Feb 18, 2026

Banking Risk Assessment Guide: What U.S. Banks Miss in 2026

By Fraxtional LLC

Summarize the blog with AI

In the past year, U.S. regulators issued final interagency guidance that pushes banks to manage risk across the full lifecycle of third-party relationships planning, due diligence, contracting, ongoing monitoring, and exit planning.

That raised the bar for what a banking risk assessment must demonstrate in practice.

And the gap is showing. In 2024, Reuters reported that a confidential OCC assessment found 11 of 22 large banks had "insufficient" or "weak" risk-management practices, spanning areas like cybersecurity and operational errors.

For many institutions, the problem isn't that they don't run a banking risk assessment. It's that the assessment doesn't align with how the bank actually operates. Vendor dependencies, product changes, control testing results, and what the board is actually being asked to oversee.

This guide explains what U.S. banks still miss in 2026. Learn how to build a banking risk assessment that reflects real exposure, holds up under exams, and drives action instead of paperwork.

At A Glance

- Annual reviews aren't enough. Risk assessments must be updated when exposure changes.

- Unchanged risk scores raise red flags. Growth without rating movement signals weak methodology.

- Third-party risk can't sit alone. Vendor exposure must feed into enterprise risk.

- Control failures should change residual risk. Repeat findings must impact scoring.

- Risk assessment should drive strategy, not just pass exams.

Why Banking Risk Assessments Are Under New Scrutiny in 2026

Supervisory tone has shifted. Risk governance is no longer reviewed in isolation. It is evaluated against liquidity stress, third-party exposure, cyber events, and operational resilience.

The FDIC identified operational, cyber, and third-party risks as ongoing areas of supervisory focus for financial institutions. That focus has intensified as banks expand digital services and fintech partnerships. Regulators are no longer satisfied with static documentation.

They expect risk identification to evolve with business activity.

The Federal Reserve has reinforced these expectations through ongoing examination guidance on enterprise risk management and board oversight. Examiners increasingly test whether risk assessments:

- Reflect current product and service complexity

- Incorporate vendor and fintech dependencies

- Align with control testing results

- Translate into board-level reporting and decision-making

In practical terms, that means a banking risk assessment must function as a living governance tool. If inherent risk ratings remain unchanged year after year despite growth or new exposures, examiners interpret that as weak risk sensitivity.

The scrutiny in 2026 is not about whether a document exists. It is about whether the methodology adapts, connects to remediation activity, and informs strategic oversight.

Let's see what a banking risk assessment is intended to accomplish and where many institutions quietly fall short.

What a Banking Risk Assessment Is Supposed to Do (But Often Doesn't)

At its core, a banking risk assessment is meant to answer one question: Where is the institution most exposed, and are controls strong enough to manage that exposure?

Done correctly, it should:

- Identify inherent risk across business lines

- Evaluate the effectiveness of existing controls

- Determine residual risk after mitigation

- Inform resource allocation and internal audit focus

- Provide the board with a clear view of emerging threats

That is the theory.

In practice, many institutions reduce the process to a spreadsheet exercise. Risk categories are scored annually. Ratings change infrequently. Control effectiveness is assumed rather than tested. The output is a document prepared for examiners, not a tool for leadership.

This disconnect shows up in three ways:

- Risk assessments disconnected from growth. New products, expanded digital channels, or fintech integrations do not materially shift inherent risk scores.

- Control testing not feeding back into risk ratings. Findings are logged, but the underlying risk score remains unchanged.

- Board reporting that lacks forward-looking insight. Reports summarize past metrics instead of identifying risk velocity or emerging concentration.

A banking risk assessment should serve as a decision-making framework. When it does not, regulators interpret that as governance weakness.

Also Read: Risk-Based Approach for Better Risk Management in Business

Next, let's examine the specific blind spots U.S. banks continue to miss in 2026, even when a formal risk assessment framework is in place.

The 5 Things U.S. Banks Still Miss in 2026

Most institutions can produce a documented banking risk assessment on request. The issue is not completion. It is calibration.

Below are the five gaps examiners continue to identify across U.S. financial institutions.

1. Risk Scores That Don't Reflect Product Complexity

Banks expand digital channels, integrate fintech partners, or introduce new lending models, yet inherent risk ratings remain stable year over year.

If the operating model changes but the risk profile does not, examiners question the methodology's sensitivity. A banking risk assessment must evolve alongside product, customer, and geographic exposure.

2. Weak Integration Between Risk Assessment & Issue Management

Findings from internal audit, compliance testing, or regulatory exams often sit in separate tracking systems.

- When repeated issues occur without impacting residual risk ratings, it signals a disconnect between control effectiveness and risk scoring.

- The risk assessment should be adjusted when remediation lags or controls fail.

3. Third-Party and Fintech Risk Viewed in Isolation

Under the interagency third-party guidance, regulators expect banks to understand how vendor and fintech exposure affects enterprise risk.

- Yet many institutions assess vendor risk separately from the core banking risk assessment.

- That fragmentation hides concentration and operational dependency risk.

In 2026, examiners increasingly evaluate whether third-party exposure is integrated into enterprise-level risk ratings.

4. Board Reporting That Lacks Forward-Looking Indicators

Risk reports often summarize historical metrics, including the number of alerts, complaints, and incidents.

What boards need and regulators expect is insight into risk velocity.

- Is the inherent risk increasing?

- Are controls weakening?

- Is vendor concentration rising?

A banking risk assessment should be forward-looking, not just a historical summary.

5. Static Annual Review Cycles

Annual refresh cycles were acceptable when business models moved slowly.

- Today, digital banking expansion, cyber threats, and fintech partnerships introduce risk changes quarterly, sometimes monthly.

- If risk assessments are updated only once per year, the framework lags reality.

Supervisors now test whether institutions have interim reassessment triggers tied to product launches, vendor changes, or material incidents.

These gaps rarely appear dramatic in isolation. Together, they undermine the credibility of the banking risk assessment framework.

Fraxtional works with financial institutions to recalibrate banking risk assessment frameworks so scoring reflects real exposure and control performance. If your current ratings would be difficult to defend in an exam walkthrough, contact us, and we will help you strengthen the structure before regulators do.

Let's see how regulators actually evaluate risk assessments during examinations and what evidence they look for beyond the document itself.

How Regulators Actually Evaluate Banking Risk Assessments

Examiners do not start by asking for your risk matrix. They start by asking whether it works.

During supervisory reviews, regulators assess more than the existence of a banking risk assessment. They evaluate whether it is credible, integrated, and actively used in governance.

Here is what they typically test.

1) Methodology Transparency

Examiners review how inherent risk is defined, how scoring is determined, and how residual risk is calculated. If ratings appear subjective or inconsistent across business lines, credibility weakens.

Clear documentation of scoring criteria and weighting matters.

2) Alignment With Actual Operations

Regulators compare the risk assessment to real activity:

- New product launches

- Vendor onboarding

- Geographic expansion

- Technology changes

If operational complexity increases but risk ratings remain static, examiners question whether the framework is sensitive to change.

3) Integration With Control Testing

A credible banking risk assessment reflects the performance of controls.

Supervisors often trace internal audit findings, compliance testing results, or issue management logs back to the risk assessment. If repeated control failures do not impact residual risk ratings, that disconnect becomes a finding.

4) Evidence of Ongoing Monitoring

Under current supervisory expectations, risk assessment is not annual paperwork. Examiners look for:

- Interim updates tied to material events

- Documentation of management review

- Board reporting linked to risk rating changes

A static annual refresh suggests limited governance maturity.

5) Board and Senior Management Oversight

Finally, regulators assess whether leadership understands the risk profile.

Board minutes, reporting packages, and executive discussions are reviewed to determine if the banking risk assessment informs decision-making. If leadership cannot articulate the top risks or emerging exposures, examiners interpret this as a weakness.

In short, regulators evaluate whether the risk assessment functions as governance infrastructure rather than merely as compliance documentation.

Next, let's outline how to build a banking risk assessment framework to reduce exam findings and strengthen institutional resilience.

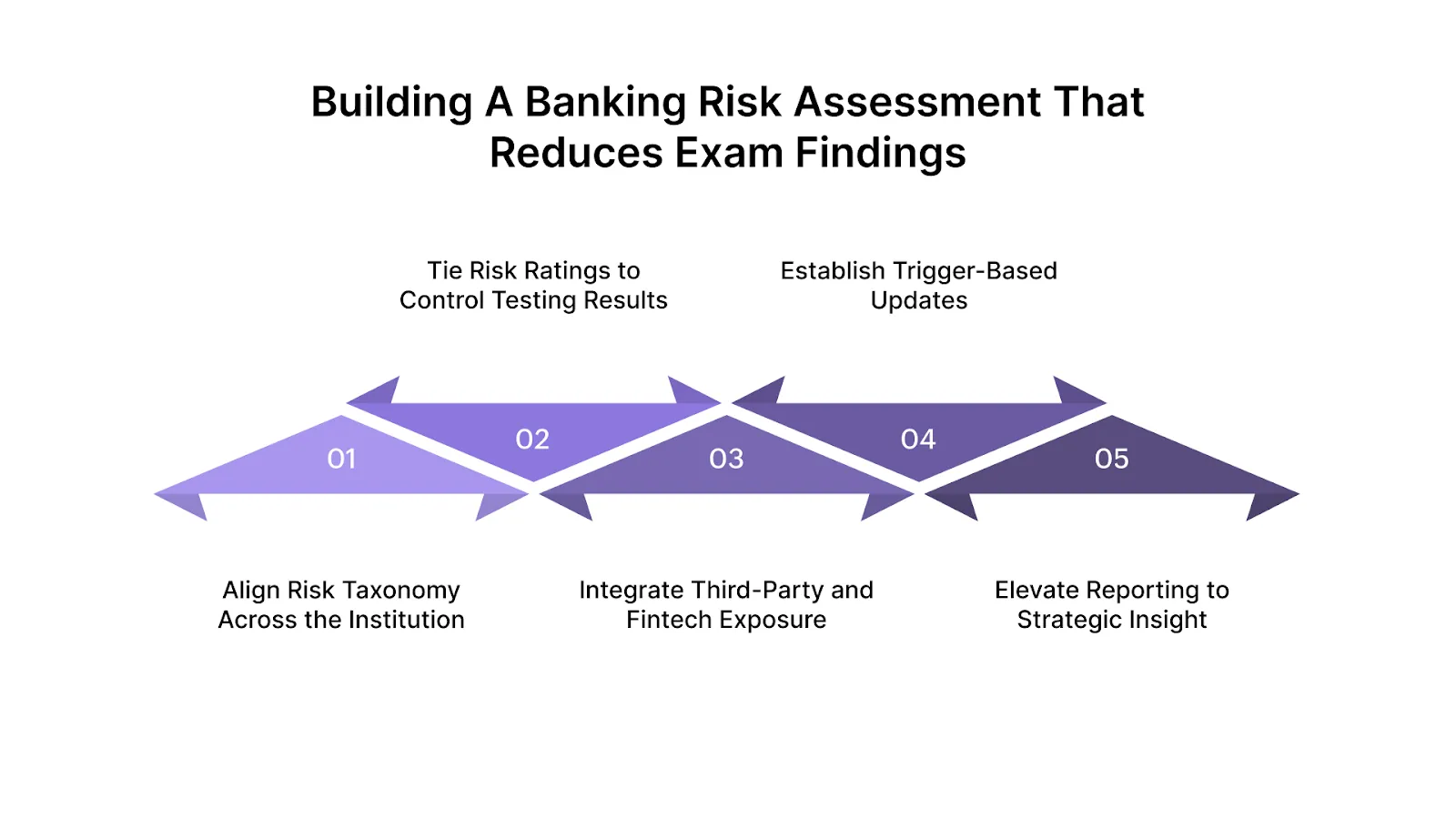

Building a Banking Risk Assessment That Reduces Exam Findings

If a banking risk assessment produces repeated findings, the issue is rarely formatting. It is structured.

Below is a practical framework U.S. financial institutions can implement to strengthen credibility and reduce supervisory friction.

Step 1: Align Risk Taxonomy Across the Institution

Risk categories should be consistent across compliance, credit, operations, IT, and third-party oversight.

When departments use different definitions or scoring scales, enterprise risk becomes fragmented. A unified taxonomy ensures inherent and residual risk ratings are comparable and defensible.

Step 2: Tie Risk Ratings to Control Testing Results

Risk scores should adjust when control performance changes.

If the internal audit identifies recurring weaknesses or remediation timelines extend, the residual risk must reflect that exposure. Static ratings despite control failures undermine confidence in the framework.

Step 3: Integrate Third-Party and Fintech Exposure

Under current U.S. supervisory guidance, vendor and fintech dependencies cannot be excluded from enterprise risk.

Critical third-party relationships should influence operational, compliance, and concentration risk ratings. Integration prevents blind spots and demonstrates lifecycle oversight.

Step 4: Establish Trigger-Based Updates

Annual updates are insufficient in dynamic operating environments.

Create documented triggers that require reassessment when:

- A new product launches

- A critical vendor is onboarded or terminated

- A significant incident occurs

- Transaction volume materially increases

This keeps the banking risk assessment aligned with real-time exposure.

Step 5: Elevate Reporting to Strategic Insight

Board reporting should answer forward-looking questions:

- Where is inherent risk trending upward?

- Which controls are under pressure?

- What emerging exposures require resource allocation?

When reporting moves beyond historical summaries, governance strengthens.

Implementing trigger-based updates, integrated vendor scoring, and board-level reporting requires more than policy updates. It requires execution discipline.

Fraxtional partners with internal risk and compliance teams to redesign banking risk assessment processes so they move from static spreadsheets to defensible governance tools. If your current framework feels fragmented, schedule a call with us, and we can help you operationalize it correctly.

Now, let's see when financial institutions benefit from strengthening their risk assessment framework with external leadership support.

When Financial Institutions Need External Risk Leadership

A banking risk assessment often breaks down at inflection points, when exposure changes faster than governance can keep up. That matters because regulators have explicitly tied risk expectations to the full lifecycle of third-party relationships.

And the risk environment isn't theoretical. In the FDIC's Quarterly Banking Profile (Q3 2024), the number of banks on the FDIC "Problem Bank List" increased to 68, with $87.3B in total assets held by problem banks.

Below are the situations in which external risk leadership is most practical.

1) Rapid growth or business model change

If product scope, transaction volume, or delivery channels expand quickly, annual scoring cycles can lag reality. That's when risk ratings stay "stable" even as exposure changes.

External support helps recalibrate methodology, weighting, and refresh triggers to ensure the banking risk assessment aligns with current operations.

2) Rising third-party and fintech dependency

Operational and cyber risk increasingly includes third parties. Ransomware and supply-chain attacks threaten banks and their third parties, underscoring that vendor dependencies cannot be isolated from enterprise risk.

This is where banks often need help integrating vendor and fintech exposure into core risk scoring.

3) Pre-exam remediation or repeat findings

If issues recur across exam cycles, regulators expect structural change, not new wording. External risk leadership is useful when you need to connect control testing results, issue management, and residual risk ratings in a defensible way.

4) M&A, conversions, or major vendor change

Large transitions introduce control gaps and data inconsistencies. A refreshed banking risk assessment is often needed to reflect combined exposure and show active oversight.

5) Board and executive turnover

If leadership cannot clearly explain top risks, drivers, and trend direction, the problem is usually framework design and reporting quality, not effort.

External risk leadership is not about outsourcing responsibility. It is about strengthening methodology, alignment, and oversight at moments when exposure increases.

How Fraxtional Strengthens Banking Risk Assessments

A banking risk assessment fails when it becomes a scoring exercise instead of a governance tool.

Fraxtional operates at the point where risk data must translate into defensible oversight.

Our fractional Chief Risk and Compliance Officers work alongside internal risk, compliance, and audit teams to recalibrate methodology, align scoring with control performance, and ensure enterprise risk reflects real operational exposure.

We focus on what regulators actually test.

Every engagement begins with clarity:

- Mapping inherent and residual risk to actual product, vendor, and geographic exposure

- Aligning risk scoring with internal audit and compliance testing results

- Integrating third-party and fintech dependencies into enterprise risk ratings

- Elevating board reporting from static summaries to forward-looking insight

The objective is not to add documentation. It is to strengthen the structure.

Turn risk scoring into strategic oversight. Partner with Fraxtional to build a risk assessment framework that stands up to scrutiny and evolves with your institution's growth.

Conclusion

A banking risk assessment should do more than satisfy an exam request. It should shape how an institution understands its exposure, allocates resources, and informs its board.

In 2026, regulators are not questioning whether banks complete risk assessments. They are questioning whether those assessments reflect real operational complexity, third-party dependency, and control performance.

Static scoring models and annual refresh cycles are no longer enough.

Institutions that avoid repeat findings treat risk assessment as governance infrastructure, not documentation. They recalibrate risk when exposure changes. They integrate vendor and fintech dependencies into enterprise scoring. They ensure board reporting highlights emerging risk, not just historical metrics.

That level of alignment rarely happens by accident.

Fraxtional works with financial institutions to redesign banking risk assessment frameworks so they withstand supervisory review and support strategic decision-making. If your current framework feels static, disconnected, or overly reactive during exams, it may be time to rebuild it with a more structured approach.

Reach out to us today to strengthen your banking risk assessment before regulators test it.

FAQs

At a minimum, banks conduct a formal annual update. However, regulators expect interim reassessments when material events occur, such as new product launches, significant vendor changes, mergers, or major control failures.

Inherent risk is the level of risk before controls are applied. Residual risk reflects the remaining exposure after evaluating the effectiveness of mitigation controls. Regulators assess whether residual risk ratings realistically reflect control performance.

The framework should be proportional to size and complexity. However, regulatory expectations around lifecycle risk management, third-party oversight, and board reporting apply to community banks as well, even if the methodology is scaled.

Critical vendors and fintech partners can materially affect operational, compliance, and concentration risk. Regulators expect banks to incorporate significant third-party exposure directly into enterprise risk scoring, rather than assessing it in isolation.

Examiners typically evaluate methodology clarity, alignment with actual operations, integration with audit findings, responsiveness to change, and evidence that senior management and the board actively use the assessment in decision-making.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.

Now Accepting:

BTC

ETH

USDC

USDP