Feb 18, 2026

Fractional Transformation Executive: 5 Proven Crisis Moves for U.S. FinTech Leaders

By Fraxtional LLC

Summarize the blog with AI

U.S. FinTech is growing fast, but the margin for error is shrinking.

The global FinTech market is projected to expand by more than $800 billion between 2025 and 2029. This reflects the scale and speed of change across payments, lending, and embedded finance. At the same time, regulatory pressure is intensifying.

For founders and boards, this creates real crisis risk. A delayed exam response, weak risk reporting, or breakdown in sponsor bank trust can stall funding, freeze partnerships, or trigger regulatory scrutiny.

This is where a fractional transformation executive becomes strategically valuable. Instead of waiting months to hire full-time leadership, firms can deploy experienced executive oversight immediately to stabilize governance, align risk controls, and reset execution.

This article outlines five proven crisis moves U.S. FinTech leaders can activate through fractional business leadership to protect continuity, restore confidence, and turn instability into structured transformation.

Key Takeaways

- Most FinTech crises stem from weak governance, not bad products. Sponsor bank pressure and AML scrutiny escalate when ownership and reporting lack structure.

- A fractional transformation executive brings immediate authority and execution. This is embedded leadership, not advisory support.

- The first 30 days matter most. Rapid exposure mapping and tracked remediation reduce regulatory and partnership risk.

- Sponsor bank trust depends on documented oversight. Clear governance cadence and defensible controls prevent costly slowdowns.

- Fraxtional delivers structured crisis leadership without permanent overhead. Executive-grade transformation, deployed when it matters most.

What Is a Fractional Transformation Executive & Why It Matters in Crisis

A fractional transformation executive is a senior leader brought in on a part-time or time-bound basis to drive structural change during high-stakes periods. Unlike a traditional consultant who advises from the outside, this role operates inside the leadership team, with decision-making authority and accountability.

In stable periods, fractional business leadership is often used to guide scaling, cost optimization, or system upgrades. In a crisis, the mandate shifts. The focus becomes containment, stabilization, and rapid alignment across risk, operations, and stakeholder communication.

For U.S. FinTech firms, a crisis rarely looks dramatic at first. It often starts with subtle warning signs:

- A sponsor bank requesting enhanced oversight documentation

- Gaps flagged in an internal audit

- Delays in money transmitter licensing approvals

- Investor pressure tied to compliance maturity

Left unaddressed, these signals compound. Regulatory scrutiny increases. Partner confidence weakens. Growth slows.

This is where the role of fractional executives in crisis management becomes distinct.

Compared to hiring a full-time executive, which can take three to six months, a fractional transformation executive can step in immediately, assess risk exposure within weeks, and implement corrective frameworks without long-term overhead.

For FinTech boards and founders, that speed is not a convenience. In a regulated environment, it is often the difference between temporary turbulence and sustained disruption.

Suggested Read: Why Banks Are Replacing Full-Time Executives With Fractional Leaders in 2026

The Crisis Reality for U.S. FinTech Leaders

Crisis in FinTech rarely announces itself. It builds quietly at the intersection of regulation, liquidity, and partner oversight.

In the United States, FinTech firms operate within a layered framework that includes FinCEN oversight under the Bank Secrecy Act (BSA), state-level money-transmitter licensing requirements, and heightened scrutiny by sponsor banks.

In recent years, federal regulators have issued enforcement actions and consent orders related to third-party risk management and AML deficiencies.

This signals that fintech-bank partnerships are under closer scrutiny. For early and growth-stage firms, this creates three recurring pressure points:

- Sponsor Bank Escalations

Sponsor banks are expected to maintain effective oversight of fintech partners. When documentation, transaction monitoring, or governance controls fall short, banks often respond with heightened reviews, remediation demands, or slowed product approvals. - Licensing and Regulatory Delays

Money transmitter license applications can stall if compliance programs are not yet mature. Even minor documentation gaps can extend approval timelines by months, affecting expansion plans and investor timelines. - Investor and Board Pressure

During funding slowdowns or market volatility, investors scrutinize risk exposure more aggressively. Weak compliance reporting or unclear risk ownership can quickly erode confidence.

These are not theoretical risks. They are operational realities for U.S. FinTech firms trying to scale.

If your leadership team is still under pressure from the sponsor bank or regulatory escalation, this is the point at which structure matters more than speed.

Fraxtional deploys experienced fractional transformation executives who embed directly into your team to restore governance clarity and execution control. Schedule a call with us today!

The Role of Fractional Executives in Crisis Management

When a FinTech enters a high-pressure cycle, leadership gaps become visible fast. Decision rights blur. Risk reporting lags. Board updates become reactive rather than strategic.

This is where the role of fractional executives in crisis management becomes materially different from traditional advisory support.

A consultant typically delivers recommendations. An interim executive may stabilize operations. A fractional transformation executive, however, is charged with realigning structure, governance, and execution at the leadership level.

In crisis settings, that role centers on three priorities:

1. Immediate Risk Clarity

Within the first weeks, the executive maps control gaps, regulatory exposure, sponsor bank dependencies, and reporting weaknesses. The goal is not documentation for its own sake. It is decision-grade visibility.

2. Governance Reset

Crisis often reveals unclear accountability across compliance, operations, and product teams. Fractional business leadership establishes defined ownership, escalation channels, and board reporting cadence to prevent further drift.

3. Accelerated Execution Without Overhead

Hiring a full-time C-suite executive can take months. Crisis response cannot. A fractional transformation executive steps in quickly, implements structured remediation plans, and scales involvement based on urgency.

For U.S. FinTech leaders, this model strikes a balance between speed and authority. It provides executive-level oversight without long-term hiring friction, while maintaining alignment with regulatory expectations and investor scrutiny.

In short, the role is not to "assist" during turbulence. It is to create a controlled transformation while pressure is highest.

Let's move from structure to action: the proven crisis moves that define effective fractional leadership in regulated FinTech environments.

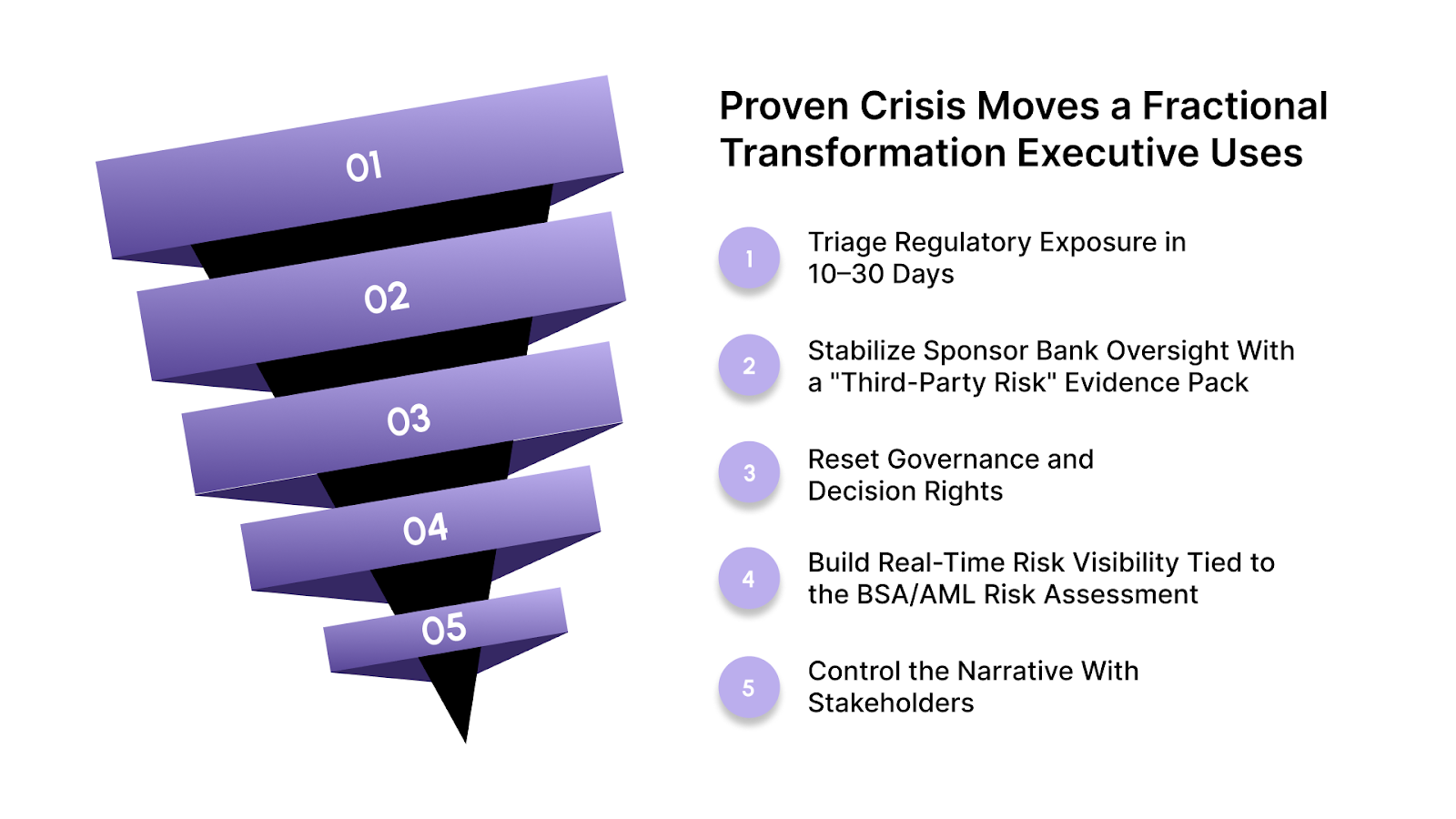

5 Proven Crisis Moves a Fractional Transformation Executive Uses

In U.S. FinTech, "crisis" usually means a breakdown in trust: with a sponsor bank, regulators, or investors. The fastest way to rebuild that trust is to demonstrate disciplined governance, clear risk management, and documented controls.

Below are five moves a fractional transformation executive drives when the clock is running.

1) Triage Regulatory Exposure in 10–30 Days

The first job is to establish decision-grade clarity: what can trigger enforcement risk, bank escalation, or investor concern.

A practical triage focuses on the same fundamentals that examiners look for: policies, procedures, and processes for identifying, evaluating, and reporting suspicious activity, along with the end-to-end SAR workflow and escalation path.

Why this matters now:

U.S. enforcement outcomes are not theoretical. FinCEN has assessed headline civil penalties and imposed multi-year monitorships, including a $1.3B penalty against TD Bank (with an independent monitorship) and a $3.4B civil penalty in the Binance matter.

What the executive does immediately

- Map the BSA/AML control stack: monitoring, alert QA, investigations, SAR decisioning, filing timeliness, and documentation.

- Identify the "high-consequence gaps” that banks and regulators address most quickly (ownership, evidence, timeliness).

- Produce a short remediation plan with owners, timelines, and proof artifacts.

2) Stabilize Sponsor Bank Oversight With a "Third-Party Risk" Evidence Pack

When sponsor banks become nervous, they request proof. The most effective response is a structured evidence pack aligned to the interagency third-party risk management lifecycle: planning, due diligence, contract structuring, ongoing monitoring, and termination/contingency planning.

This is exactly the lens through which banks are supervised when managing fintech relationships.

What the executive builds (fast)

- A clean operating model: who owns compliance, who approves changes, who escalates incidents.

- Monitoring artifacts: control testing, issue logs, corrective actions, and status reporting.

- A "bank-ready narrative": current state, gaps, remediation timeline, and how oversight is sustained.

Outcome: fewer ad-hoc bank requests, fewer surprises, faster re-approval cycles.

3) Reset Governance and Decision Rights (So Crisis Doesn't Multiply)

Crisis becomes expensive when accountability is unclear. In FinTech, that usually shows up as:

- Compliance vs product disagreements

- No defined escalation thresholds

- Board updates that are descriptive but not actionable

A fractional transformation executive sets a crisis-governance cadence that aligns with what regulated partners expect: owners, escalation rules, reporting rhythm, and documented decisions.

What changes in practice

- A weekly risk committee with named owners and tracked actions.

- A decision matrix: what requires compliance sign-off, what requires bank notice, what requires board notification.

- A single source of truth for remediation and evidence.

This is fractional business leadership doing what founders often don't have time to operationalize under pressure.

4) Build Real-Time Risk Visibility Tied to the BSA/AML Risk Assessment

In many fintechs, data exists but doesn't translate into visibility. Examiners and partner banks care whether monitoring is risk-based and anchored to an explicit risk assessment.

So the move here is not "dashboards for dashboards' sake." It's a short list of KRIs that connect: Risk assessment → monitoring priorities → alerts → investigations → SAR decisions → remediation

What the executive implements

- A compact KRI set (e.g., alert volumes, QA fail rates, SAR timeliness, backlog age, high-risk typologies).

- A "red/yellow/green" escalation system tied to thresholds.

- Board-ready reporting that shows trendlines and action, not noise.

5) Control the Narrative With Stakeholders (Board, Bank, Investors)

In regulated industries, silence reads as disorder.

This move is about communicating like a mature operator: transparent, measured, and evidence-based. When firms show structured remediation with clear milestones, they reduce uncertainty for:

- sponsor banks (partnership risk)

- investors (downside risk)

- boards (governance risk)

What the executive standardizes

- A weekly status brief: what changed, what's controlled, what's pending, what's next.

- Bank updates aligned to third-party oversight expectations.

- Board updates that connect risk posture to business impact (launches, markets, funding readiness).

Each of these five moves reflects the practical reality of fractional business leadership in regulated markets. They are not theoretical best practices. They are targeted interventions designed for U.S. FinTech firms operating under real supervisory scrutiny.

Next, let's examine the measurable organizational impact of these crisis moves on founders, boards, and investors.

What These Crisis Moves Deliver for U.S. FinTech Leaders

Crisis containment is the short-term goal. Structural resilience is the long-term outcome.

When a fractional transformation executive executes the five moves above, the impact is measurable across three areas that matter most to U.S. FinTech leaders: regulatory posture, sponsor bank confidence, and investor credibility.

1. Reduced Enforcement and Examination Risk

Federal regulators have made clear that risk-based compliance programs must be demonstrable, documented, and continuously monitored. Effective internal controls, independent testing, and board oversight are the core pillars of compliance.

When governance resets and real-time visibility frameworks are implemented, firms move from reactive remediation to structured oversight. That materially lowers the probability of Matters Requiring Attention (MRAs), supervisory findings, or enforcement escalation.

The outcome is not perfection. It is defensibility.

2. Faster Sponsor Bank Alignment and Fewer Operational Pauses

Banks are expected to conduct ongoing monitoring of fintech partners throughout the relationship lifecycle.

If a fintech cannot clearly demonstrate controls, monitoring, and remediation tracking, banks are obligated to slow expansion or impose corrective plans.

After structured crisis intervention:

- Evidence requests become predictable instead of urgent

- Documentation cycles shorten

- Product launches face fewer compliance-driven delays

For fintech firms dependent on sponsor bank infrastructure, this directly protects revenue continuity.

3. Stronger Board and Investor Confidence

During market volatility, investors prioritize downside protection. Governance maturity becomes part of the valuation logic.

When boards receive:

- Defined risk dashboards

- Escalation matrices

- Clear remediation timelines

- Control testing documentation

They can make informed, strategic decisions rather than operate in uncertainty.

For private equity and late-stage investors, visible governance discipline reduces diligence friction. It signals operational maturity aligned with federal supervisory expectations.

4. Strategic Flexibility Without Permanent Cost Expansion

Hiring a full-time transformation leader can take months and significantly increase fixed overhead. In contrast, fractional business leadership provides executive-grade oversight calibrated to the severity of the crisis.

That flexibility matters in a capital-constrained environment.

Leadership gains:

- Immediate expertise

- Structured transformation

- Controlled cost exposure

- Scalable involvement as stability returns

The role of fractional executives in crisis management is not simply to "fix compliance." It is to convert regulatory pressure into operational clarity. Crisis becomes a controlled transformation phase rather than a destabilizing event.

Also Read: Top 5 GigX Alternatives for Fractional Executives

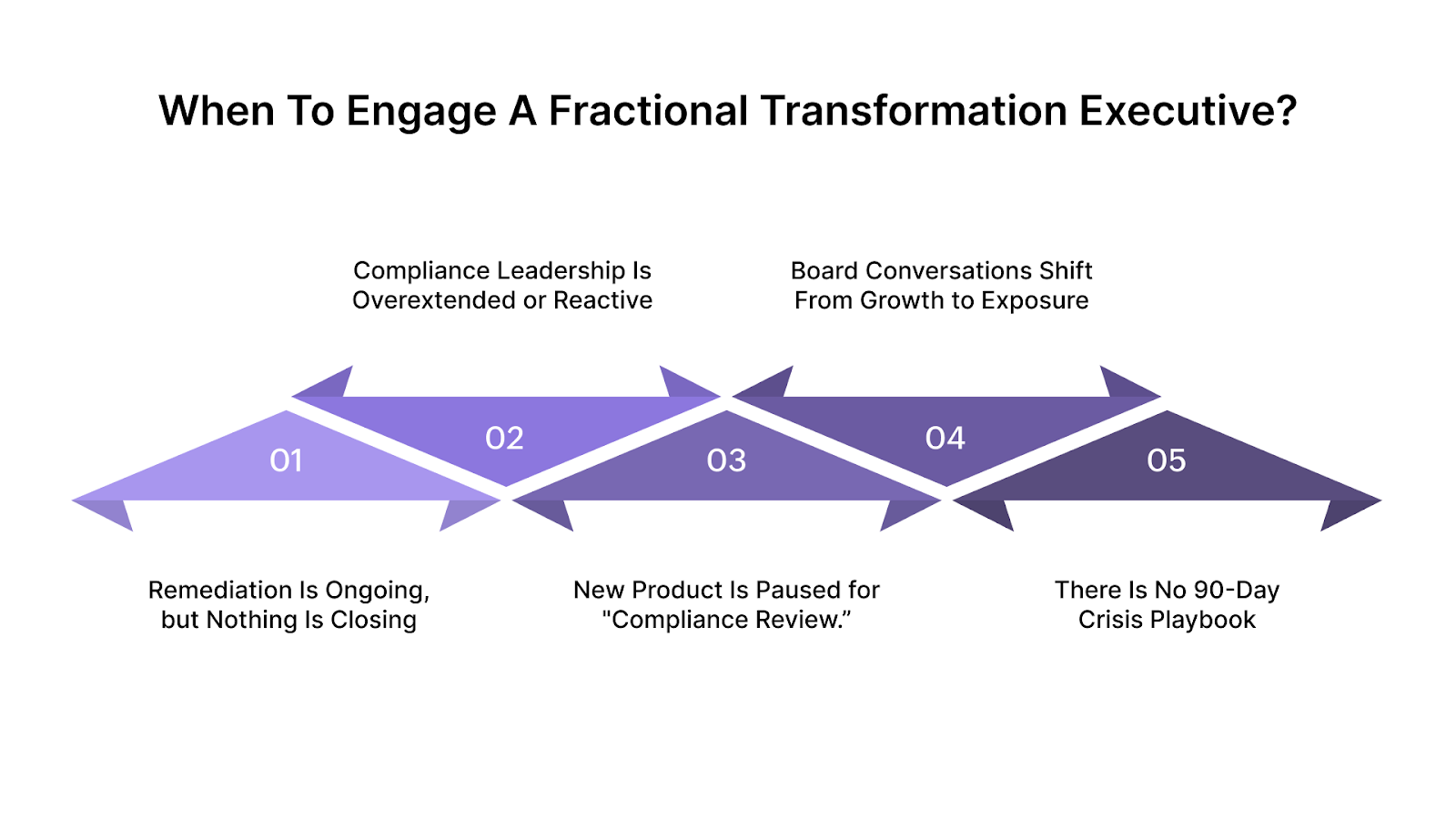

When to Engage a Fractional Transformation Executive (Trigger Points)

The right time to engage a fractional transformation executive is not when enforcement hits. It is when structural strain becomes visible.

Here are sharper, board-level signals that action is warranted.

1. Remediation Is Ongoing, but Nothing Is Closing

If audit findings, QA failures, or bank action items remain open across multiple reporting cycles, the issue is not effort. It is ownership and execution architecture.

Regulators expect documented corrective action tracking with defined accountability. When remediation lists grow rather than shrink, the governance structure needs intervention, not more staff.

2. Compliance Leadership Is Overextended or Reactive

In many growth-stage FinTech firms, one senior compliance leader manages AML oversight, licensing, and bank communications

When that role becomes primarily reactive, strategic transformation stalls. A fractional transformation executive restores separation between operational firefighting and structural reform.

3. New Product or Market Expansion Is Paused for "Compliance Review.”

If launches are delayed because compliance cannot sign off with confidence, that signals misalignment between product velocity and control maturity.

This is a transformation trigger. Without a structured governance reset, every expansion cycle will repeat the same friction.

4. Board Conversations Shift From Growth to Exposure

When board discussions increasingly center on regulatory downside, sponsor bank dependency, or enforcement headlines, confidence is already weakening.

At that stage, fractional business leadership provides structured clarity before risk perception impacts valuation or partnership leverage.

5. There Is No 90-Day Crisis Playbook

If leadership cannot clearly answer:

- What would happen if the sponsor bank imposed enhanced oversight tomorrow?

- Who owns the SAR backlog reduction?

- How quickly can we produce regulator-ready evidence?

Then, resilience is assumed rather than engineered.

If your team cannot clearly articulate a 90-day crisis response framework, that gap will surface under scrutiny.

Fraxtional builds structured crisis playbooks that align compliance, product, and executive leadership under one accountable framework. Reach out to us today and engage before external pressure forces reactive change.

How Fraxtional Turns Crisis Into Structured Transformation

Crisis management in FinTech is not about adding more reports. It is about installing leadership discipline where pressure is highest.

Fraxtional operates at the intersection of regulatory exposure, sponsor bank scrutiny, and investor oversight. Our fractional transformation executives step into active leadership roles during high-stakes moments. They do not replace internal teams. They align them.

Every engagement begins with precision:

- Mapping regulatory exposure across BSA/AML controls, licensing status, and third-party dependencies

- Stress-testing sponsor bank oversight expectations against the current governance structure

- Clarifying decision rights across compliance, product, and executive leadership

- Converting remediation backlogs into tracked, board-visible action plans

From there, the focus shifts to execution.

Fraxtional embeds structured risk cadence into leadership routines, ensuring reporting is measurable, defensible, and aligned with federal supervisory expectations. We translate operational fixes into narratives that sponsor banks and investors recognize as credible.

The outcome is not short-term damage control. It is a controlled transformation. Try it out yourself today!

Conclusion

A crisis does not test software. It tests leadership.

Dashboards can surface anomalies. Audit tools can generate reports. But when a sponsor bank escalates oversight or regulators question controls, what matters is executive accountability. Someone must interpret the data, defend the framework, and own the response.

That is where a fractional transformation executive becomes decisive.

In regulated U.S. FinTech markets, credibility depends on governance that is structured, visible, and defensible. Fractional business leadership provides the structure without slowing growth or creating permanent overhead.

Automation improves efficiency. Documentation proves activity.

Executive oversight builds trust.

Fraxtional delivers that leadership when it matters most. Our fractional transformation executives embed directly into your organization to stabilize governance, restore partner confidence, and convert crisis into controlled transformation.

If your FinTech is facing escalating oversight or structural strain, partner with Fraxtional and formalize leadership architecture.

FAQs

A consultant advises and exits. A fractional transformation executive holds decision authority, embeds within leadership, and drives execution. The difference is accountability, not recommendations.

Yes, if structured properly. Regulators and banks care about documented oversight, clear ownership, and defensible controls. A fractional executive provides named accountability and governance discipline.

It usually includes regulatory exposure assessment, governance reset, remediation tracking, and sponsor bank alignment. The goal is measurable stabilization, not just policy updates.

Yes, especially pre-Series A or growth-stage firms that cannot justify a full-time executive but face licensing, AML, or sponsor bank pressure. It adds senior oversight without permanent cost.

Through reduced remediation backlog, improved reporting clarity, sponsor bank feedback, and defined risk KPIs. Effectiveness is reflected in governance structure, not just in documentation volume.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.