Apr 13, 2026

Why Bank-Fintech Partnerships Fail: US Compliance & Approval Checklist (2026)

By Fraxtional LLC

Summarize the blog with AI

Most bank-fintech partnerships fail not because of weak products, but because fintechs lack a compliance program that a bank’s risk committee can defend to regulators.

Banks are not just evaluating your business model. They are assessing whether partnering with you creates regulatory exposure for them. The FDIC, OCC, and Federal Reserve have made third-party risk a supervisory priority, which means every bank's internal compliance and risk team is under heightened pressure to vet, document, and monitor every fintech they bring on board.

This guide is for fintech and crypto founders, CCOs, and legal teams aiming for sponsor bank relationships, investor audits, or licensing. Learn what banks look for, why partnerships fail, and how to build a compliance program that gets approved.

Quick look

- Bank-fintech partnerships are delayed or rejected mainly due to gaps in compliance documentation, risk assessment, and governance alignment.

- Banks evaluate fintechs through strict due diligence, focusing on AML controls, third-party risk management, and audit readiness.

- Regulatory scrutiny from agencies like FDIC, OCC, and FCA has increased oversight on partnership structures and ongoing compliance.

- Most failures occur during due diligence due to incomplete policies, weak controls, and lack of continuous monitoring systems.

- Fraxtional helps fintechs prepare for partnerships by building compliance frameworks, structuring documentation, and aligning with bank requirements.

Why Bank-Fintech Partnerships Are Harder to Close Than They Should Be

Fintech bank partnerships sit at the intersection of two fundamentally different operating cultures. Banks are built around regulatory accountability, audit trails, and documented controls. Fintechs are built around speed, iteration, and product-market fit. To secure a bank partnership, fintechs must operate on paper like regulated institutions.

The first challenge starts with how banks and fintechs approach risk and execution differently.

1. Misalignment Between Banks and Fintechs

Banks evaluate partnerships through a risk-first lens, while fintechs prioritize speed and product rollout.

- Banks require structured governance, controls, and auditability

- Fintechs often operate with evolving processes and limited compliance infrastructure

This gap creates friction during due diligence and onboarding.

2. Rising Regulatory Scrutiny

Regulators in the US and globally have increased oversight on bank-fintech relationships.

- Agencies like the FDIC, OCC, and Federal Reserve are focusing on third-party risk

- Joint guidance emphasizes due diligence, monitoring, and governance controls

- Enforcement actions frequently highlight gaps in AML and oversight programs

This means banks are now more cautious when approving fintech partners.

3. Lack of Compliance Maturity in Fintechs

Many fintechs approach partnerships without a fully developed compliance structure.

Common gaps include:

- Incomplete AML policies and procedures

- Weak documentation and audit trails

- No defined ownership of compliance responsibilities

These gaps become visible immediately during due diligence.

These challenges highlight why compliance readiness is not optional. To move forward, fintechs must meet specific regulatory expectations set by banks and supervisors.

What Banks Actually Require: Core Compliance Standards for Fintech Bank Partnerships

.jpg)

To secure and sustain a bank-fintech partnership, your compliance program must meet the same foundational standards as the bank's internal operations. Focus on excelling in the following non-negotiable areas, as every bank risk committee will evaluate them.

1. Third-Party Risk Management (TPRM)

Banks are required to manage risks introduced by fintech partners throughout the partnership lifecycle.

This includes:

- Pre-engagement due diligence covering financial, operational, and reputational factors

- Ongoing monitoring of performance, controls, and compliance adherence

- Clearly defined contractual obligations and accountability structures

Without a structured TPRM framework, fintech partnerships are unlikely to pass internal risk reviews.

2. AML and BSA Compliance

Anti-money laundering (AML) compliance is a core requirement for any fintech operating within a bank partnership model.

Key expectations include:

- Customer identification and verification (KYC) processes

- Transaction monitoring systems with defined alert thresholds

- Suspicious Activity Report (SAR) workflows and escalation protocols

- Beneficial ownership identification and verification

Banks expect fintechs to demonstrate these capabilities through documented processes and audit-ready systems.

3. Governance and Oversight

Strong governance structures are essential to ensure accountability and regulatory compliance.

Fintechs must establish:

- Clearly defined roles for compliance, risk, and operational teams

- Executive-level or board-level oversight of compliance functions

- Documented issue management and escalation procedures

Lack of governance clarity often leads to delays or rejection during due diligence.

4. Multi-Jurisdiction Regulatory Alignment

Fintechs operating across regions must ensure compliance consistency across regulatory frameworks.

Examples include:

- United States - BSA, FDIC, OCC regulatory requirements

- United Kingdom - FCA compliance standards

- European Union - AMLD and PSD regulations

Inconsistent regulatory alignment across jurisdictions increases risk exposure and complicates partnership approvals.

Meeting these requirements is only part of the process. Many fintechs still struggle to operationalize them effectively, which leads to common failure points during partnership execution.

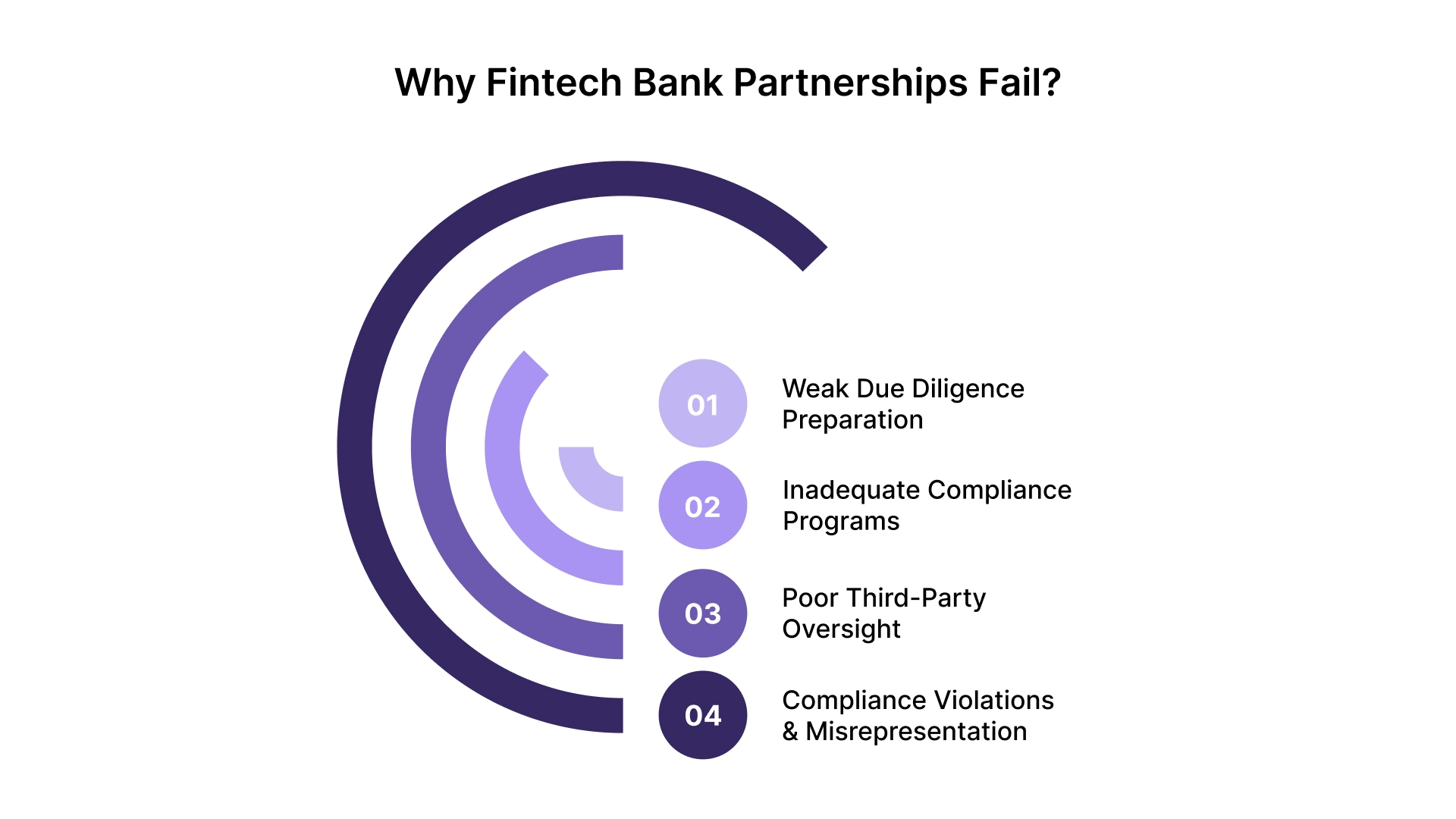

Why Fintech Bank Partnerships Fail: The Six Most Common Compliance Breakdowns

Even when fintechs meet baseline requirements, many partnerships fail during due diligence or early implementation. The issue is rarely a single gap, it is usually a combination of weak preparation, incomplete controls, and lack of ongoing oversight.

1. Weak Due Diligence Preparation

Many fintechs enter the due diligence process without complete or structured documentation. This leads to repeated requests, extended timelines, and reduced confidence from the bank.

Common issues include:

- Missing or outdated compliance policies: Fintechs often present policies that are outdated or incomplete, which makes it difficult for banks to assess compliance.

- No formal risk assessment reports: Lack of documented risk assessments, such as missing SARs (Suspicious Activity Reports), leaves banks unsure about the fintech’s ability to identify potential risks.

- Inconsistent documentation across teams: Teams may have misaligned or incomplete records, making it hard to present a unified compliance front. For example, no clear record of vendor oversight or third-party risk assessments.

2. Inadequate Compliance Programs

Banks frequently identify gaps in how compliance programs are designed and implemented. These gaps can range from incomplete frameworks to insufficient documentation, making fintechs appear as high-risk partners.

Typical gaps include:

- Incomplete AML frameworks: A fintech may have AML policies in place but may be missing critical components like transaction monitoring systems or SAR filing protocols.

- Lack of defined controls and testing mechanisms: Insufficient internal controls for anti-fraud measures or due diligence testing (e.g., no formal control matrix to manage ongoing risk).

- No audit-ready documentation: Fintechs may lack necessary documentation, such as complete audit trails or AML risk assessments, which banks require to verify compliance and mitigate risk.

3. Poor Third-Party Oversight

Fintechs often lack systems to monitor and manage compliance on an ongoing basis. This issue becomes particularly evident when the fintech relies on third-party vendors or contractors without sufficient oversight, which exposes both the fintech and the bank to risk.

Key gaps include:

- No continuous monitoring of compliance activities: Failure to monitor transactions or implement automated risk detection systems, leaving the fintech exposed to unreported risks.

- Limited reporting and visibility into risk issues: Banks require ongoing visibility into risk activities, but many fintechs fail to report regularly or sufficiently, which complicates their evaluation.

- Absence of formal escalation and remediation processes: Lack of clear protocols for addressing compliance failures such as missing audit findings or regulatory alerts, means issues are not escalated promptly.

4. Compliance Violations and Misrepresentation

Issues in customer-facing processes and disclosures can raise immediate regulatory concerns. Misleading claims or inadequate consumer protection measures are significant reasons for partnership rejection.

Examples include:

- Misleading product or marketing claims: Offering services or products that do not meet regulatory standards or misrepresenting the company’s capabilities. For instance, fintechs might advertise a “fully compliant” AML system that lacks critical real-time monitoring features.

- Inaccurate disclosures related to banking services: Providing incorrect or incomplete information to banks or regulators about the fintech’s capabilities, such as undisclosed risks in cross-border transactions or unreported fraud cases.

- Weak consumer protection controls: Failing to implement robust consumer data protection practices, which can lead to data breaches or violations of consumer privacy laws.

Fintechs facing these gaps can benefit from Fraxtional’s fractional compliance leadership, providing CCO and CRO-level expertise to structure risk and governance. This includes building compliance frameworks, preparing due diligence documentation, and aligning with bank expectations.

These common breakdowns highlight why a structured and comprehensive approach to compliance is essential for success. Now, let’s look into a practical framework to help fintechs build a bank-ready compliance program in five actionable steps.

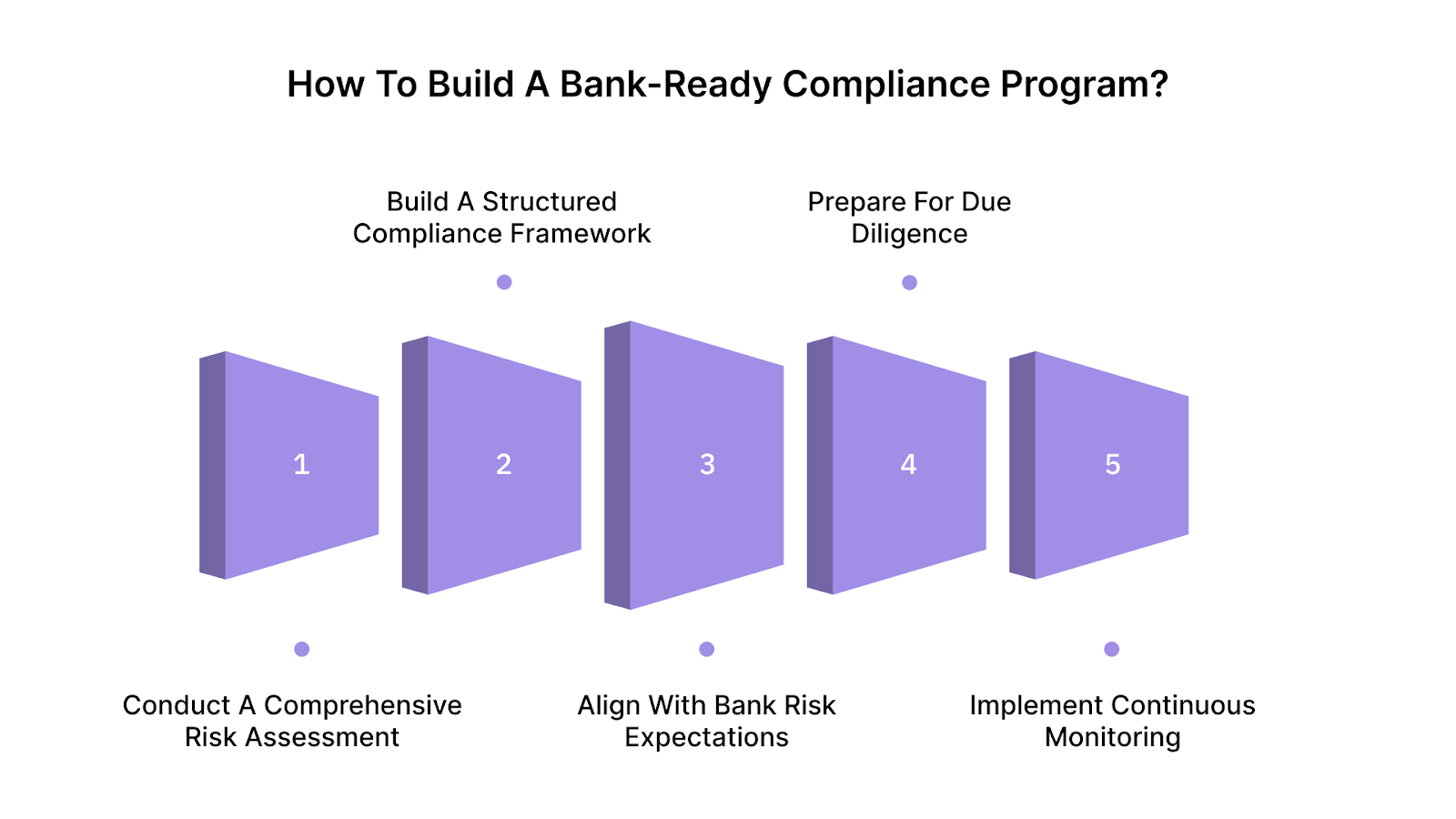

How to Build a Bank-Ready Compliance Program: A Five-Step Framework

A structured approach to compliance directly aligns with how banks evaluate risk and regulatory readiness. When fintechs follow and document a clear process, they can move through due diligence efficiently and reduce approval delays.

The following steps will help you build a compliance program that meets bank expectations with confidence:

Step 1: Conduct a Comprehensive Risk Assessment

Start by identifying all relevant risks across your product, operations, and regulatory exposure.

This includes:

- Operational risks: Assess risks related to your core systems, processes, and third-party providers.

- Regulatory risks: Determine the regulations that apply to your fintech in different jurisdictions (e.g., AML, GDPR).

- Product-specific risks: Identify risks related to your fintech’s offerings, such as transaction fraud, credit risk, or data privacy.

This risk assessment should be documented and form the foundation for your compliance framework.

Example:

- For Startups: At an early stage, focus on basic risks such as identifying key regulatory obligations (e.g., AML and KYC).

- For Scale-ups: As your fintech grows, include a more detailed risk assessment, especially around cross-border operations and third-party vendor risks.

Step 2: Build a Structured Compliance Framework

Develop a framework that clearly defines how compliance is managed across the organization.

Key components include:

- Drafting policies and procedures: Cover major compliance areas like AML, risk management, and governance.

- Implementing controls: Establish preventive, detective, and corrective controls to mitigate risks.

- Creating documentation standards: Ensure all processes align with audit and regulatory requirements.

All elements must be consistent, version-controlled, and accessible.

Example:

- For Startups: Start by drafting core policies in AML and KYC and align them with your key operational needs.

- For Scale-ups: Develop a more comprehensive framework, including policies on transaction monitoring, third-party risk assessments, and data protection.

Step 3: Align With Bank Risk Expectations

Banks assess fintechs based on how well their compliance programs align with internal risk standards.

To achieve alignment:

- Understanding the bank’s risk appetite: Learn about the bank's risk framework and control requirements.

- Matching governance structures: Ensure your internal governance aligns with the bank’s expectations.

- Clarifying roles and responsibilities: Define who is responsible for each compliance task within your organization.

Misalignment at this stage is a common cause of delays.

Example:

- For Startups: Align your governance structure with basic bank requirements and define roles for AML and KYC tasks.

- For Scale-ups: Formalize roles and responsibilities, ensuring dedicated teams for AML monitoring, internal audits, and risk management.

Step 4: Prepare for Due Diligence

Due diligence is where most fintechs face delays due to incomplete preparation.

Be ready with:

- Organizing compliance documentation: Ensure you have complete documentation, including AML policies, risk assessments, and audit logs.

- Preparing risk assessment reports: Demonstrate how risks are identified and mitigated.

- Ensuring audit-ready logs: Keep logs of compliance activities, such as customer verifications and SAR filings.

Example:

- For Startups: Focus on collecting basic compliance documentation, including draft AML policies and risk assessment reports.

- For Scale-ups: Ensure comprehensive documentation, including full audit trails, third-party risk assessments, and financial compliance reports.

Step 5: Implement Continuous Monitoring

Compliance is an ongoing requirement, not a one-time setup.

This includes:

- Monitoring compliance activities: Set up continuous tracking for transactions, KYC verification, and suspicious activity monitoring.

- Tracking issues and remediation: Implement a system to identify and resolve compliance-related issues.

- Establishing reporting systems: Create reports on compliance status for internal stakeholders and banks.

Example:

- For Startups: Set up basic monitoring tools to track high-priority activities such as KYC checks and fraud prevention.

- For Scale-ups: Implement automated monitoring systems to track all compliance activities in real-time, with alerts for suspicious transactions.

Use the checklist below to self-assess your current readiness and identify areas for improvement.

Bank Partnership Readiness Checklist:

Building a compliance program is not only about meeting initial requirements. It directly impacts how quickly partnerships are approved and how effectively they scale over time.

To make this more practical, let’s explore how fintechs at different stages can approach compliance readiness. Whether you’re a startup just starting to build your program or a scale-up preparing for a bank partnership, the steps you take next can make all the difference.

Stage-Based Scenarios: What to Do Next at Different Fintech Stages

Fintechs at different stages have different needs when preparing for bank partnerships. Here’s how fintechs should approach compliance readiness depending on whether they are a startup or a scale-up.

Scenario 1: Startup Fintech (Pre-Approval Stage)

Key Needs: Basic compliance setup, initial risk assessment, and foundational policies.

- What to Do Next:

- Build a Risk Register to identify early-stage operational risks (e.g., platform downtime, third-party provider risks)

- Draft Initial AML Policies, covering KYC, transaction monitoring, and reporting obligations

- Assign a Dedicated CCO/CRO (even on a fractional basis) to oversee early compliance functions

- Create an Org Chart to clearly define compliance roles and responsibilities

Supporting Tools:

- Risk Register Template

- Draft AML Policy Outline

- Org Chart Template for CCO/CRO Roles

Scenario 2: Scale-Up Fintech (Post-Funding, Pre-Bank Partnership)

Key Needs: A more mature compliance framework, preparation for due diligence, and readiness for multi-jurisdictional compliance.

- What to Do Next:

- Review and Update AML Framework, ensuring it is audit-ready and aligned with bank expectations (e.g., add more detailed transaction monitoring procedures)

- Create a Control Matrix that outlines key controls, testing procedures, and escalation mechanisms for risk and compliance

- Ensure Ongoing Compliance Monitoring Systems are in place to track compliance activities and report issues promptly

- Conduct Due Diligence Mock Audits to test readiness for bank reviews

Supporting Tools:

- Updated Control Matrix

- AML Policy Full Version (with appendices for reporting, KYC, etc.)

- Ongoing Monitoring System Overview

- Due Diligence Checklist

These scenarios highlight the steps fintechs must take at different growth stages to ensure they meet compliance and regulatory requirements.

Let’s explore how a solid compliance framework can accelerate approval and strengthen long-term partnerships.

How Strong Compliance Accelerates Bank Approval?

Strong compliance isn't just about meeting requirements, it's a key driver of faster approvals, smoother partnerships, and sustainable growth. Fintechs with structured compliance programs see fewer delays, align better with banks, and strengthen their position in the market.

- Faster approvals: Complete, well-organized due diligence packages reduce information request cycles and can cut onboarding timelines from six months to six weeks.

- Multiple partnership options: A bank-ready compliance program makes you a credible candidate for multiple bank relationships, giving you negotiating leverage.

- Investor confidence: Institutional investors conducting compliance due diligence on fintech portfolios reward programs with documented governance, tested controls, and clear CCO ownership.

- Regulatory resilience: A documented, continuously monitored compliance program is the best protection against enforcement action, for you and for your bank partner.

- Scalable growth: Standardized compliance frameworks that align with US, UK, and EU requirements enable multi-market expansion without rebuilding your program from scratch in each jurisdiction.

These outcomes highlight why compliance is a critical enabler for partnerships, and where structured execution support can make a measurable difference.

How Fraxtional Supports Bank-Fintech Partnerships?

Fraxtional provides experienced compliance and risk professionals who embed directly into fintech and crypto companies, functioning as fractional CCOs and CROs rather than external consultants. This approach delivers leadership that is accountable, operational, and timeline-aligned.

Here’s how Fraxtional can assist:

- Fractional CCO and CRO leadership: Providing hands-on guidance to define and implement a comprehensive compliance strategy and governance framework.

- Compliance framework development: Building tailored frameworks that include AML procedures, risk assessments, and policy documentation, ensuring they meet both regulatory and bank partner requirements.

- Bank partnership readiness support: Helping fintechs prepare for due diligence, organizing audit-ready documentation, and aligning with bank compliance expectations for smooth approval processes.

- Ongoing compliance oversight and monitoring: Offering continuous compliance reporting and monitoring to ensure alignment with evolving regulatory expectations.

- Regulatory expertise across regions: Navigating complex regulatory landscapes in the US, UK, EU, and other markets to ensure compliance in every jurisdiction fintechs operate within.

With structured compliance leadership and execution in place, fintechs can move through approvals with fewer delays. This improves partnership outcomes and reduces long-term regulatory risk.

Wrapping Up

Bank-fintech partnerships depend on strong alignment in compliance, risk management, and governance. Most delays and failures occur due to gaps in due diligence preparation, weak AML frameworks, and lack of ongoing oversight.

Fraxtional provides fractional compliance leadership and execution support tailored to fintech and financial services companies. It helps build risk and compliance frameworks, prepare for bank due diligence, and ensure ongoing regulatory alignment.

With experienced CCO and CRO support, fintechs can meet bank expectations without hiring full-time teams.

If your fintech is preparing for a bank partnership and needs structured compliance support, Contact us Today.

FAQs

A sponsor bank provides the regulatory framework that allows fintechs to offer financial services without holding a banking license. It enables access to payment rails, deposit accounts, and lending infrastructure. The bank also retains compliance responsibility for regulated activities.

Banks evaluate fintechs across financial stability, operational capability, compliance maturity, and risk exposure. This includes reviewing policies, audit records, and internal controls. They also assess the fintech’s ability to meet ongoing regulatory requirements.

Fintechs must adapt their controls, governance, and processes to match the bank’s defined risk thresholds. This includes aligning on customer onboarding, transaction monitoring, and reporting standards. Clear documentation and consistency are critical for approval.

Operational risks include system integration failures, data security issues, and breakdowns in process controls. Gaps in communication and responsibility between the bank and fintech can increase exposure. These risks must be identified and managed through structured controls.

Yes, but managing multiple bank partnerships increases complexity in compliance and operations. Each bank may have different requirements, risk frameworks, and reporting expectations. Fintechs must ensure consistency and avoid conflicts across partnerships.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.