Feb 23, 2026

Internal Audit Checklist: A 2026 Guide for Founders and Boards

By Fraxtional LLC

Summarize the blog with AI

You’ve built processes, hired key leaders, and raised capital, yet some risks still lurk in plain sight. For many startup founders, boards, and risk leaders in fintech, crypto, and banking, the real pain is the hidden control weaknesses that only surface when an investor, sponsor bank, or regulator asks for evidence and you’re under the clock.

That moment of panic, when your team scrambles to find documentation or explain control failures, isn’t just embarrassing; it can delay deals, erode trust, and stall growth. This isn’t hypothetical. Research shows that effective internal audit functions significantly improve risk management and decision-making performance because they help companies detect, assess, and mitigate risks before they escalate.

In this blog, we will walk you through what an internal audit checklist really means for a scaling company, why the checklist matters, and how to make it actionable for founders, boards, and risk leaders.

Key Takeaways

- An internal audit checklist gives founders, boards, and risk leaders early visibility into operational, financial, and compliance risks before investors, banks, or regulators raise concerns.

- Audit expectations increase rapidly after Seed and Series A, making risk-based internal audits essential to avoid diligence delays and credibility issues.

- Effective internal audits focus on executed evidence, clear ownership, and consistent controls, not perfect or overly complex documentation.

- Structuring the checklist by key risk areas keeps audits practical, targeted, and aligned with business growth rather than slowing teams down.

- Fraxtional’s risk and compliance leadership helps companies right-size audit scope, strengthen controls that matter, and stay audit-ready without the cost of full-time executives.

Why Internal Audit Checklists Matter for Scaling Companies

When you’re building fast, internal audits rarely feel urgent. You’re closing customers, shipping features, and managing burn. Controls feel like something you’ll “tighten later.” The problem is, risk doesn’t wait for later; it quietly compounds in everyday decisions you stop noticing.

For fintech founders, compliance leaders, bank partners, and investors, an internal audit checklist is about seeing risks early, before someone else points them out. It helps you answer uncomfortable but critical questions:

- Are controls actually working, or just documented?

- Do owners know what they’re accountable for?

- Would you be comfortable sharing this with a bank, regulator, or investor tomorrow?

Here’s why skipping this work almost always backfires:

- Investors use audit readiness as a proxy for leadership maturity, especially post-Seed and Series A. Gaps signal execution risk, not just compliance risk.

- Sponsor banks and regulators expect evidence, not intent, and missing documentation slows approvals and damages credibility.

- Poor internal audit hygiene creates hidden costs, delayed deals, extended diligence cycles, and last-minute firefighting that distracts leadership.

The “we’re still early” mindset stops working once external scrutiny begins. At that stage, internal audit checklists become less about compliance and more about protecting momentum, without needing a full-time executive team to manage them.

Also Read: Is ComplyAdvantage Better Than Fractional Officers? A Decision Guide (2026)

Knowing that internal audit checklists matter is one thing. Knowing what an internal audit actually does, and what it doesn’t, is what turns them from paperwork into a real risk management tool.

What is an Internal Audit?

Before you can use a checklist, you need clarity on what an internal audit actually does and why it matters beyond checking boxes for compliance teams.

At its core, internal audit is an independent and objective evaluation of how your company manages risk, assures controls are reliable, and keeps its operations running as intended.

Internal audit evaluates:

- Internal Controls: the rules and systems you rely on to protect assets, financial integrity, and operational consistency. These controls help make sure processes work as intended, every day, not just once.

- Risk Management Effectiveness: how well your organization identifies, assesses, and mitigates risks before they become crises or deal-breakers in diligence.

- Policy Adherence: whether documented policies are actually followed, not just stored in a folder somewhere.

Now, let us have a look at the difference between internal audit, external audit, and regulatory exam.

Internal Audit vs External Audit vs Regulatory Exam

These three reviews are often grouped together in board discussions, but they serve very different purposes. Confusing them leads to the wrong preparation, the wrong owners, and the wrong expectations, especially when scrutiny increases after Seed or Series A.

Here’s how they differ at a practical, board-level view:

With the role of internal audit defined, it’s worth looking at who actually relies on audit checklists day to day, and what they gain from them as scrutiny increases.

Who Actually Uses an Internal Audit Checklist and Why

Internal audit checklists aren’t built for auditors alone. In growing fintechs, banks, crypto firms, and PE-backed companies, they’re used by decision-makers who need clear visibility into risk, accountability, and readiness before external stakeholders start asking hard questions.

Here’s how different leadership roles use internal audit checklists for very different, but equally critical, reasons:

- Founders & CEOs: Validate controls pre-fundraising, support investor discussions, streamline negotiations, and ensure predictable operations.

- Boards & Audit Committees: Oversee risks, ensure financial integrity, track remediation, and guide strategic decisions.

- Risk & Compliance Leaders: Prioritize high-risk areas, enforce governance, measure program maturity, and provide structured evidence for the board.

- Banks, Crypto Firms & PE Firms: Demonstrate risk discipline, support diligence, maintain portfolio transparency, and ensure compliance in digital assets.

Also Read: 7 Best Strategies for Private Equity Risk Management

Understanding who relies on internal audit checklists sets the stage for execution. The next step is seeing how an internal audit actually unfolds, from scoping through remediation.

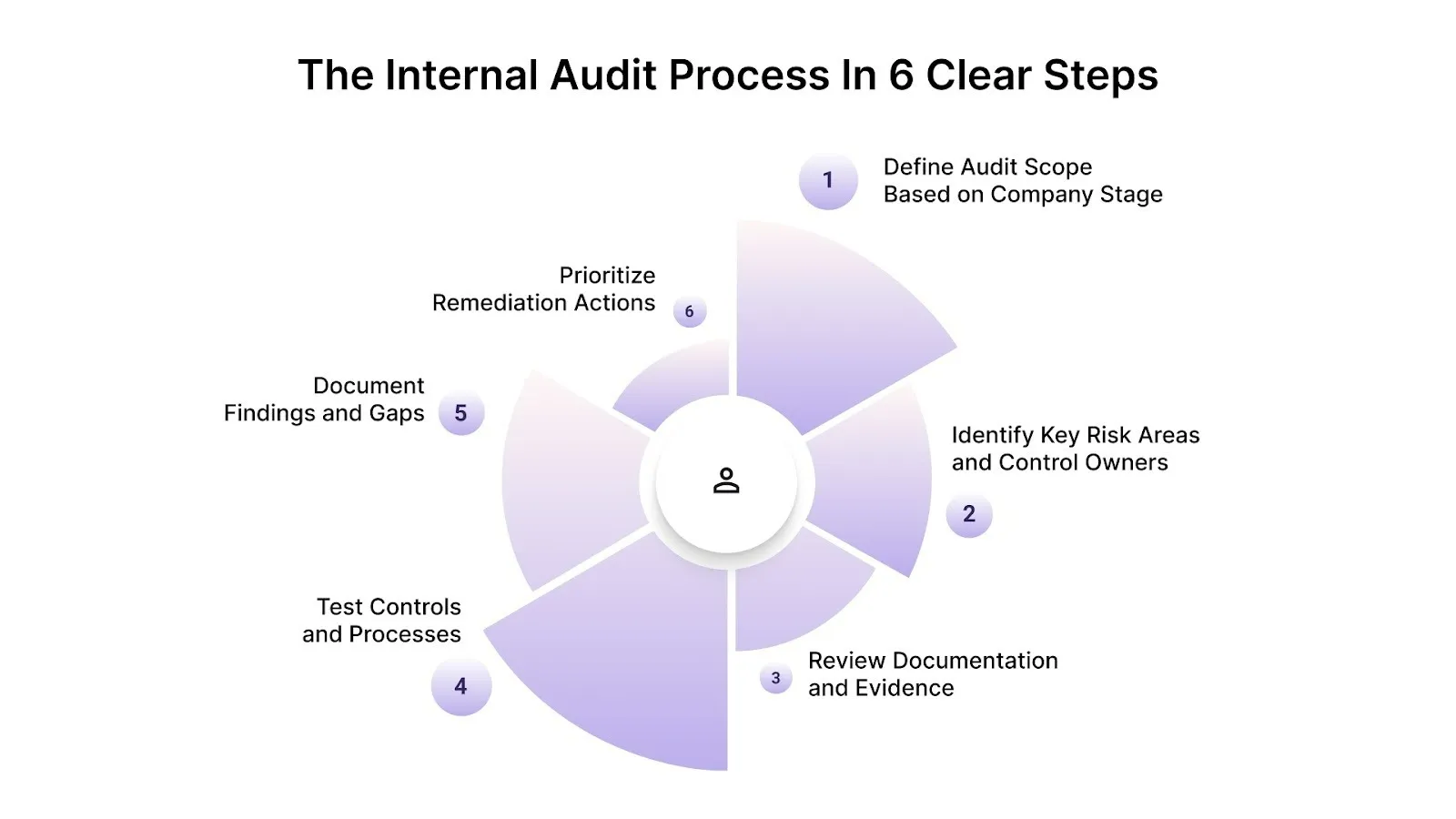

The Internal Audit Process in 6 Clear Steps

Before you enter a detailed checklist, it’s useful to understand how an internal audit actually works from start to finish. Here’s a practical, stage-aware breakdown of the internal audit process your leadership team can relate to:

- Define Audit Scope Based on Company Stage and Risk Profile: Set objectives based on your business stage (early-stage controls vs growth-stage risk areas) and map them to key risks that could derail strategic goals. A clear scope focuses limited resources on what matters most.

- Identify Key Risk Areas and Control Owners: Pinpoint where risk lives (e.g., data security, financial reporting, compliance), then assign accountable owners who understand process nuances.

- Review Documentation and Evidence: Gather policies, procedures, process flows, and artifacts that demonstrate how controls operate, not just on paper.

- Test Controls and Processes: Verify whether controls function as intended under real operational conditions, focusing testing where risk is highest.

- Document Findings and Gaps: Record actual control performance, note deviations, and distinguish between design and operating effectiveness.

- Prioritize Remediation Actions: Rank issues by risk impact and likelihood, then integrate actionable next steps into your risk management plan.

If internal audits still feel unclear or reactive, that’s often a leadership gap, not a tooling problem. Fraxtional brings experienced risk and compliance leadership to help you define the right audit scope and avoid surprises before investors or banks ask. Reach out to us to discuss what audit readiness should look like at your stage.

With the audit process in place, it’s time to move from “how” to “what.” A risk-based internal audit checklist translates process into action.

Comprehensive Internal Audit Checklist by Risk Area

A useful internal audit checklist isn’t exhaustive; it’s risk-focused. For founders, boards, and risk leaders, the goal is to review the areas most likely to disrupt growth, partnerships, or regulatory standing.

Below is a practical breakdown of internal audit focus areas leaders typically review first:

- Governance and Decision Oversight: Evidence that the board and leadership actively review risk, clearly delegate authority, manage conflicts of interest, and formally approve governance policies and charters.

- Financial Control Integrity: Controls that ensure financial data is accurate and defensible, including consistent revenue recognition, controlled expense approvals, segregation of duties, and regular reconciliations.

- Regulatory and Compliance Execution: Proof that licenses are current, policies align with applicable laws, regulatory changes are tracked, staff are trained, and compliance issues are escalated and resolved.

- Technology and Data Protection: Controls demonstrating that systems and data are protected in practice, including access management, incident response readiness, vendor security oversight, and tested backups.

- Operational and Third-Party Resilience: Assurance that critical operations can withstand disruption through vendor due diligence, enforceable SLAs, documented continuity plans, and regular testing.

Also Read: What Is Relationship Banking? A 2026 Guide for FinTech & Sponsor Banks

Now, let us have a look at what internal auditors look for during reviews.

What Internal Auditors Actually Look for During Reviews

When auditors walk into a review, they aren’t there to catch you out; they’re there to assess how reliable, consistent, and trustworthy your controls really are.

Here are the core things auditors focus on:

- Evidence Over Intention: Auditors seek documentation that shows controls were executed, not just written. For example, signed logs, dated records, and system outputs that match documented procedures.

- Consistency Over Perfection: Reliable controls are repeatable over time. One-off fixes or inconsistent execution raise flags more than minor design gaps. Auditors want to see that your processes produce the same results every cycle.

- Ownership Clarity: Clear control owners mean there’s someone accountable and auditable for each risk area. Ambiguous ownership creates gaps during reviews and slows remediation.

Once you understand what internal auditors actually look for, the focus shifts to preparation. The goal isn’t to overcorrect or slow the business down, but to align evidence, ownership, and execution with real audit expectations.

How to Prepare for an Internal Audit Without Slowing the Business

Preparing for an internal audit doesn’t have to feel like a bottleneck or a bureaucratic rewrite of everything your team does.

Below is a guide to preparing for internal audits in ways that strengthen operations and scale risk visibility without slowing execution.

- Prioritize Key Documentation: Collect evidence that shows real process execution, like approval logs, reconciliations, and control records. Use dated folders, tag owners, and retain artifacts from actual transactions.

- Rationalize Controls: Focus on controls that mitigate real risks. Avoid duplicative processes or unnecessary approvals that don’t reduce exposure.

- Align with Growth Stage: Match audit work to company maturity:

- Early-stage: document understanding of critical risks.

- Growth-stage: track executed domain-specific controls.

- Mature/PE-ready: report trends and remediation over time.

- Integrate Controls in Daily Operations: Make documentation part of routine workflows with clear ownership, standardized naming, and scheduled reviews to avoid audit sprints.

Also Read: Client Onboarding Financial Services: Risk and Control Guide

Preparation sets the foundation, but execution determines outcomes. The next section highlights the most common internal audit mistakes that turn good intentions into real risk.

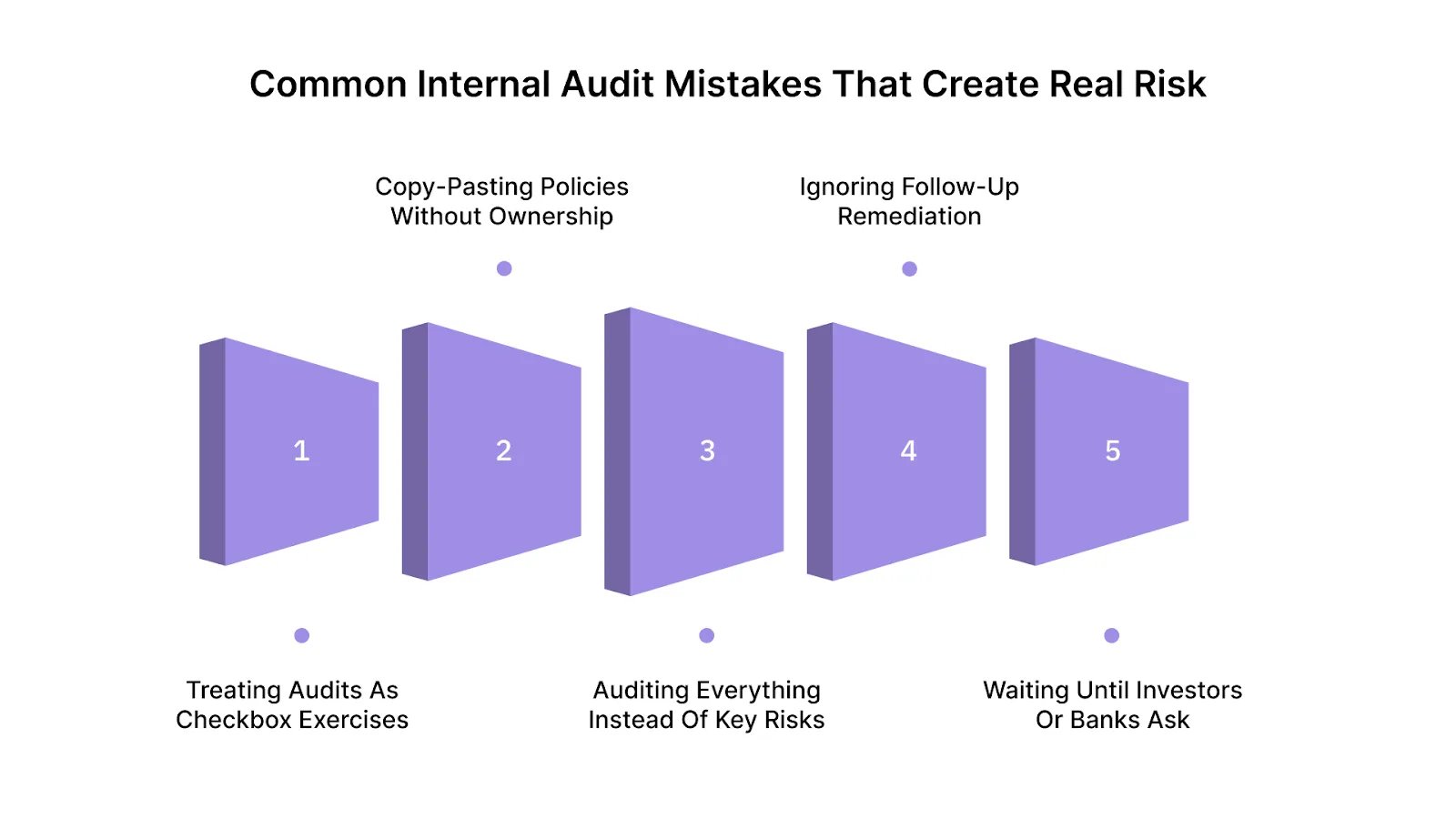

Common Internal Audit Mistakes That Create Real Risk

Below are the most common internal audit missteps leaders make, and how to fix them:

- Treating Audits as Checkbox Exercises: Controls exist on paper, but don’t reflect real operations.

- The Fix: Focus audits on how controls actually run, using executed evidence instead of templates.

- Copy-Pasting Policies Without Ownership: No one is accountable when something breaks.

- The Fix: Assign clear owners to every policy and control, with review and update responsibility.

- Auditing Everything Instead of Key Risks: Teams waste time while high-impact risks remain unchecked.

- The Fix: Scope audits around the top risks tied to revenue, data, regulation, and third parties.

- Ignoring Follow-Up Remediation: Known issues repeat, eroding trust with boards and partners.

- The Fix: Track findings with owners, timelines, and documented closure evidence.

- Waiting Until Investors or Banks Ask: Reactive audits delay deals and damage credibility.

- The Fix: Build lightweight, ongoing audit reviews aligned to growth milestones.

If audit preparation is starting to slow your team or pull focus from growth, the issue is usually how controls and priorities are being guided. Fraxtional integrates senior risk and compliance leadership so audits stay practical, focused, and aligned to your growth milestones. Contact us to explore a leadership model that fits without adding full-time overhead.

Understanding common internal audit mistakes is only useful if it informs better execution. The following example shows how a scaling fintech applies a risk-based internal audit checklist.

Realistic Internal Audit Checklist Example for a Scaling FinTech

When you’re preparing a real internal audit example, even in a hypothetical case, it helps to ground it in a company context, a focused scope, and clear outcomes rather than generic steps.

Here’s a practical illustration of how a scaling U.S.-based fintech might approach an internal audit to strengthen risk visibility without overwhelming teams.

- Company Profile: Early-growth fintech (Series B), headquartered in the U.S., offering digital payments and compliance-sensitive services.

- Audit Scope Selection: Targeted high-risk areas, data security, regulatory compliance (including AML/KYC), and financial reporting controls, chosen based on recent growth and partner inquiries. This risk-based focus aligns with standard internal audit practices where critical controls get priority.

Key Findings:

- Documentation gaps in user access approval logs.

- Inconsistent reconciliation evidence in financial reporting.

- Vendor controls are incomplete for third-party service providers.

Practical Remediation Outcomes:

- Standardized evidence folders with version control and templates.

- Scheduled reconciliation cycles with ownership assignments.

- Remediation plans for vendor risk oversight, including SLAs and security attestations.

While examples illustrate what good execution looks like, long-term audit readiness depends on governance and risk leadership that can scale with the organization and external expectations.

How Fraxtional Risk and Compliance Leadership Supports Audit Readiness

As your company scales, you need leadership that understands risk, controls, and regulatory expectations, but full-time executives aren’t always the right fit early on. That’s where Fraxtional’s risk and compliance leadership model changes the way teams prepare for internal audits and external scrutiny.

Recognized as a top 10 provider of fractional compliance leadership in the U.S. in 2024, Fraxtional brings experienced leaders into your organization to strengthen risk posture without the cost or commitment of a full-time hire.

Here’s how this leadership model supports audit readiness and business confidence:

- Right-Sized Leadership for Your Stage: Fraxtional leaders integrate directly with your team, adding senior compliance and risk expertise without full-time overhead, so controls and audits are prepared at the pace of your growth.

- Guided Audit Scope and Priorities: Leaders help define the right audit focus based on your specific risks, regulatory context, and stakeholder expectations, avoiding overengineering while targeting what matters most.

- Remediation-Focused Execution: Controlling risks isn’t just documenting them; Fraxtional leadership ensures gaps get ownership, timelines, and defensible evidence so auditors see progress, not just findings.

- Sponsor Bank and Investor Readiness: With experienced compliance leadership, you’re able to demonstrate controls and evidence that align with what sponsor banks and investors actually look for during reviews.

- Flexible Engagement Models: Whether you need on-demand advisory, subscription retainer support, or a named compliance executive, the model scales with your needs without the drag of permanent executive costs.

Also Read: Vendor Audit Guide: Key 5 Step Process and Controls That Drive Approval

Strong audit readiness ultimately reflects governance quality and leadership discipline.

Final Thoughts

An effective internal audit checklist does more than prepare you for reviews; it gives founders, boards, and risk leaders a clear view of how risks actually operate inside the business. When audits are scoped correctly and aligned to the company stage, they surface gaps early and protect momentum during fundraising, partnerships, and regulatory scrutiny.

This is where Fraxtional’s risk and compliance leadership model fits naturally. By integrating senior-level expertise without forcing premature full-time hires, Fraxtional helps companies define the right audit scope, strengthen controls that matter, and turn audit findings into practical remediation, across fintechs, banks, crypto firms, and PE portfolios.

If you’re evaluating how audit readiness fits into your growth plans, reach out to speak with a Fraxtional risk and compliance leader to discuss your current gaps, upcoming scrutiny, and the most practical next steps forward.

FAQs

An internal audit checklist should be updated whenever there’s a material change in business model, regulation, systems, or risk exposure. For most scaling companies, this means at least annually, with targeted updates after funding rounds, new product launches, or regulatory changes.

Internal audits are not legally mandatory for most startups. However, investors, sponsor banks, and regulators often expect internal audit discipline as companies scale. Internal audits become a commercial requirement well before they become a legal one.

Yes. Many growing companies conduct internal audits through existing leadership, supplemented by experienced external or integrated audit leadership. The key requirement is independence of review and clear accountability, not a large in-house audit department.

Auditors typically request evidence of control execution, such as approval logs, reconciliations, access reviews, policy acknowledgments, and remediation tracking. Documents that show what actually happened matter more than lengthy policy manuals or theoretical process descriptions.

The duration depends on scope and maturity. A focused, risk-based internal audit can take a few weeks, while broader reviews may take several months. Overly large scopes are a common reason audits drag on and disrupt business operations.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.

Now Accepting:

BTC

ETH

USDC

USDP