Feb 18, 2026

Fintech Compliance Partnership Playbook: Build Strong Bank Relationships That Scale

By Fraxtional LLC

Summarize the blog with AI

In 2024, sponsor banks reported that more than half of their deposit growth (51.3%) was tied to fintech partnerships. This makes these relationships core to their revenue strategy, not optional innovation. At the same time, banks remain fully accountable for third-party risk throughout the relationship lifecycle.

That tension is exactly where many partnerships struggle.

A fintech compliance partnership today is not just about passing onboarding. It's about proving, month after month, that governance, monitoring, and controls are structured, documented, and scalable. When that foundation is weak, the fintech bank relationship becomes reactive, slow-moving, and subject to increased oversight.

This playbook exists for one purpose: to help U.S. fintech leaders and sponsor banks build compliance partnerships that reduce friction, satisfy regulatory expectations, and support sustainable growth.

You will understand what strong partnerships actually look like in practice and how to operationalize one in the next 30–60 days.

Key Takeaways

- Passing onboarding isn't enough. Sponsor banks evaluate ongoing oversight, not just initial approval.

- Lifecycle risk management is mandatory. Clear roles, measurable controls, and contingency planning are baseline expectations.

- Governance structure reduces friction. A defined cadence and evidence-ready documentation speed up reviews.

- Vendor oversight drives scrutiny. Weak third-party controls often trigger monitoring pressure.

- Compliance maturity enables scale. Strong partnerships accelerate growth; weak ones slow it down.

Why "Compliance Partnership" Is Now Make-or-Break for U.S. Sponsor Banking

Over the past years, U.S. regulators have sharpened their expectations around third-party risk. Banks are responsible for managing risk across the entire lifecycle of fintech partnerships, from due diligence to ongoing monitoring and termination planning.

In practical terms, that means oversight doesn't stop at contract signing.

For fintechs, this shift changes the nature of a fintech compliance partnership. It is no longer required to submit policies during onboarding. It is about maintaining structured governance, documented controls, and transparent reporting long after launch.

Regulators now expect banks to demonstrate:

- Risk assessments customized to each fintech partner

- Clear roles and accountability between the bank and fintech

- Ongoing monitoring with measurable controls

- Contingency planning if the relationship ends

When these elements are weak, sponsor banks face exam findings, enforcement actions, or growth restrictions. As a result, banks are tightening expectations across every fintech bank relationship.

The difference between partnerships that stall and those that scale is rarely innovation. It is almost always a governance discipline.

Let's define what banks actually mean when they say they want a "strong" compliance partnership and how that translates into operational reality.

What Banks Actually Mean by a "Strong" Fintech Compliance Partnership

When sponsor banks say they want a "strong" compliance partnership, they are not asking for more documents. They are asking for predictability.

Under U.S. interagency third-party risk guidance, banks must demonstrate to examiners that fintech relationships are governed by structured planning, due diligence, contracting, ongoing monitoring, and contingency readiness. That framework shapes how banks evaluate every fintech compliance partnership today.

A strong partnership, therefore, is one where governance and evidence are routine, not reactive.

The five attributes banks consistently reward are:

- Clear ownership and escalation paths

Banks expect defined roles across compliance, risk, operations, and technology. If an issue arises, there should be no confusion about who owns remediation and how it escalates. - A risk-based compliance program

Template policies are not enough. Controls must align with the fintech's actual products, transaction flows, customer base, and vendor ecosystem. - Evidence-ready controls

Monitoring, testing, and QA should produce documented outputs. Banks want to see dashboards, reports, issue logs, and closure documentation without repeated follow-ups. - Transparent reporting and data integrity

Reconciliations, transaction-monitoring metrics, complaint data, and audit findings should be accessible and consistent. Surprises create scrutiny. - Change management discipline

New products, expanded geographies, or new vendors should follow a documented review and approval process. Growth without governance is where most fintech bank relationships break down.

A mature fintech compliance partnership reduces repeated information requests and shortens review cycles. It creates a steady operating rhythm that allows both parties to focus on growth instead of remediation.

Fraxtional helps fintech teams define escalation paths, align risk frameworks with sponsor bank expectations, and build compliance programs that withstand recurring reviews. If you're preparing for enhanced monitoring or a new bank relationship, let's structure it correctly from the start. Schedule a call with us today!

Now, let's move from definition to execution, outlining the practical operating model fintechs can implement to make compliance partnerships scalable.

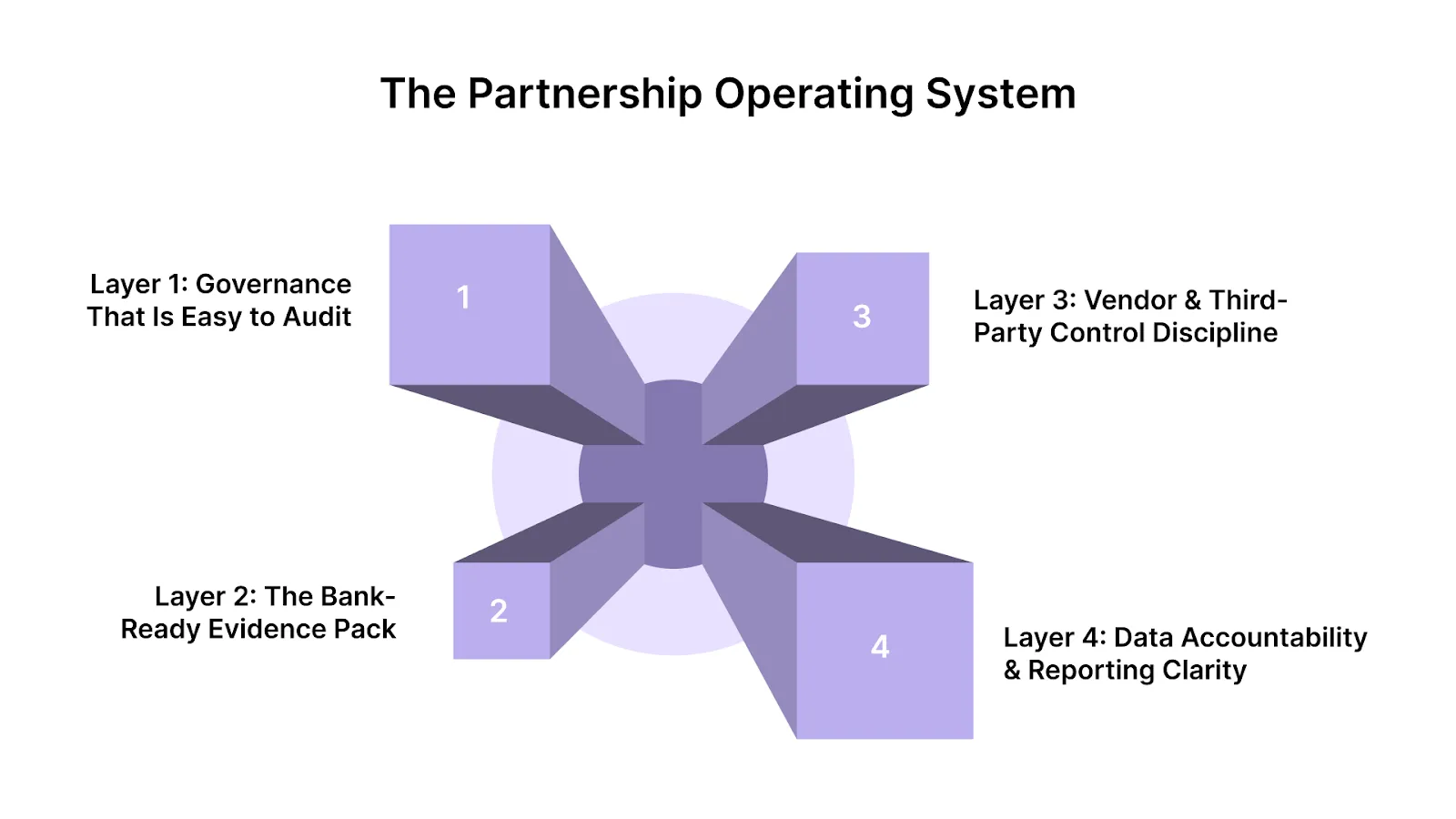

The Partnership Operating System: How to Make Compliance Scalable

A fintech compliance partnership becomes scalable when it runs on a clear operating system. No more meetings. Not more policies. A repeatable structure that produces evidence, manages risk, and keeps both sides aligned.

Below is the practical model many durable fintech bank relationships follow.

Layer 1: Governance That Is Easy to Audit

Strong partnerships begin with a defined structure.

That includes:

- A joint governance charter outlining decision rights

- A standing compliance and risk forum, typically monthly

- Quarterly executive reviews for strategic issues

- A documented issue management workflow

Every issue should move through a defined path: intake, severity rating, owner assignment, remediation plan, and documented closure.

When governance is structured this way, sponsor banks see discipline instead of disorder. Examiners see oversight instead of dependency.

Layer 2: The Bank-Ready Evidence Pack

Banks do not want explanations. They want proof.

A scalable fintech compliance partnership maintains an “evidence pack” that can be shared on demand. At minimum, this includes:

- A current enterprise risk assessment

- A mapped inventory of policies and procedures with version control

- Training records and attestations

- Monitoring metrics and QA results

- An internal audit or an independent testing plan

- A vendor inventory with due diligence status

- An incident response and communication plan

When these artifacts are organized and up to date, ongoing monitoring becomes smoother and faster.

Layer 3: Vendor and Third-Party Control Discipline

Many breakdowns in fintech bank relationships stem from vendor oversight.

Banks are expected under federal guidance to evaluate not only direct fintech risk, but also the fintech's critical third parties. That means fintechs must demonstrate:

- Risk-based vendor due diligence

- Annual refresh cycles for high-risk providers

- Contract clauses that allow oversight and audit rights

- Contingency planning if a critical vendor fails

Ignoring this layer exposes both sides to avoidable risk.

Layer 4: Data Accountability and Reporting Clarity

Operational clarity prevents regulatory escalation.

Fintechs should clearly define:

- The system of record for balances and reconciliations

- Reporting cadence and format provided to the sponsor bank

- Data access controls and retention standards

- Escalation triggers for discrepancies

When data ownership is ambiguous, oversight intensifies. When it is documented and tested, trust increases.

A fintech compliance partnership built on these four layers shifts the dynamic from reactive oversight to structured collaboration.

Next, let's examine the most common failure points in fintech bank relationships and how to prevent them before they trigger friction in monitoring.

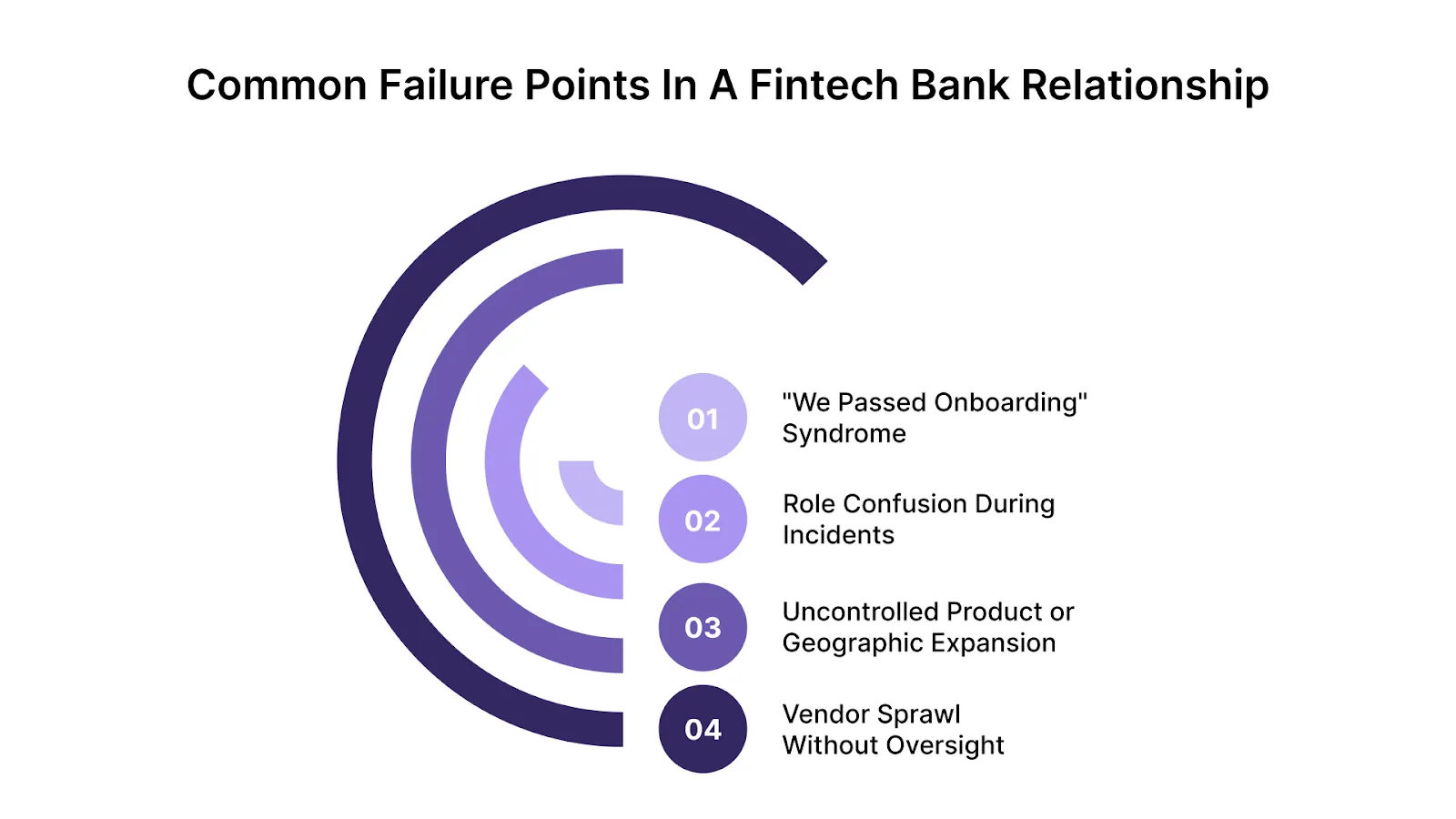

The Most Common Failure Points in a Fintech Bank Relationship

Most fintech compliance partnerships do not fail because of bad intent. They fail because structure does not keep pace with growth.

Below are the most common breakdowns sponsors see and how to prevent them.

1. "We Passed Onboarding" Syndrome

The fintech invests heavily in initial due diligence. Policies are drafted. Controls are documented. Launch happens.

Then monitoring begins.

Over time, documentation becomes outdated. Risk assessments are not refreshed. Metrics are tracked but not formally reviewed. The partnership becomes reactive.

- Prevention:

Treat ongoing monitoring as a recurring audit cycle. Refresh risk assessments at least annually. Maintain version-controlled policies. Document review meetings and issue remediation.

A fintech compliance partnership must operate continuously, not episodically.

2. Role Confusion During Incidents

When a compliance issue or operational event occurs, escalation becomes messy. Who owns regulator communication? Who documents remediation? Who informs customers?

Ambiguity erodes trust quickly.

- Prevention:

Create a documented RACI matrix covering compliance, fraud, AML alerts, disputes, and customer complaints. Test it through tabletop exercises. Shared clarity reduces friction during real events.

3. Uncontrolled Product or Geographic Expansion

Growth is positive. Uncontrolled expansion is not.

Adding a new product feature, customer segment, or state footprint without a documented compliance review introduces risk misalignment. Sponsor banks may then impose tighter controls or pause approvals.

- Prevention:

Implement a formal change management process. Any new initiative should trigger a risk review, policy updates, and notification to the sponsor bank before launch.

Strong fintech bank relationships reward disciplined scaling.

4. Vendor Sprawl Without Oversight

Fintech ecosystems rely on multiple technology providers, processors, and analytics tools. When vendor due diligence is inconsistent or undocumented, sponsor banks elevate scrutiny.

This is particularly sensitive under U.S. third-party risk guidance, which expects banks to understand the fintech's critical dependencies.

- Prevention:

Maintain a centralized vendor inventory. Classify vendors by risk tier. Track due diligence refresh dates and contractual audit rights.

Vendor oversight is often the silent pressure point in a fintech compliance partnership.

In each case, the root cause is the same: governance did not evolve with the business's scale.

Suggested Read: 10 Effective Techniques for Compliance Remediation

Let's move from risk prevention to execution, outlining a practical 30–60-day plan to operationalize a scalable compliance partnership.

30–60 Day Implementation Plan: Operationalize the Partnership

Building a scalable fintech compliance partnership does not require a year-long transformation. It requires focused structure and disciplined execution.

Below is a practical rollout plan many high-performing fintech teams follow.

Weeks 1–2: Align Scope, Ownership, and Expectations

Start with clarity.

- Define the partnership model and risk boundaries

- Confirm regulatory scope across products and geographies

- Create a RACI matrix covering compliance, AML, fraud, disputes, and reporting

- Establish a standing monthly compliance forum and quarterly executive review

At this stage, the goal is alignment. A fintech bank relationship strengthens when expectations are documented early.

Weeks 3–4: Build the Evidence Pack MVP

Next, assemble the core artifacts that sponsor banks will routinely request.

Focus on:

- Updating or completing the enterprise risk assessment

- Creating a centralized policy and procedure inventory

- Documenting monitoring metrics and reporting cadence

- Building or refining the vendor inventory with risk tiers

- Establishing a formal issue tracking log

Perfection is not required at this stage. Consistency and documentation are. A structured evidence foundation reduces the need for subsequent reviews.

Weeks 5–8: Operationalize and Stress-Test

Now shift from documentation to discipline.

- Conduct a mock monitoring review internally

- Run a tabletop incident simulation with defined escalation roles

- Review open issues and document closure evidence

- Validate vendor oversight documentation

- Confirm data reconciliation processes and reporting accuracy

This phase converts policies into an operating rhythm.

A fintech compliance partnership is durable when its governance is tested by regulators or sponsor banks before implementation.

By the end of 60 days, the partnership should have:

- Defined governance cadence

- Documented risk and policy framework

- Structured vendor oversight

- Clear reporting flows

- Active issue management

At that point, monitoring becomes predictable. Growth discussions become easier. Trust deepens.

If you're trying to operationalize compliance in the next quarter but lack senior oversight to lead it, that gap will slow execution.

Fraxtional's fractional compliance and risk leaders step in to drive the buildout, from risk assessments and vendor frameworks to sponsor bank governance alignment. If you need momentum without hiring full-time leadership yet, reach out to us today!

Now, let's address when fintechs should rely on internal teams alone and when fractional leadership strengthens the compliance partnership.

When to Strengthen the Partnership With Fractional Leadership

Not every fintech needs a full in-house compliance executive on day one. But every fintech compliance partnership requires senior-level oversight.

The question is not whether expertise is needed. It is when and how to structure it.

1) Early Stage: Structure Without Full-Time Overhead

Seed and Series A fintechs often lack the budget for a full-time Chief Compliance Officer. Yet sponsor banks still expect structured governance, documented controls, and regular reporting.

At this stage, fractional leadership can:

- Build the initial risk assessment and policy framework

- Establish governance cadence with the sponsor bank

- Design monitoring dashboards and issue tracking

- Prepare the team for due diligence and onboarding

This approach creates maturity without fixed executive overhead.

2) Growth Stage: Oversight Plus Internal Execution

As transaction volume increases and products expand, operational complexity rises.

Here, fintechs benefit from:

- An internal compliance manager handling day-to-day execution

- Fractional executive oversight guiding strategy, regulator interaction, and sponsor bank engagement

- Structured audit and independent testing coordination

This model strengthens the fintech bank relationship while keeping costs aligned with growth.

3) Scale Stage: Executive Depth & Specialized Support

Once a fintech operates across multiple states, partners, or product lines, compliance becomes enterprise-level.

At this point, companies often:

- Hire a full-time compliance or risk leader

- Supplement with fractional specialists for licensing, SOC 2 readiness, or independent audits

- Formalize governance reporting to executive and board levels

The goal is not more hierarchy. It is sharper accountability.

A fintech compliance partnership succeeds when expertise matches risk complexity. Under-resourced oversight leads to friction. Overbuilt teams waste capital.

The right balance depends on stage, scale, and regulatory exposure.

How Fraxtional Strengthens Fintech Compliance Partnerships

A scalable fintech compliance partnership requires more than documentation. It requires senior oversight that aligns fintech execution with sponsor bank expectations.

Fraxtional operates at that intersection.

Our fractional Chief Compliance and Risk Officers embed directly into the governance rhythm of a fintech bank relationship. Not as external advisors, but as accountable leaders who translate regulatory expectations into operational structure.

Every engagement begins with clarity:

- Assessing partnership risk exposure across products, states, and vendors

- Stress-testing governance frameworks against U.S. third-party risk expectations

- Aligning monitoring metrics with what sponsor banks actually review

- Establishing escalation and reporting routines that withstand ongoing oversight

Fraxtional does not replace internal teams. It strengthens them.

We help fintechs move from reactive compliance conversations to structured, evidence-based collaboration with sponsor banks. That shift reduces friction during monitoring cycles and builds credibility where it matters most.

The result is a fintech compliance partnership that scales with growth, rather than slowing it down. Try it out yourself today!

Wrapping Up

If your fintech compliance partnership feels reactive, has slow monitoring cycles, involves repeated bank requests, or has unclear ownership, you don't need more templates.

You need an operating rhythm that sponsors banks' trust.

Fraxtional helps fintechs strengthen sponsor bank relationships by embedding fractional compliance and risk leadership into the partnership itself. We build the governance cadence, evidence pack, escalation paths, and monitoring structure banks expect, so your fintech bank relationship can scale without constant friction.

Turn compliance partnership effort into bank-ready proof. Partner with Fraxtional to build a compliance operating system that supports growth and withstands ongoing oversight.

FAQs

A sponsor bank is the regulated financial institution that holds deposits and provides access to payment rails. The fintech builds the customer-facing product and experience. In a fintech compliance partnership, both share operational responsibilities, but the bank retains regulatory accountability.

Examiners review third-party risk management across the full lifecycle due diligence, contracting, ongoing monitoring, and contingency planning. They assess whether the bank has documented oversight and whether the fintech can produce reliable compliance evidence on demand.

Banks commonly request updated risk assessments, transaction-monitoring metrics, audit findings, complaint logs, vendor due diligence records, and policy-refresh confirmations. The depth increases if the product scope or transaction volume changes.

Fintechs reduce delays by implementing structured change management before launching new features or entering new states. Providing advanced risk assessments and documented controls shortens review cycles and builds credibility in the fintech bank relationship.

Diversification becomes relevant when transaction volumes grow, geographic expansion increases risk exposure, or operational dependency creates concentration risk. However, governance maturity must come first, as weak compliance structures multiply risk across multiple partnerships.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.

Now Accepting:

BTC

ETH

USDC

USDP