Jan 30, 2026

Vendor Audit Guide: Key 5 Step Process and Controls That Drive Approval

By Fraxtional LLC

Summarize the blog with AI

Vendor relationships are rarely stress-tested during routine operations. Pressure shows up during audits, sponsor bank diligence, and regulatory exams, when reviewers start asking for evidence behind your vendor audit program, not slide decks. In regulated fintech and banking environments, a vendor audit becomes the proof point that third-party risk is identified, measured, and actively controlled.

Reviewers dig into how your vendor audit process operates across data security, AML dependencies, infrastructure providers, and critical service partners, looking for documented scope, control validation, and tracked remediation. When vendor oversight exists in theory but not in evidence, diligence slows, bank approvals stall, and regulatory questions expand quickly.

This guide breaks down what a vendor audit means in regulated financial services, how banks and examiners evaluate vendor audits, and what your vendor audit process must include to hold up under real scrutiny.

Key Takeaways

- A vendor audit must demonstrate real control testing, evidence validation, and remediation tracking, not just policies or vendor questionnaires.

- Payment processors, cloud hosts, AML providers, and API partners need annual audits plus continuous monitoring due to their direct regulatory and operational impact.

- Sponsor banks examine access controls, encryption practices, API security, subcontractor oversight, and unresolved audit findings before approving partnerships.

- Outdated SOC reports, missing right-to-audit clauses, open CAPAs, and poor fourth-party visibility are common reasons fintech-bank deals stall.

- Management tracks the relationship; vendor audits independently verify controls actually operate as intended under regulatory expectations.

What Is a Vendor Audit in Regulated Financial Services?

A vendor audit in financial services is a formal, evidence-driven control assessment of third parties that handle regulated data, funds flow, or critical infrastructure. It verifies that vendor operations align with financial regulations, security obligations, and enforceable contractual standards.

- Risk Transfer Validation: Quantifies operational and compliance risk shifted to vendors handling KYC, payments processing, cloud hosting, or transaction monitoring.

- Sensitive Data Safeguards: Tests controls protecting PII, cardholder data, SAR information, and encryption key management environments.

- Regulatory Control Mapping: Confirms vendor processes map to PCI-DSS, SOC 2 Trust Services Criteria, FFIEC guidance, or equivalent supervisory expectations.

- Operational Resilience Testing: Reviews disaster recovery RTO/RPO metrics, failover architecture, and incident response integration with your escalation procedures.

- Contractual Control Enforcement: Verifies right-to-audit clauses, data use restrictions, subcontractor oversight, and breach notification timelines are operationalized.

A vendor audit proves your third-party controls work in practice, not just on paper. Regulators and sponsor banks expect documented evidence of that oversight.

Why Vendor Audits Matter for Fintech, Crypto, and BaaS

Fintechs, crypto firms, and BaaS platforms run on outsourced infrastructure, embedded partners, and API-driven ecosystems. That model scales fast, but it multiplies third-party regulatory, data, and operational exposure overnight.

- Outsourced Core Infrastructure: Card processors, cloud hosts, node providers, and KYC vendors run critical paths. Failures there become your regulatory and customer incident.

- Cross-Border Data Exposure: Vendors often process EU, UK, and US data simultaneously, triggering overlapping GDPR, UK GDPR, GLBA, and state privacy enforcement risk.

- Embedded Finance Dependencies: BaaS programs rely on sponsor bank processors and middleware. Weak vendor controls can break settlement, ledger integrity, or transaction monitoring flows.

- Fourth-Party Risk Expansion: Your vendor’s subcontractor may store backups, run analytics, or handle support. That creates unseen exposure regulators still hold you accountable for.

- Real-Time Attack Surface: API-connected vendors expand your live production perimeter, increasing credential abuse, token compromise, and integration-layer breach risk.

Vendor audits give you documented control over an ecosystem you do not fully own. That control is what banks, regulators, and investors look for before they trust your model.

For a deeper look at audit readiness in card data environments, see How to Prepare for a PCI Audit: Expert Tips for 2026.

Types of Vendor Audits You Should Be Running

A mature third-party oversight program uses multiple audit types depending on vendor risk, service model, and regulatory exposure. One audit style does not cover fintech, crypto, and BaaS risk profiles.

- Pre-Contract Control Audit: Validates security architecture, compliance posture, and operational maturity before production access, API integration, or customer data exchange begins.

- Periodic Surveillance Audit: Recurring reviews of control effectiveness, incident history, SLA adherence, and regulatory change impact during the active vendor relationship.

- Incident-Triggered Audit: Deep-dive assessment launched after breaches, AML control failures, downtime events, or regulator inquiries tied to the vendor’s environment.

- Service Provider Control Audit: Focuses on SaaS, cloud, and API partners, testing logical access, encryption practices, uptime resilience, and secure development lifecycle controls.

- Independent Assurance Audit: Takes advantage of SOC reports, ISO certifications, or AUP testing by external firms to validate internal audit conclusions with third-party evidence.

Running the right mix of vendor audits guarantees oversight matches real operational and regulatory exposure. Regulators expect audit types to scale with vendor criticality, not convenience.

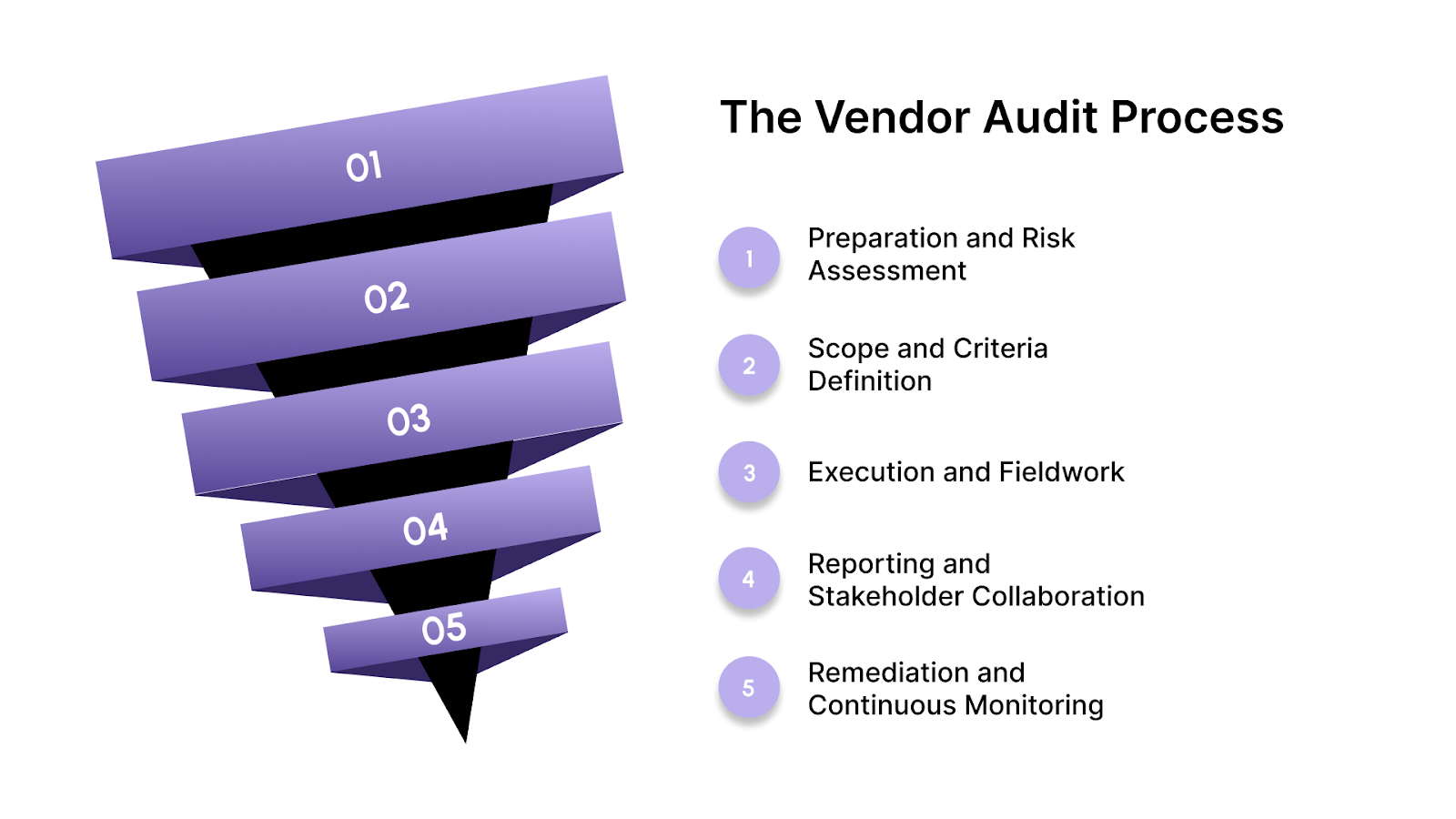

The Vendor Audit Process (Step-by-Step Framework)

A defensible vendor audit process follows structured phases, moving from risk scoping to continuous oversight, guaranteeing third-party controls align with regulatory, security, and contractual obligations.

Step 1: Preparation and Risk Assessment

This stage establishes vendor criticality, regulatory exposure, and system dependency to determine audit intensity, timing, and control depth before any detailed testing begins.

- Risk Tiering Alignment: Classify vendors by data sensitivity, funds flow involvement, customer impact, and regulatory scope across AML, privacy, and operational resilience domains.

- Integration Footprint Review: Map APIs, data exchanges, authentication flows, and infrastructure dependencies to understand how deeply the vendor connects into production systems.

- Control Maturity Baseline: Issue structured security and compliance questionnaires to benchmark governance, incident response, access control, and regulatory readiness before fieldwork.

Step 2: Scope and Criteria Definition

Here, you translate risk into audit focus, defining which controls, systems, and compliance domains will be tested and which evidence sources are acceptable.

- Regulatory Mapping Exercise: Align audit criteria to applicable frameworks such as SOC 2, PCI-DSS, ISO 27001, or sector-specific supervisory expectations impacting the vendor’s service.

- KPI and Control Selection: Define measurable indicators covering uptime performance, access provisioning timelines, encryption coverage, and recovery objectives for critical systems.

- Evidence Requirement Matrix: Predefine required artifacts, including policies, logs, architecture diagrams, penetration test summaries, and independent assurance reports.

Step 3: Execution and Fieldwork

This is the evidence-gathering phase where stated controls are validated against real operational practices through technical review, interviews, and record testing.

- Environment Validation Testing: Inspect system configurations, access control lists, encryption settings, and monitoring tools to confirm controls operate as documented.

- Personnel Control Interviews: Interview security, compliance, and engineering leads to validate role responsibilities, escalation paths, and incident handling workflows.

- Transactional Data Sampling: Analyze selected production records, access logs, or exception reports to confirm system accuracy and control enforcement in live operations.

Step 4: Reporting and Stakeholder Collaboration

Findings are formalized, prioritized, and shared with governance stakeholders to drive accountability, regulatory defensibility, and operational clarity.

- Severity-Based Findings Classification: Rate issues by regulatory impact, data exposure potential, and operational disruption risk to guide remediation urgency and executive attention.

- Cross-Functional Review Sessions: Discuss results with compliance, security, legal, and vendor owners to validate context, dependencies, and remediation feasibility.

- Action Plan Formalization: Document required corrective steps, responsible parties, and target dates within a tracked remediation framework.

Step 5: Remediation and Continuous Monitoring

This phase guarantees issues are resolved, risks are reduced, and vendor performance is monitored long after the audit report is closed.

- CAPA Tracking Governance: Monitor corrective and preventive actions through formal plans, requiring documented evidence before closure of high and medium-risk findings.

- Timeline Enforcement Controls: Escalate overdue remediation items tied to security or regulatory risk through governance committees or contract enforcement mechanisms.

- Ongoing Performance Surveillance: Feed audit outcomes into continuous monitoring dashboards tracking incidents, SLA breaches, control changes, and emerging risk indicators.

A structured vendor audit process proves oversight is systematic, evidence-based, and enforceable. That consistency is what regulators, sponsor banks, and auditors expect to see.

Fraxtional provides director-led fractional compliance support that helps fintechs and sponsor-bank programs strengthen vendor oversight, close control gaps, and stay prepared for regulatory review. Request a focused review of your current vendor audit structure and evidence model to see where scrutiny could surface issues.

What Sponsor Banks and Regulators Look for in Vendor Audits

Sponsor banks and examiners review vendor audits to confirm you control outsourced risk with the same rigor as internal operations. They look for proof, not promises.

- Independent Control Validation: Current SOC reports, ISO certificates, and industry attestations reviewed, not just collected, with documented gap analysis and management response.

- Technical Access Governance: Evidence vendors follow least-privilege access, MFA enforcement, privileged user monitoring, and controlled network segmentation between your environment and theirs.

- Data Handling Discipline: Documented encryption standards, data retention schedules, secure transfer methods, and restrictions on secondary data use or unauthorized data replication.

- Subcontractor Oversight Structure: Clear visibility into fourth parties, flow-down security obligations, and monitoring mechanisms guaranteeing subcontractors meet the same control expectations.

- Contractual Enforcement Mechanisms: Right-to-audit clauses, breach notification timelines, remediation obligations, and termination rights tied to unresolved security or compliance failures.

Regulators expect your vendor oversight to be structured, evidence-backed, and enforceable. If a vendor fails, they assume your controls should have caught it.

To understand how governance frameworks translate into practical oversight, review Internal Control and Audit Procedures for Effective Management.

Common Vendor Audit Gaps That Delay Bank Partnerships

Bank due diligence teams move fast until vendor risk files fall apart. The issues below routinely push fintech and BaaS partnerships into “pause until fixed” territory.

Banks expect vendor oversight to be current, enforceable, and technically sound. Gaps in evidence or control maturity translate directly into partnership delays.

For a deeper look at identifying control weaknesses before reviews begin, see How to Conduct a Compliance Risk Assessment.

How Often Should Vendor Audits Be Performed?

Vendor audit frequency should match real exposure, not calendar habits. Banks and regulators expect cadence tied to risk tier, system impact, and live control performance.

- Annual Enterprise Risk Review: Reassess vendor risk tiering every year, factoring in new products, integrations, data types, and regulatory changes affecting existing third-party relationships.

- Critical Vendor Annual Audits: Vendors supporting payments, AML monitoring, core processing, or cloud infrastructure should undergo full control reviews at least once every twelve months.

- Quarterly Control Check-Ins: High-impact vendors should provide quarterly updates on incidents, SLA performance, control changes, and penetration testing results between formal audit cycles.

- Trigger-Based Immediate Audits: Launch out-of-cycle audits after breaches, enforcement actions, material outages, ownership changes, or negative security intelligence tied to the vendor.

- Continuous Monitoring Signals: Use automated tools to track uptime, vulnerability disclosures, certificate expirations, and compliance attestations, triggering reviews when risk thresholds are breached.

Audit timing should flex with vendor risk, not internal convenience. If exposure changes, your audit schedule should change with it.

Vendor Audits vs. Vendor Management: What Is the Difference?

These two terms get mixed up constantly. Vendor management runs the relationship. Vendor audits test whether that relationship is actually controlled, compliant, and defensible under regulatory scrutiny.

Vendor management keeps the engine running. Vendor audits pop the hood to make sure the engine is actually built the way you think it is.

Fraxtional Leadership That Strengthens Your Vendor Audit Process

Building a vendor audit program that satisfies sponsor banks and regulators takes senior compliance judgment. Fraxtional embeds experienced Directors who turn vendor oversight into a defensible, bank-ready control function.

- Embedded Compliance Leadership: A dedicated Fraxtional Director acts as your fractional CCO or BSA lead, owning third-party risk oversight end to end.

- Bank-Ready Audit Frameworks: We design vendor audit structures aligned to what sponsor banks, auditors, and regulators expect to see during diligence.

- Hands-On Control Validation: Our team reviews real vendor evidence, not summaries, and flags control gaps before they surface in bank reviews.

- Actionable Remediation Roadmaps: You receive prioritized fix plans tied directly to licensing, SOC 2, and sponsor bank approval dependencies.

- Ongoing Oversight, Not One-Off Reviews: We stay embedded to track remediation, monitor vendor risk changes, and keep your program regulator-ready as you scale.

This is not generic consulting. It is director-level compliance leadership that helps you clear bank diligence, satisfy regulators, and grow without hiring a full-time team. Make your vendor audit process review-ready. Connect with Fraxtional.

Conclusion

Vendor oversight rarely breaks because teams ignore risk. It breaks when control testing, documentation depth, and remediation tracking cannot withstand scrutiny during a vendor audit. In regulated fintech and banking models, a defensible vendor audit connects third-party risk to real operational controls, system evidence, and accountable oversight. Banks and regulators evaluate how your vendor audit process functions in practice, not how it is described in policy. When vendor audits lack traceability, independence, or follow-through, partnerships slow, and regulatory exposure increases.

Fraxtional embeds senior compliance leaders who design and run vendor audits that stand up to sponsor bank and regulatory review. We turn your vendor audit process into a structured, evidence-backed program aligned to growth, licensing, and bank expectations.

If your team is preparing for diligence or regulatory review, connect with Fraxtional to strengthen your vendor audit program.

FAQs

Yes. A mature vendor audit should evaluate how your vendor oversees its own subcontractors. Banks increasingly expect visibility into fourth-party controls within the broader vendor audit process.

Yes. Sponsor banks often require at least a basic vendor audit framework before onboarding, especially for KYC, payments, and cloud providers tied to regulated functions.

Very. Effective vendor audits include configuration proof, access control samples, encryption standards, and incident logs, not just policy documents or management attestations.

Not fully, but a structured vendor audit process can validate vendor controls between SOC reporting cycles and address scope gaps that SOC 2 reports do not cover.

Ownership should sit with compliance or risk leadership, not procurement. Regulators expect the vendor audit process to align with AML, security, and regulatory oversight functions.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.