Jan 8, 2026

Everything You Need to Know About CDD Compliance in 2026

By Fraxtional LLC

Summarize the blog with AI

The Customer Due Diligence (CDD) services market reached $3.08 billion in 2024 and is expected to grow at a rate of 9.6% annually. This significant growth reflects the growing importance of compliance in sectors such as banking, FinTech, and cryptocurrency. As regulations become stricter, businesses face more pressure to meet legal requirements without compromising customer trust.

If you’re in an industry that deals with high volumes of transactions, the complexity of staying compliant can feel daunting. The risk of penalties, reputational damage, or missing vital red flags is real, and it can put your business at risk. Getting CDD wrong isn’t just a regulatory failure; it can cost you clients, investors, and your company's reputation.

In this blog, we’ll explore what CDD is, why it matters, the different types of CDD, and how businesses can implement best practices. We’ll also examine regulatory requirements, sector-specific needs, and the future direction of CDD.

Key Takeaways:

- CDD ensures businesses verify customer identity, assess financial crime risk, and comply with regulations to prevent fraud, money laundering, and terrorism financing.

- There are three types of CDD: Standard, Simplified, and Enhanced, based on the customer's risk level.

- Effective CDD helps avoid regulatory penalties, reputational damage, and financial crime involvement.

- The CDD process includes customer identification, risk assessment, ongoing monitoring, and enhanced checks for high-risk clients.

- Common challenges in CDD include weak monitoring and incomplete checks, but these can be addressed with technology, regular training, and a risk-based approach.

What is Customer Due Diligence (CDD)?

Customer Due Diligence (CDD) is the process of verifying a customer’s identity, assessing their risk, and ensuring compliance with regulatory requirements. It helps prevent financial crime and protects businesses from the risk of fraud, money laundering, and terrorism financing. CDD is a fundamental part of the broader anti-money laundering (AML) efforts across various sectors.

To clarify how CDD differs from other related processes, here’s a table that compares KYC, CDD, and EDD:

Now that you understand what CDD is, let's explore the different types of due diligence applied based on risk.

Also Read: KYC Compliance in Commercial Banking Explained

Types of Customer Due Diligence (CDD)

Customer Due Diligence is not a one-size-fits-all process. Depending on the customer's risk profile, businesses must apply different levels of scrutiny. There are three main types of CDD:

1. Standard Due Diligence

This is the most common form of CDD applied to low-risk customers. It includes basic identity verification and a risk assessment based on the customer’s profile. Standard checks typically involve reviewing official identification documents and confirming basic financial information.

2. Simplified Due Diligence

Simplified Due Diligence is used when the customer poses a low risk. This level of CDD requires fewer checks and documentation compared to standard due diligence. It is often applied to low-value transactions or customers who have established a low-risk profile over time.

3. Enhanced Due Diligence (EDD)

EDD is reserved for high-risk clients, including politically exposed persons (PEPs) and individuals from high-risk countries. This type of due diligence requires deeper investigation, including additional documentation and a thorough review of the customer’s financial history.

With the different types of CDD in mind, let’s explore why it’s so important for your business.

The Importance of CDD for Compliance and Security

Customer Due Diligence is critical for ensuring that businesses comply with legal requirements while protecting themselves from financial risks. It helps detect and prevent financial crimes such as money laundering, fraud, and terrorist financing. Without proper CDD, businesses face significant risks, including financial penalties, reputational damage, and exposure to illicit activities.

To highlight why CDD is essential, consider the following points:

- Compliance with Regulations: CDD ensures that businesses meet the requirements set by regulatory bodies, such as FinCEN, the FCA, and the FATF, thereby avoiding penalties.

- Prevention of Financial Crime: Effective CDD helps detect suspicious activities, such as money laundering, protecting businesses from becoming unwittingly involved in illegal practices.

- Mitigation of Risk: By assessing the risk profile of each customer, CDD helps businesses avoid high-risk clients and potential financial losses.

- Trust and Reputation: Proper CDD demonstrates to clients, investors, and regulators that a business takes its legal obligations seriously and is committed to maintaining a trustworthy environment.

- Operational Efficiency: A well-designed CDD process can help businesses reduce fraudulent activities, saving time and resources in the long run.

Having established the importance of CDD, let’s walk through the process to ensure you can implement it effectively.

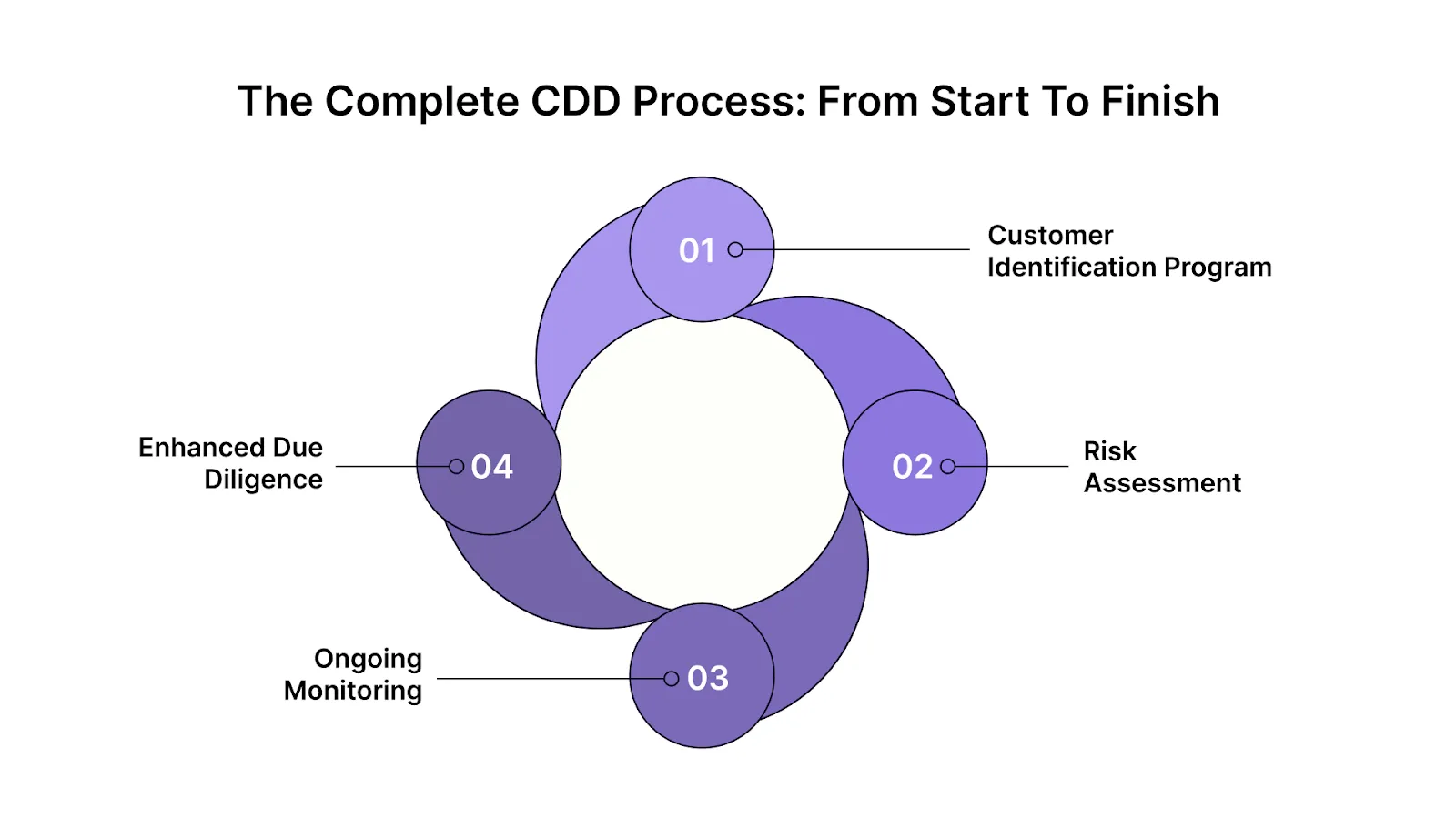

The Complete CDD Process: From Start to Finish

The CDD process involves several stages to ensure businesses comply with regulations and assess potential risks. Each step helps businesses confirm the identity of their customers and assess whether they pose any threats. Here’s a detailed breakdown of the key steps in the process:

- Step 1: Customer Identification Program (CIP)

- This first step involves gathering and verifying basic customer information, including their full name, address, and date of birth. Customers may be required to provide official documents, such as government-issued IDs, to verify their identity.

- Step 2: Risk Assessment

Once the customer’s identity is verified, businesses assess the risk they pose based on factors like geographic location, type of business, and transaction patterns. Higher-risk customers require more scrutiny.

- Step 3: Ongoing Monitoring

After onboarding, businesses must continuously monitor their customers' activities. This includes tracking transactions for suspicious behavior and ensuring customer information remains up to date.

- Step 4: Enhanced Due Diligence (EDD)

For high-risk customers, businesses conduct more detailed checks. This can include additional documentation, background checks, and investigations into sources of funds, particularly for politically exposed persons (PEPs) or complex corporate structures.

Now that you understand the process, it's essential to align it with global regulations to ensure compliance.

Also Read: Risk Management Strategies to Protect Your Business in 2025

Understanding CDD Compliance Across Different Jurisdictions

Understanding regulatory environments across major jurisdictions helps businesses align their CDD procedures with applicable requirements. Below are key regions and their enforcement frameworks.

- United States

The Financial Crimes Enforcement Network (FinCEN) enforces the CDD Final Rule, which requires financial institutions to identify beneficial owners and monitor customer relationships.

Penalty actions include civil and criminal fines for violations of the Bank Secrecy Act (BSA); fines can reach millions of dollars, and individuals may face jail time. For instance, violations of anti‑money laundering laws may result in organizational fines up to double the transaction value or millions of dollars per offence.

- United Kingdom

The Financial Conduct Authority (FCA) and other regulators enforce the Money Laundering Regulations 2017 and the Sanctions and Anti‑Money Laundering Act 2018, which govern CDD duties for firms.

Firms that fail to execute effective CDD may face significant monetary penalties or regulatory sanctions, and firms have lost business licenses for repeated non‑compliance. Under the UK framework, money laundering offenses carry criminal sentences up to 14 years’ imprisonment and substantial fines under the Proceeds of Crime Act 2002.

- Global & Emerging Markets

International standards set by the Financial Action Task Force (FATF) require CDD for high‑risk jurisdictions and virtual asset providers, pushing countries to adopt new rules. Enforcement statistics show that the U.S. imposed over $8.2 billion in financial remedies in 2024, driven by failures in CDD and transaction monitoring.

For international firms operating across borders, the implications include regulatory scrutiny, loss of correspondent banking access, and reputational damage if CDD frameworks are weak.

Fraxtional offers dedicated leadership solutions for compliance, risk management, and regulatory compliance. Explore our services today!

Top CDD Challenges and How to Solve Them

Financial institutions frequently encounter significant challenges in implementing Customer Due Diligence (CDD) effectively, which can lead to regulatory fines, reputational damage, and regulatory intervention. Each challenge requires not only recognition but actionable responses that address systemic gaps. What follows are common issues and practical strategies for overcoming them.

- Inadequate customer risk profiling and monitoring

When firms fail to assess customer risk accurately or update profiles effectively, regulators may impose fines of up to millions of dollars.

Solutions: Adopt a risk‑based approach that assigns higher scrutiny to high‑risk customers, and implement regular reviews of customer activity and risk profiles.

- Poor or incomplete beneficial ownership checks

Insufficient verification of beneficial owners and complex ownership structures can result in regulatory sanctions and substantial penalties.

Solutions: Require clear documentation of ultimate beneficial ownership, and ensure verification of identities using reliable data sources and periodic reassessments.

- Failure to report suspicious activity

Failure to monitor transactions or file Suspicious Activity Reports (SARs) can result in regulatory action, including substantial monetary fines for non-compliance.

Solutions: Deploy technology tools such as alerts and analytics to flag unusual activity, and establish formal policies for suspicious transaction reporting and escalation.

- Regulatory and jurisdictional complexity

Operating in multiple jurisdictions increases the complexity of CDD compliance, exposing firms to enforcement in different regimes with varying penalties and enforcement actions.

Solutions: Create a global compliance framework with local adaptations, maintain centralized oversight, and ensure cross‑jurisdiction training for staff on specific regional requirements.

- Resource constraints

Reliance on outdated methods, poor data integrity, and a lack of automation can lead to compliance breakdowns and regulatory scrutiny.

Solutions: Invest in compliance technologies such as automation and analytics, cleanse and standardize customer data, and integrate CDD workflows into broader governance models.

By addressing each of these challenges with targeted solutions, your firm can mitigate regulatory risk, maintain investor confidence, and safeguard its operations against compliance failures.

Conclusion

Customer Due Diligence (CDD) is crucial for businesses to avoid financial crimes, regulatory penalties, and reputational damage. Non-compliance can result in significant fines and legal consequences, as seen in both the U.S. and the U.K.

Fraxtional offers the expertise to help your business build a strong, scalable CDD program. From fraxtional compliance leadership to tailored policies, we support fintechs, banks, crypto companies, and private equity firms.

FAQs

The 4 P's of due diligence refer to People, Processes, Platform, and Performance. These factors help businesses evaluate potential clients or partners, ensuring that all necessary risks are assessed during the due diligence process.

A red flag in due diligence refers to any warning sign or inconsistency that raises concerns about a client or partner’s activities. Examples include suspicious financial transactions, unexplained ownership structures, or discrepancies in reported income.

While there is no one-size-fits-all rule, CDD should be updated regularly based on the risk profile of the client. High-risk clients may require more frequent updates, while low-risk customers can be reviewed periodically, such as every 2-3 years.

Yes, small businesses that deal with financial transactions or provide financial services must perform CDD to comply with anti-money laundering (AML) regulations. The level of due diligence may vary based on the size and nature of the transactions.

Businesses can manage the cost of CDD by adopting automated solutions, such as software tools for identity verification and transaction monitoring. Outsourcing compliance functions or using fractional compliance leadership can also help reduce internal costs.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.

Now Accepting:

BTC

ETH

USDC

USDP