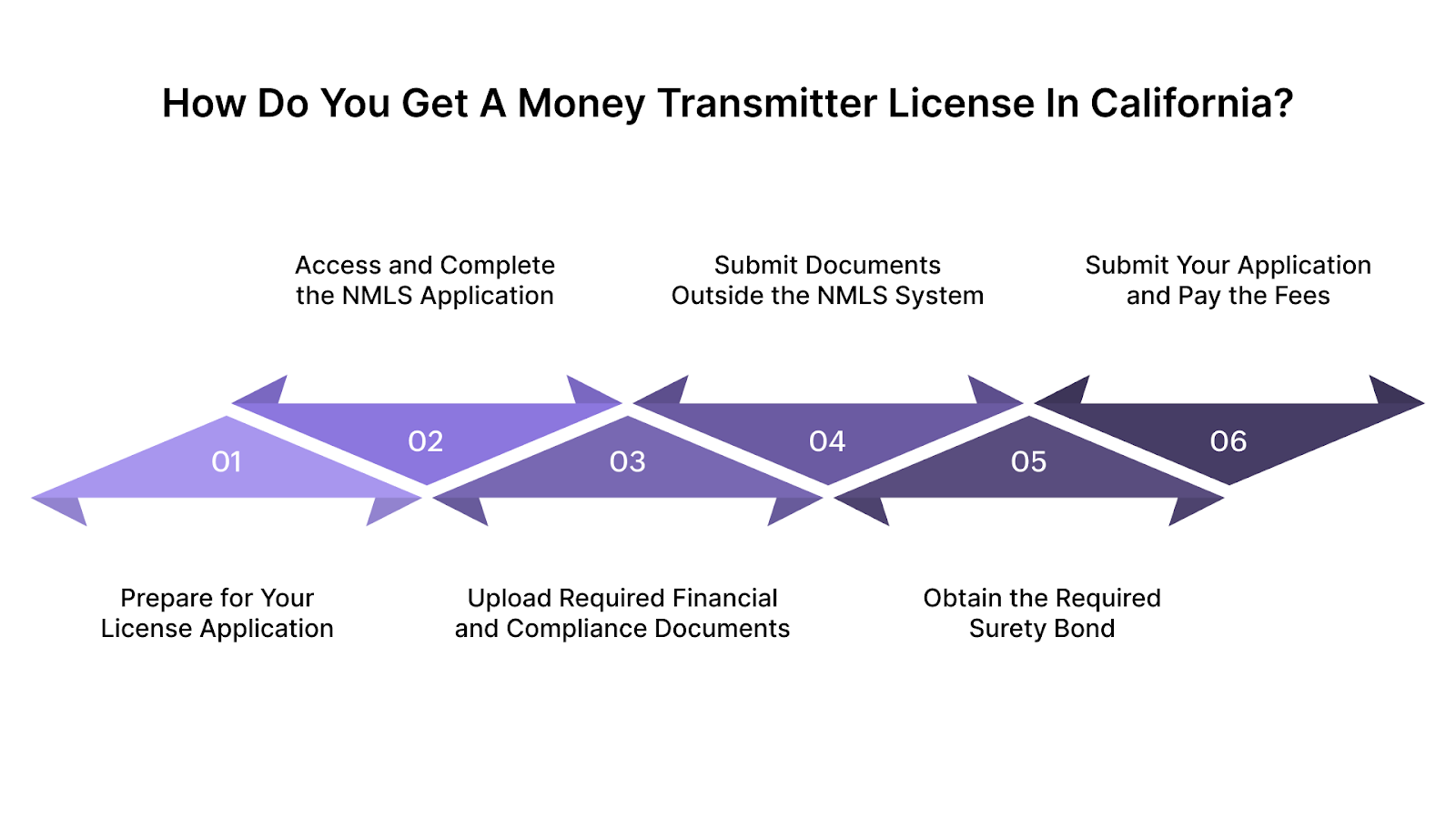

How Do You Get A Money Transmitter License In California?

Getting approved in California requires preparation, detailed filings, and coordination through the NMLS system. The state reviews how your business handles funds, who controls it, and how risks are managed.

Here’s how you can get your money transmitter license in California:

1. Prepare for Your License Application

Before filing anything, you must review the California Money Transmission Act. This law defines how you must operate after approval, including reporting, consumer protection, and record retention duties.

The Money Transmitter Division strongly recommends scheduling a pre-filing meeting. This meeting lets you confirm how your business model fits the law before paying the non-refundable filing fee.

- Review duties under the California Money Transmission Act

- Confirm whether your product holds or transfers customer funds

- Schedule a pre-filing meeting with the Money Transmitter Division

- Identify all control persons and ownership interests

2. Access and Complete the NMLS Application

California processes all money transmitter applications through the Nationwide Multistate Licensing System. You must register your company and complete the required electronic forms.

NMLS collects both company and control person data.

- MU1 company application

- MU2 forms for all control persons

- Identity verification and credit authorization

- Registered agent and trade name listings

- Primary company and consumer complaint contacts

- FinCEN registration number, when applicable

- Bank account details for operating, trust, and credit accounts

- Disclosure question responses with written explanations

3. Upload Required Financial and Compliance Documents

California requires extensive documentation that explains how your company operates and manages risk. These records allow regulators to assess stability, transparency, and customer protection.

You must submit:

- Audited financial statements prepared in accordance with GAAP

- Pro forma financial projections for three years

- Business plan with products, fees, and target markets

- AML and BSA policy with the most recent independent review

- OFAC compliance description

- Flow of funds for each transaction type

- Sample transaction receipts and payment instruments

- Management and organizational charts with ownership percentages

- Certificate of Good Standing or Authority issued within sixty days

4. Submit Documents Outside the NMLS System

Several items must be mailed directly to the state because they cannot be uploaded through NMLS. California uses these to complete background and fitness reviews.

You must send:

- DBO Form 2 personal financial statements

- DBO Form 550 emergency contact form

- DBO Form 4030 authorization for release of information

- Board authorization resolutions

- At least two banking references

- Branch and agent growth estimates for three years

- Agent selection and supervision policies

- Fingerprints and background checks for control persons

- Foreign background reports, when required

Note: These records must be mailed to the Money Transmitter Division at the same time your NMLS file is submitted.

5. Obtain the Required Surety Bond

Every applicant must post a surety bond to protect customer funds. The bond amount depends on how your business handles money.

Bond rules include:

- Payment instruments or stored value require at least $500,000 or 50% of outstanding obligations

- Money transmission requires a bond above average daily outstanding amounts

- Minimum bond is $250,000, and the maximum can reach $7,000,000

- Bond amounts are cumulative across activities

You pay a premium that reflects your credit and financial profile, not the full bond amount.

6. Submit Your Application and Pay the Fees

You must submit your full package through NMLS while mailing the required forms to California. The state charges a $5,000 application fee plus credit report fees for control persons.

Once filed, regulators review your business, finances, and compliance structure. If all requirements are met, your money transmitter license in California will be issued.

Feeling stuck after reviewing California’s licensing steps? Fraxtional helps teams validate requirements, prepare filings, and avoid costly rework before regulators ever review the application. Contact us today!

Common Challenges In California MTL Applications

Even well-prepared applicants often face delays during California’s review process. Regulators evaluate applications holistically, not just document completion. Small gaps can raise broader questions about governance, controls, or financial readiness.

Below are the most common issues regulators flag during review:

- Incomplete or Outdated Financial Statements:

Regulators expect recent, accurate financials that show liquidity, cash flow, and ongoing stability. Applications often stall when statements are missing, outdated, or inconsistent across submissions. - Weak or Generic AML and BSA Policies:

California requires detailed policies that explain how your company monitors transactions and reports suspicious activity. Applications get delayed when policies are copied or lack independent review. - Unclear Flow of Funds:

The state expects a step-by-step explanation of how money moves from customer to recipient. When transaction paths or wallet structures are vague, regulators cannot assess customer risk. - Ownership and Control Gaps:

Every direct and indirect owner must be disclosed with voting percentages. Delays happen when subsidiaries, parent entities, or control persons are not clearly mapped. - Missing or Incomplete Background Checks:

Fingerprinting, credit reports, and foreign background checks are mandatory for many control persons. Reviews pause when any of these checks remain incomplete. - Bank Account and Reference Issues:

California verifies how you hold operating and trust accounts. Applications often slow down when banking details or reference letters are missing or inconsistent.

Also Read: 10 Effective Techniques for Compliance Remediation

How Fraxtional Supports California Money Transmitter Licensing

Applying for a California money transmitter license is rarely just a paperwork exercise. Regulators evaluate your risk controls, leadership experience, and operational readiness, which means small compliance gaps can delay approvals for months.

Fraxtional helps fintech, crypto, and payments companies move through the licensing process faster and with fewer regulatory surprises by combining compliance expertise with hands-on execution. Instead of leaving your team to navigate complex filings alone, it manages the process end-to-end while ensuring your compliance framework meets regulator expectations.

What makes Fraxtional different is its fractional leadership model. You gain access to experienced compliance executives and licensing specialists without hiring a full-time internal team. This approach gives early-stage and scaling companies the expertise regulators expect while keeping operational costs manageable.

Fraxtional supports companies throughout the entire licensing lifecycle, including:

- Regulatory readiness reviews to confirm whether your business model triggers California money transmission requirements.

- End-to-end license application management, including NMLS filings, documentation preparation, and regulator responses.

- Compliance program development, such as AML/BSA policies, risk assessments, and flow-of-funds documentation.

- Sponsor bank and partner readiness, ensuring your compliance structure meets bank and investor expectations.

- Multi-state licensing strategy, helping companies expand beyond California as they grow.

The result is a structured licensing process where applications are complete, policies are regulator-ready, and communication with regulators stays proactive.

Final Thoughts

A California money transmitter license means a commitment to transparency, controls, and customer protection. Succeeding requires early planning, complete documentation, and a clear sense of how regulators view risk.

With a structured approach, licensing becomes more predictable and less disruptive. Good preparation, accurate filings, and readiness for compliance mean fewer delays and smoother approval.

If you are planning to apply or reassess your licensing strategy, Fraxtional supports you through every step with our dedicated Money Transmitter Licensing services. Contact us today for a consultation to ensure your filings, insurance, and compliance setup are regulator-ready.

FAQs

Yes, if your business receives or transfers money for others in California, you usually need a state money transmitter license before you can legally operate.

In California, Bitcoin and other virtual currency activities may fall under the Money Transmission Act if they involve receiving, holding, or transferring value on behalf of customers.

You qualify as a money transmitter when your business receives money or stored value from one party and sends it to another. This applies whether the transfer happens through bank rails, payment apps, or virtual currency systems.

A trading platform may operate without a license only if it never takes custody of customer funds or crypto and simply connects buyers and sellers.

Yes, if your platform controls or holds crypto on behalf of users, California regulators may treat that activity as money transmission.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.