Dec 8, 2025

Why Banks Are Replacing Full-Time Executives With Fractional Leaders in 2026

By Fraxtional LLC

Summarize the blog with AI

What do banks do when they need senior leadership that can take charge of risk, compliance, or transformation without waiting months for a full-time hire?

The answer many institutions now rely on is fractional leadership.

Banks, credit unions, and investment firms are dealing with sharper regulatory oversight, tighter audit cycles, and the added complexity of fintech partnerships. Senior talent in risk, AML, cybersecurity, governance, and operational strategy is scarce, and hiring takes far longer than most institutions can wait.

Fractional leaders fill that timing gap.

These are former CROs, CAMLOs, CCOs, CFOs, and transformation heads who join part-time but take full responsibility for their function: board reporting, audit preparation, control redesign, partner-bank oversight, and everything else that can’t stall.

The model is gaining traction because banks get something they rarely get quickly — leadership with regulatory credibility, without waiting through lengthy searches or adding permanent headcount.

This article breaks down how fractional leadership works in banks, which roles are most commonly fractionalized, and why institutions are using this model to maintain governance without slowing operations.

Key Takeaways

- Banks are using fractional leaders (CROs, CAMLOs, CCOs, CFOs, CISOs) to fill senior positions faster than full-time hiring allows.

- The model gives immediate regulatory credibility, especially during audits, supervisory exams, or fintech-partner oversight.

- Fractional executives take full ownership, not advisory roles, board reporting, risk decisions, remediation plans, and governance design.

- It’s more cost-efficient than full-time leadership, while still giving institutions access to enterprise-level expertise.

- Fraxtional provides embedded risk and compliance leaders, designed specifically for banks, investment firms, and BaaS ecosystems.

The Rise of Fractional Leadership in Banking

Banks are navigating tighter supervision cycles, rising technology risks, and stronger scrutiny of fintech and BaaS partnerships. Regulators have made that clear in recent guidance: for example, the Financial Stability Board notes that banks’ reliance on third-party and fintech providers now “introduces different types of risks, which need specialist competencies to address.”

In this environment, traditional executive recruitment is too slow: full-time CROs, CAMLOs, or CCOs can take six to nine months to source and onboard. By then, the bank may already be on its third remediation plan. Fractional leadership moves into that gap.

Banks are increasingly engaging fractional senior executives, CROs, CAMLOs, CCOs, CFOs, and CISOs as embedded operators who join the business immediately, take charge of the risk and compliance agenda, and drive stability during critical windows of exposure.

Fractional leadership is rising because it supports critical functions without the friction of permanent hiring. It lets banks deploy experienced leadership when the risk model demands it, not when the hiring cycle is complete.

Why Banks Are Turning to the Fractional Leadership Model

The leadership challenges banks face today are sharper and more time-sensitive. Regulatory expectations shift quickly, and exam cycles can intensify with little notice.

Internal teams already stretched by ongoing audits, fintech-partner oversight, or remediation work often don’t have the bandwidth for new demands.

This is where fractional leadership becomes practical, not as a trend, but as a structural solution.

Banks use fractional leaders when:

- Oversight demands spike during exam cycles

- Controls need to be redesigned before an upcoming review

- Hard-to-hire roles (CRO, CAMLO, CISO) sit vacant

- New lines of business require stronger governance

- Audit findings or enforcement actions increase workloads

- Partnership models (BaaS, payments, lending) expand risk exposure

Fractional executives give banking teams something they rarely have during high-pressure periods: immediate senior leadership that can absorb work, guide remediation, and keep decisions aligned with supervisory expectations.

The model works because it lets banks scale leadership according to the intensity of regulatory pressure, bringing depth into a function quickly and tapering it once stability returns.

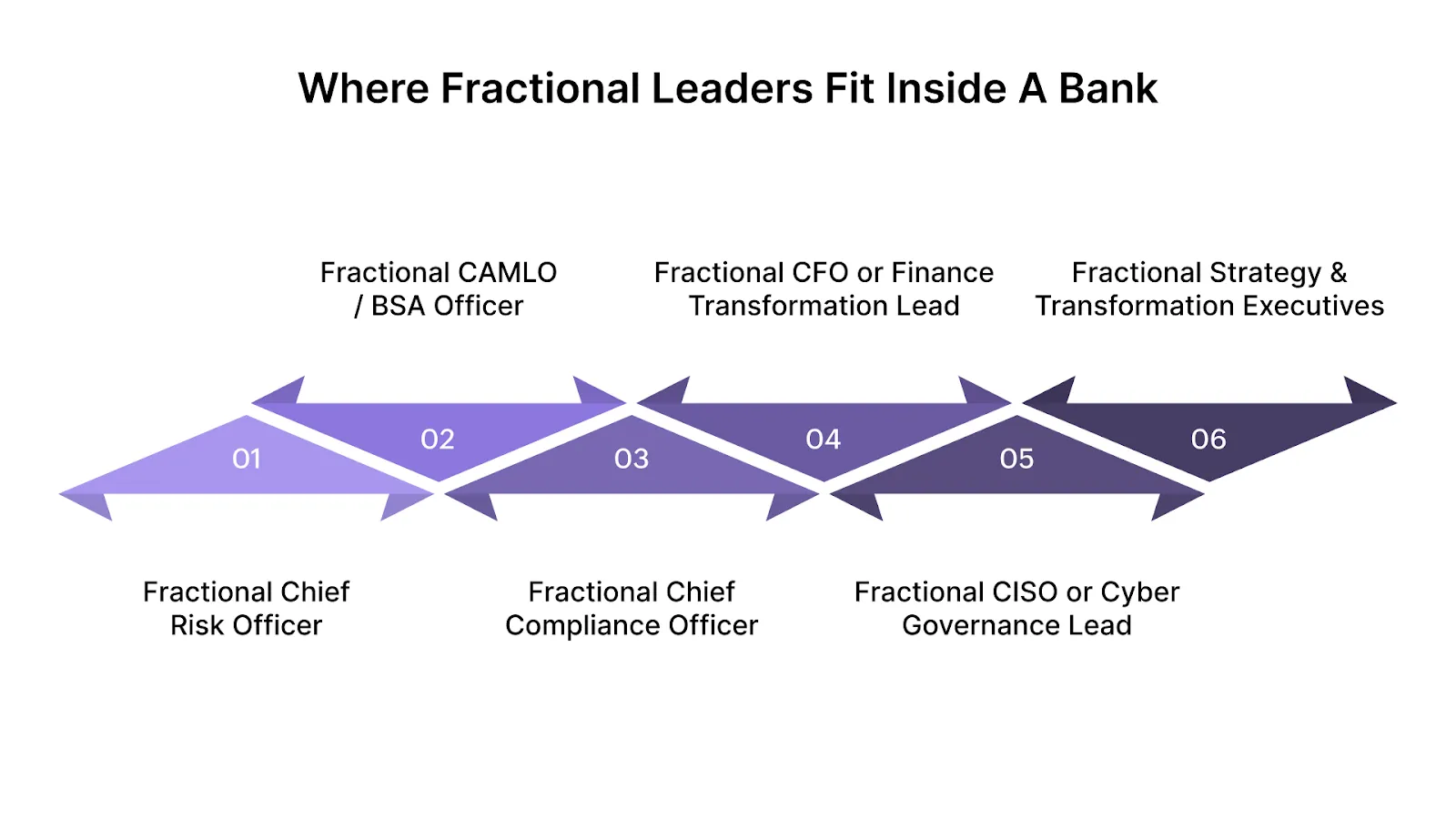

Where Fractional Leaders Fit Inside a Bank

In banking, leadership gaps create operational risk. Fractional executives are brought in to stabilize functions that cannot afford delays, taking charge of governance-heavy work and clearing backlogs before they become regulatory issues.

1. Fractional CRO (Chief Risk Officer)

Banks turn to fractional CROs when new exposures emerge faster than internal teams can rework controls.

They step in to:

- Rebuild credit, operational, or enterprise risk frameworks

- Oversee stress-testing cycles and scenario planning

- Tighten risk appetite statements before regulatory review

- Support new lines of business (cards, lending, BaaS partnerships)

A fractional CRO helps the bank keep its risk posture steady during transitions by aligning frameworks, limits, and governance with current supervisory expectations.

2. Fractional CAMLO / BSA Officer

Banks bring in fractional AML leaders when monitoring volumes spike, rules need recalibration, or examiners flag inconsistencies.

Their responsibilities include:

- Overseeing transaction-monitoring programs

- Tuning rules to reduce alert fatigue without missing suspicious activity

- Preparing and filing SARs during periods of heightened scrutiny

- Managing audits, independent reviews, and enforcement-driven remediation

Fractional CAMLOs ensure AML operations stay consistent and defensible, something internal teams often struggle to maintain during turnover or heavy alert periods.

3. Fractional CCO (Chief Compliance Officer)

Fractional CCOs stabilize compliance operations during restructuring, product expansion, or supervisory exams.

They typically handle:

- Compliance risk assessments and annual planning

- Policy harmonization across lines of business

- Compliance training, testing, and monitoring

- Strengthening issue-tracking and escalation routines

A fractional CCO keeps the compliance program synchronized with regulatory updates, ensuring controls evolve as quickly as business lines and new guidance require.

4. Fractional CFO or Finance Transformation Lead

Banks tap fractional finance leaders when capital strategy shifts or when product expansion creates new reporting demands.

They take ownership of:

- Financial controls and reporting cleanup

- ALM reviews and liquidity planning

- M&A financial integration

- Cost-rationalization and profitability modelling

Fractional finance leaders give banks clearer oversight of liquidity, capital, and reporting integrity essential during stress tests, restructuring, or rapid portfolio growth.

5. Fractional CISO or Cyber Governance Lead

Cyber governance gaps can escalate quickly. Fractional CISOs anchor the security function while the bank searches for long-term leadership.

They focus on:

- Incident-response maturity

- Vendor-risk assessments

- Identity and access governance

- Security controls needed for SOC, ISO, or FFIEC alignment

Banks rely on fractional CISOs to tighten controls during moments when cyber exposure increases from vendor escalations to audit findings.

6. Fractional Strategy & Transformation Executives

Banks bring in fractional transformation leaders to accelerate programs that typically stall due to internal bottlenecks.

They drive:

- Process redesign and operational efficiency

- Modernization of legacy systems

- Change-management leadership

- New-product governance and approval frameworks

Fractional transformation leaders help banks move high-impact projects forward by coordinating teams, clearing decision bottlenecks, and maintaining momentum across functions.

Each of these roles plugs into a different pressure point inside a bank. Not every institution needs all of them, but every institution eventually needs one of them, especially during audits, supervisory exams, or leadership turnover.

Fractional vs. Consulting vs. Full-Time Leadership: What Banks Actually Need

Banks tend to compare models when a deadline, audit, or leadership gap forces a choice.

A compliance review may need hands-on ownership.

A licensing push may need documentation.

A cyber incident may need a decision-maker, not a report.

That’s why banking teams evaluate three models side by side: consulting firms, fractional executives, and full-time leadership.

Each solves a different operational problem. Each fits a different stage of pressure.

This table breaks down how they differ where it matters most.

Leadership Models in Banking: A Practical Comparison

Why This Comparison Matters for Banks

Banks don’t pick one leadership model and stick with it. They shift between options depending on urgency, complexity, and compliance pressure.

- Fractional leadership helps rebuild controls fast, ideal for early-stage remediation or urgent risk gaps.

- Consulting firms excel during licensing and audits, where documentation accuracy and process assessments are critical.

- Full-time hires make sense once systems are stable and long-term accountability becomes necessary.

This comparison isn’t about ranking the models. It’s about helping banks decide which one to deploy, and when.

Choosing the wrong model, like hiring full-time before the problem is understood, can waste both time and credibility.

This side-by-side view helps risk leaders and founders make faster, more aligned decisions under pressure.

The challenge for most banks is finding a partner who can step in at the exact moment operational pressure peaks. That’s where the gap usually appears: exam cycles tighten, a key leader leaves, or a fintech partner expands faster than expected, and suddenly the bank needs experience it can’t hire quickly enough.

This is the point where Fraxtional fits in.

How Fraxtional Supports Banks When Leadership Capacity Falls Short

Banks call Fraxtional when a function needs someone who can take ownership immediately, someone who can walk into examiner meetings, handle governance tasks that are behind schedule, and steady a department that can’t afford drift.

Here’s how Fraxtional directly solves the issues covered in this article:

1. Filling Leadership Roles That Can’t Sit Empty

Banks struggle the most when critical roles sit vacant: CRO, CAMLO, CCO, CISO.

Fraxtional steps in with leaders who have already run these functions inside regulated institutions.

They pick up the workload on day one, risk limits, SAR decisions, control reviews, and exam prep, so nothing slows down while the bank searches for a permanent hire.

2. Bringing Order During Exam Pressure

Supervisory exams can overwhelm even well-staffed teams. Findings pile up, documentation falls behind, and routine testing pauses because every resource gets diverted toward cleanup.

Fraxtional’s leaders step in to stabilise that pressure. They help banks:

- Clear overdue issues with examiner-ready documentation, not rushed summaries

- Rebuild the risk, AML, or compliance processes flagged during the last review, so the same weaknesses don’t resurface

- Prepare teams for the next round of interviews, walkthroughs, and evidence requests with tighter narratives and cleaner audit trails

They work the way supervisors expect: organised, detail-driven, and able to defend decisions without hesitation, the level of discipline internal teams often struggle to maintain when exam cycles compress.

3. Strengthening Governance Around Fintech Partnerships

Fintech partnerships broaden a bank’s reach, but they also widen its exposure surface. Every program adds new monitoring rules, new data flows, and new operational blind spots.

Fraxtional brings in leaders who understand how to control that expansion. They focus on the areas examiners scrutinise most in BaaS and partner-bank models:

- Aligning transaction-monitoring rules with each partner’s risk profile

- Building risk-scoring methods that surface outliers early

- Standardising issue logs, reporting routines, and escalation workflows across programs

The result is a partnership framework that doesn’t crack under exam pressure — consistent, well-documented, and easy for supervisors to trace end-to-end.

4. Fixing Control Environments That Fall Behind

Fraxtional’s leaders focus on the operational routines examiners look at first when they want to understand whether a control environment is actually working:

- How testing cycles are documented

- How escalations are handled and closed

- Whether quality checks catch issues early

- How exceptions are tracked, justified, and trended

Instead of rewriting policy manuals, they strengthen the operational behaviours that determine whether a control passes or breaks under scrutiny. This is where most regulatory findings originate, and this is where Fraxtional brings stability the fastest.

5. Providing Leadership Without the Weight of Permanent Headcount

Banks don’t always need a full-time executive; they need experience at the right time.

Fraxtional gives them that flexibility:

- More support during exam seasons to handle remediation, evidence prep, and examiner queries.

- Reduced involvement during steady periods so the bank isn’t paying for idle senior time.

- Continuity during transitions so risk decisions, SAR approvals, and governance routines don’t stall.

It’s C-suite-level oversight only when it’s needed, without adding permanent overhead to the organisation.

6. Built Specifically for Regulated Institutions

Fraxtional is not a general fractional platform. The entire model is designed for banks, credit unions, investment firms, and BaaS ecosystems, places where the work is tied to supervision, exam cycles, and accountability.

If your bank needs experienced risk or compliance leadership without waiting months for a full-time hire, Fraxtional can step in immediately.

Connect with Fraxtional to bring in leaders who know how regulated environments work and can take ownership from day one.

Conclusion

Banks can’t afford leadership gaps in functions that carry regulatory exposure. Audit cycles tighten, examiner expectations shift, and fintech-partner oversight adds pressure that internal teams can’t always absorb on their own.

Fractional leadership has become a practical way for institutions to bring in experienced executives exactly when workloads peak, without waiting for long hiring cycles or expanding headcount.

Whether the need is risk, AML, compliance, cybersecurity, or transformation, fractional leaders give banks a way to keep governance stable while the organization moves through audits, remediation, or new-product growth.

Fraxtional fits directly into that reality. Their model is built for regulated environments and provides the senior oversight banks rely on during high-stakes moments, steady, accountable, and ready to take ownership from day one.

If you’re ready to reinforce a critical function without slowing down operations, Fraxtional can help.

FAQs

Fractional leadership allows banks to bring in senior executives, such as CROs, CAMLOs, CCOs, CFOs, or CISOs, on a part-time or contract basis. They take ownership of risk, compliance, or governance functions without being hired full-time.

Consultants advise and deliver documentation. Fractional leaders operate inside the bank, run the function day-to-day, and handle examiner-facing work. They’re responsible for decisions, not just recommendations.

Banks commonly bring in fractional CROs, CAMLOs, CCOs, CISOs, CFOs, and transformation leads. These roles carry high accountability and often can’t sit vacant during audits or regulatory reviews.

Yes. Large banks use fractional leaders during exam cycles, leadership transitions, remediation projects, and major transformations where they need temporary senior capacity without adding permanent headcount.

They join as part of the management rhythm, attending risk committees, meeting with regulators, reviewing controls, guiding remediation, and coordinating with internal teams until the function stabilizes.

Most banks do this when a role is vacant, when examiners issue findings, when alert volumes spike, during partner-bank oversight, or when governance needs to mature before a supervisory review.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.