Jan 30, 2026

Client Onboarding Financial Services: Risk and Control Guide

By Fraxtional LLC

Summarize the blog with AI

Client onboarding in financial services is rarely questioned when volumes are low and risk events stay quiet. Scrutiny begins during sponsor bank due diligence, regulatory exams, and AML reviews, when investigators pull onboarding files to test whether identity, sanctions, and risk decisions are consistently executed and defensible under review. At the same time, banks lose an estimated 60% of potential customers due to complex and frustrating onboarding processes, putting pressure on institutions to balance compliance rigor with a seamless customer experience.

In regulated financial environments, digital client onboarding becomes more than a customer experience workflow. It is the control point where institutions must prove that identity verification, beneficial ownership analysis, sanctions screening, and risk classification are operating as designed. Reviewers do not rely on policy statements. They trace timestamps, decision logic, escalation records, and system outputs to confirm that onboarding controls function in practice. When execution drifts from documented procedures, approvals are questioned, monitoring is second-guessed, and remediation expands quickly.

This guide explains how client onboarding financial services programs are evaluated by regulators and sponsor banks, where operational weaknesses typically surface, and what structures must be in place for onboarding controls to withstand real-world compliance scrutiny.

Key Takeaways

- Client onboarding for financial services sets the legal identity, sanctions status, and initial risk rating that all future monitoring and compliance controls depend on.

- Regulators and sponsor banks evaluate onboarding through file testing, decision consistency, and documented escalation evidence rather than relying on written policies.

- A risk-based onboarding model allows low-risk customers to move quickly while automatically escalating higher-risk profiles for deeper investigation and review.

- Digital client onboarding systems must generate clear, retrievable evidence, including verification results, screening logs, rule logic, and reviewer actions.

- Strong compliance ownership and governance turn onboarding from a workflow into a defensible control framework trusted by regulators and banking partners.

Why Client Onboarding Is the Most Important Compliance Moment

Client onboarding is where regulatory liability, fraud exposure, and customer conversion risk all collide in real time. This is the only stage where institutions can legally establish identity, risk profile, and monitoring baselines before funds, payments, or trading activity begins.

- Identity Verification Lock-In: CIP data captured here becomes the legal identity baseline; errors later can trigger account freezes, SAR reviews, and regulator scrutiny.

- Beneficial Ownership Exposure: UBO discovery during onboarding determines whether you trigger FinCEN CDD Rule thresholds or miss hidden control risks tied to shell entities.

- Sanctions Liability Starts Here: OFAC screening at onboarding prevents strict liability violations; onboarding failures cannot be retroactively “fixed” without regulatory consequences.

- Fraud Pattern Intercept Point: Synthetic ID, deepfake liveness failures, and device spoofing are most detectable at first interaction before behavioral patterns normalize.

- Audit Trail Foundation: Every onboarding action must produce timestamped, exportable logs to satisfy examiners reviewing CIP, CDD, and EDD decision consistency.

If onboarding controls break, downstream monitoring becomes damage control instead of prevention. Get this stage right, and everything else in your compliance program stands on solid ground.

For a deeper breakdown of evolving due diligence expectations, see Everything You Need to Know About CDD Compliance in 2026.

Regulatory Requirements That Shape Financial Services Onboarding

Financial onboarding is tightly dictated by prescriptive AML, sanctions, and identity rules. These requirements define exactly what must be collected, verified, screened, risk-rated, and retained before an account goes live.

- CIP Data Element Rules: U.S. CIP mandates name, DOB, address, and TIN collection, plus documentary or non-documentary verification before account activation.

- UBO Ownership Thresholds: FinCEN CDD Rule requires identifying 25%+ equity owners and one control person; complex trusts and layered entities demand documentary traceability.

- Sanctions Screening Obligations: OFAC 50% Rule extends blocking requirements to entities owned ≥50% by sanctioned parties, even if not explicitly listed.

- EDD Trigger Criteria: FATF-aligned regimes require EDD for PEPs, high-risk jurisdictions, correspondent banking, and unusual ownership structures at onboarding.

- Record Retention Mandates: BSA recordkeeping rules require retaining CIP and CDD evidence five years after account closure, with immediate retrieval capability during exams.

Onboarding is where regulatory theory becomes operational reality. Miss a required step here, and you carry that compliance exposure for the life of the account

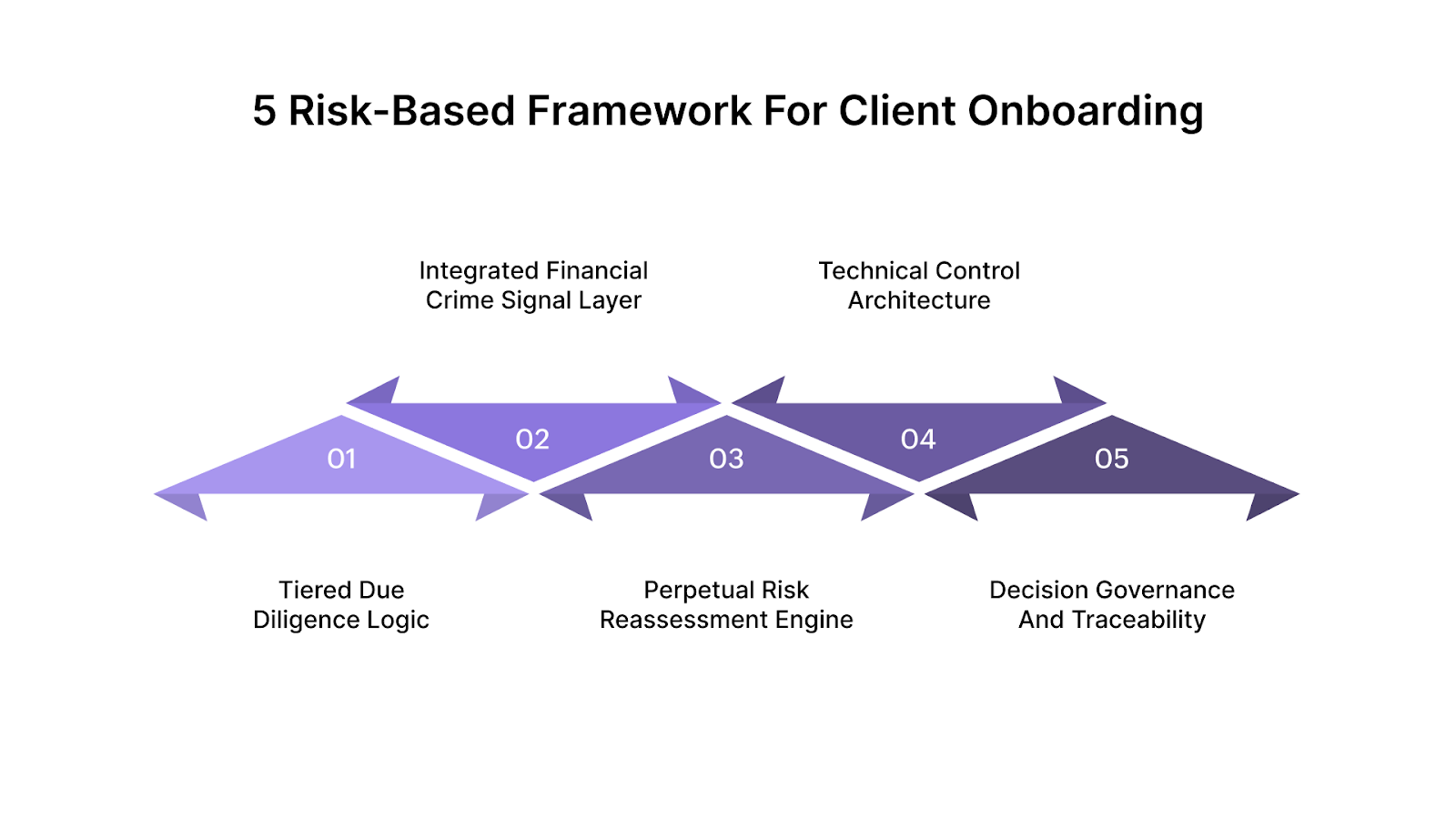

5 Risk-Based Framework for Client Onboarding

A risk-based onboarding framework dynamically adjusts verification depth using real-time risk signals, behavioral indicators, and jurisdictional exposure, preventing over-review of low-risk clients while escalating genuine financial crime risk early.

1. Tiered Due Diligence Logic

Tiered due diligence uses pre-defined risk thresholds to route applicants into automated approval, standard review, or improved investigation queues without unnecessarily slowing low-risk onboarding.

- Risk Score Thresholding: Numerical risk bands trigger workflow paths; scores combine geography, product type, ownership complexity, and sanctions proximity into automated routing decisions.

- Dynamic EDD Triggers: System escalates when PEP matches, high-risk country nexus, layered ownership, or adverse media hits exceed internal materiality thresholds.

- Straight-Through Guardrails: Low-risk applicants bypass manual review only when identity confidence, sanctions clearance, and device integrity checks exceed defined acceptance tolerances.

2. Integrated Financial Crime Signal Layer

This layer fuses identity, sanctions, behavioral, and ownership intelligence into a unified risk profile before account approval decisions are finalized.

- Biometric Identity Correlation: Facial biometrics must match the ID portrait, pass the liveness challenge, and avoid injection or replay artifacts flagged by presentation attack detection models.

- Real-Time Watchlist Resolution: Screening engines apply fuzzy logic, transliteration handling, and secondary identifiers to reduce false positives while preserving true sanctions match sensitivity.

- Ownership Structure Mapping: Graph analysis tools map shareholder chains, exposing circular ownership, nominee directors, or sanctioned exposure hidden across multi-jurisdictional entity layers.

3. Perpetual Risk Reassessment Engine

Risk evaluation does not stop at approval; customer profiles refresh automatically when new intelligence, behavioral changes, or regulatory list updates alter exposure.

- Event-Driven Re-Screening: Sanctions list updates, PEP status changes, or adverse media triggers automatically rescore customer risk without waiting for periodic reviews.

- Behavioral Drift Detection: Transaction pattern deviations from onboarding-declared purpose flag potential mule activity, account takeover, or undisclosed business model changes.

- Risk Model Recalibration: Periodic model tuning adjusts scoring weights using SAR outcomes, fraud losses, and regulator feedback to prevent model stagnation.

4. Technical Control Architecture

The framework depends on tightly integrated systems that move verified data, risk decisions, and documentation across compliance, fraud, and operations teams without duplication.

- Golden Record Enforcement: Master customer record synchronizes KYC, sanctions, and case data across systems, preventing conflicting risk assessments between onboarding and monitoring teams.

- Pre-Fill Data Orchestration: APIs pull verified internal and third-party data before user input, reducing manual entry while preserving data lineage for audit defensibility.

- Decision Rule Versioning: Every risk rule change is version-controlled with deployment timestamps, allowing regulators to trace historical decisions against active rule sets.

5. Decision Governance And Traceability

Every onboarding decision must be reproducible, explainable, and attributable to a defined control owner under regulatory review.

- Explainable Risk Outputs: Risk models generate factor-level explanations showing which signals drove escalation, approval, or rejection, supporting defensible compliance decisions.

- Case Escalation Attribution: High-risk approvals require a named compliance officer sign-off with a documented rationale linked to supporting evidence within the case system.

- Immutable Audit Logs: System logs capture data sources, screening timestamps, rule versions, and reviewer actions in tamper-evident storage for regulator retrieval.

A risk-based onboarding framework is not just smart automation; it is structured control logic, integrated intelligence, and accountable governance working together before financial access is granted.

If you want confidence that your onboarding program will stand up to sponsor bank, audit, and regulatory scrutiny, talk with Fraxtional about strengthening your controls before the next review.

Common Challenges in Client Onboarding for FinTech and Banking Teams

Designing onboarding today means juggling regulatory timing rules, fraud countermeasures, and real-time user drop-off risk, all while legacy ops and fragmented systems slow decisions.

If these issues are not engineered out of onboarding, growth creates compliance strain instead of operational power.

For teams aligning controls with audit expectations, the SOC 2 Compliance Checklist: Step-by-Step Guide to Pass Audit is a useful reference.

The Role of Technology in Modern Client Onboarding

Technology now orchestrates identity proofing, risk enrichment, workflow routing, and evidence capture in milliseconds, allowing institutions to scale onboarding volumes without weakening compliance control integrity.

- Biometric Signal Fusion: Systems combine face match, liveness challenge, device telemetry, and document forensics into a composite identity confidence score before workflow progression.

- Real-Time Data Enrichment: APIs pull sanctions context, business registry data, telecom validation, and IP geolocation during form completion, strengthening risk assessment without adding user steps.

- Workflow Orchestration Engines: Low-code decision platforms dynamically trigger document requests, manual review queues, or auto-approvals based on cumulative risk signals and product rules.

- Document Forensics Automation: Machine vision detects font inconsistencies, MRZ checksum failures, and pixel tampering to flag manipulated IDs before human review.

- Continuous Model Feedback Loops: Fraud outcomes and SAR dispositions retrain onboarding risk models, improving detection precision and reducing false-positive review burdens over time.

Modern onboarding tech does not just speed things up; it acts as an embedded control layer, strengthening fraud defense and regulatory consistency while customer volumes grow.

Why Compliance Leadership Is Critical to Onboarding Success

Technology runs the checks, but compliance leadership defines the rules, risk tolerance, and accountability model that determine whether onboarding decisions stand up to regulators and partner banks.

- Risk Appetite Translation: Leaders convert board-approved risk appetite into onboarding thresholds, escalation triggers, and approval authorities that frontline teams can consistently apply.

- EDD Approval Authority: Named compliance officers must sign off on high-risk customer approvals, documenting rationale that examiners can trace back to policy and risk models.

- Control Ownership Clarity: Leadership assigns first-line, second-line, and oversight responsibilities so that onboarding controls are not diluted between product, fraud, and compliance teams.

- Regulatory Change Implementation: New rules, consent orders, or enforcement trends must be quicklyembedded into onboarding procedures before the next regulatory exam cycle.

- Partner And Regulator Interface: Compliance leaders represent the institution in sponsor bank reviews and regulatory meetings, defending onboarding logic and remediation actions under scrutiny.

Without accountable leadership, onboarding becomes a tool-driven process with no one owning the risk. Regulators do not accept software as a responsible party; they expect people.

For a closer look at how due diligence expectations differ across segments, see KYC Compliance in Commercial Banking Explained.

What “Good” Client Onboarding Looks Like to Regulators

To regulators, “good” onboarding proves controls operate in practice, not just policy. They look for consistency, traceability, escalation discipline, and evidence that risk decisions follow documented logic.

- Consistent Decision Application: Similar risk profiles must produce similar onboarding outcomes; unexplained approval variance across analysts is a red flag during supervisory file testing.

- Clear Escalation Documentation: High-risk cases show documented review depth, supporting evidence, and policy-based rationale for approval or rejection, not generic analyst comments.

- Screening Quality Controls: Institutions demonstrate ongoing tuning of name-matching thresholds and alert handling procedures to balance false positives without weakening sanctions detection sensitivity.

- Ownership Transparency Evidence: Corporate onboarding files clearly show how control persons and ownership layers were verified, including resolution of nominee or intermediary structures.

- Control Effectiveness Testing: Internal QA or second-line reviews periodically re-perform onboarding checks to confirm frontline decisions align with procedures and regulatory expectations.

Regulators judge onboarding by how repeatable and defensible it is under file testing. If decisions cannot be reconstructed clearly, they assume the control failed.

How Fraxtional Helps Strengthen Client Onboarding Programs

Fraxtional embeds experienced compliance leaders into fintech, crypto, and banking teams to design, run, and defend onboarding programs under real regulatory and sponsor bank scrutiny.

- Embedded Compliance Officers: Fractional CCOs and BSA Officers oversee onboarding decisions, approve high-risk customers, and interface directly with regulators and sponsor bank compliance teams.

- Onboarding Procedure Buildouts: We translate regulatory requirements into step-by-step onboarding procedures, decision trees, and review standards that frontline analysts can execute consistently.

- Sponsor Bank Readiness Support: Directors prepare onboarding frameworks, risk summaries, and control documentation used in sponsor bank due diligence and ongoing partner oversight reviews.

- Licensing Control Alignment: For MTL and similar licenses, we align onboarding controls with state regulator expectations, ensuring identity, AML, and fraud processes match licensing representations.

- Independent Control Testing: Fraxtional performs targeted onboarding reviews to identify breakdowns, inconsistent decisions, or documentation gaps before regulators or partner banks find them.

Strong onboarding is not built by tools alone. It requires accountable leadership, operational structure, and regulator-ready documentation, which is where Fraxtional steps in.

Conclusion

Client onboarding financial services succeeds or fails based on whether risk decisions, identity verification, and escalation actions can be clearly defended under regulator and sponsor bank review. When onboarding controls are inconsistent or weakly evidenced, issues surface during exams, partnerships stall, and remediation becomes reactive instead of planned.

Fraxtional works alongside fintechs, banks, and crypto firms to strengthen digital client onboarding and overall client onboarding financial services frameworks, embedding experienced compliance leaders who build procedures, oversee decisions, and prepare programs to stand up to real regulatory and sponsor bank scrutiny.

Talk to Fraxtional to make sure your onboarding program is built for regulatory review, sponsor bank expectations, and sustainable growth.

FAQs

When onboarding uses automated risk scoring or AI-based identity tools, banks must validate models, document assumptions, test for bias, and maintain model governance under SR 11-7 and similar frameworks.

Vendors can perform checks, but regulatory accountability cannot be outsourced. Banks and fintechs must oversee vendor performance, tune screening thresholds, and document ongoing control validation.

Examiners often request raw identity verification outputs, screening match details, decision timestamps, rule versions, and analyst escalation notes, not just final approval status.

Onboarding risk ratings directly influence transaction monitoring thresholds. Weak initial risk scoring leads to mis-calibrated alerts, increasing false negatives or overwhelming compliance teams with noise.

Sponsor and correspondent banks review onboarding controls to assess downstream AML exposure, including identity proofing strength, sanctions logic, and high-risk customer approval governance.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.