Mar 27, 2026

Risk Management Strategies Businesses Should Use in 2026

By Fraxtional LLC

A weak risk program rarely fails all at once. It usually starts with a missed control, an unchecked vendor, a delayed escalation, or a compliance issue that leadership assumed was under control. For fintechs, banks, and other regulated businesses, those small gaps can become expensive very quickly.

In 2026, risk sits closer to growth than many leadership teams expect. A new banking partner, a higher transaction volume, a product launch, or a new market entry can all increase operational, compliance, fraud, and third-party exposure at the same time. That is why risk management strategies can no longer sit in a static policy document.

The real challenge is not listing risks. It is deciding which risks matter most, assigning the right response, and building enough oversight to keep the business stable as it scales. This guide breaks down the strategies businesses should use in 2026 and how to apply them in practice.

At a glance

- Businesses should categorize risks across operations, compliance, finance, and third-party vendors before selecting a response strategy.

- The four standard responses to risk are avoidance, mitigation, transfer, and acceptance, depending on likelihood and impact.

- Effective risk management strategies include risk registers, scoring models, internal controls, vendor oversight, scenario testing, and continuous monitoring.

- Leadership oversight is critical; many organizations assign ownership to a CRO, Head of Compliance, or dedicated risk leader.

- Fraxtional supports regulated businesses by providing fractional compliance and risk leadership to structure governance and manage regulatory exposure.

Why Risk Management Matters More in 2026

The business risk environment is more layered than it was a few years ago. Companies now face tighter regulatory expectations, deeper digital dependencies, and greater exposure to third-party vendors across payments, onboarding, cloud infrastructure, and fraud tools.

For regulated businesses, the cost of weak risk management goes beyond operational disruption. It can affect audit outcomes, sponsor bank relationships, licensing timelines, and customer trust. IBM reported that the global average cost of a data breach reached $4.4 million in 2025, showing how quickly a control failure can become a financial problem.

This pressure is even higher for growth-stage fintechs. As products expand and transaction volumes increase, risk exposure often grows faster than internal governance.

Many companies eventually reach a stage where informal oversight no longer works, making structured risk management essential.

To build an effective strategy, the first step is identifying the types of risks businesses need to plan for.

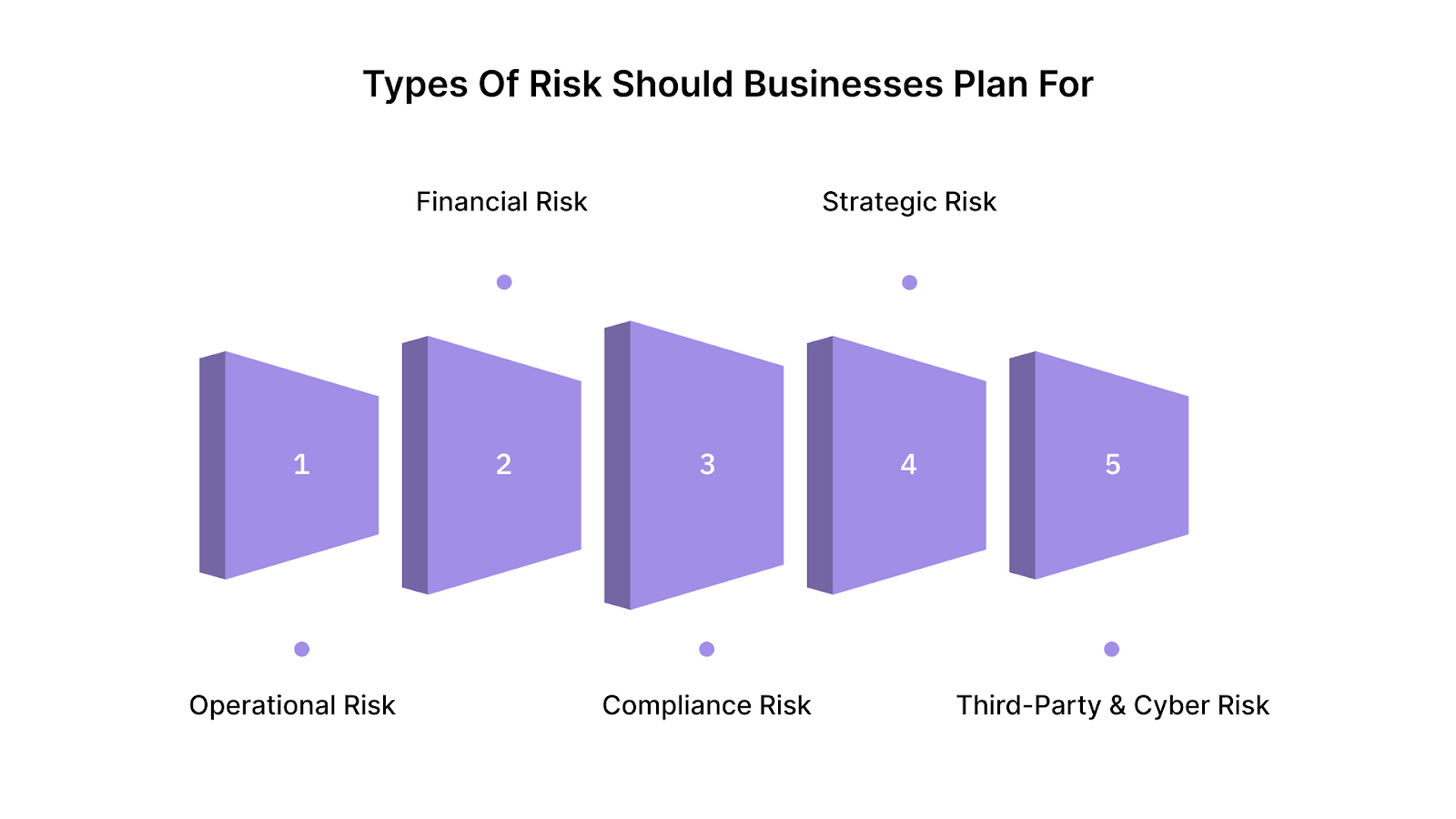

What Types of Risk Should Businesses Plan For?

An effective risk strategy starts by categorizing the risks that could affect the business. Clear categories help leadership prioritize responses and allocate resources efficiently.

1. Operational Risk

Operational risk arises from failures in internal processes, systems, or personnel. Examples include system outages, manual errors in reconciliation, or delays in transaction processing.

For example, a fintech relying on a single approval step for high-value transactions may expose itself to operational risk if that control fails.

2. Financial Risk

Financial risk involves potential losses tied to fraud, liquidity issues, or inaccurate reporting. Payment disputes, chargebacks, and credit exposure are common examples.

If fraud attempts increase faster than monitoring systems can detect them, financial losses can escalate quickly.

3. Compliance Risk

Compliance risk occurs when businesses fail to meet regulatory requirements. In financial services, this can include weak AML controls, incomplete reporting, or outdated policies.

These gaps can trigger regulatory scrutiny, remediation efforts, or delays in licensing approvals.

4. Strategic Risk

Strategic risk emerges when business decisions create avoidable exposure. Entering a new market without proper regulatory preparation or scaling operations too quickly can fall into this category.

Strategic missteps often appear when companies prioritize growth without aligning governance structures.

5. Third-Party and Cyber Risk

Modern businesses rely heavily on external vendors and digital infrastructure. Weak vendor oversight, cloud vulnerabilities, or poor cybersecurity practices can expose organizations to data breaches or operational disruption.

Once these risk categories are defined, businesses must determine how to respond to them effectively.

The 4 Core Risk Responses Every Business Should Know

Most risk decisions fall into four response categories. Choosing the right one depends on the likelihood and impact of the risk involved.

1. Risk Avoidance

Risk avoidance removes exposure entirely by eliminating the activity creating the risk.

Example: A fintech delays launching in a new market until licensing requirements are fully clarified.

2. Risk Mitigation

Risk mitigation reduces the likelihood or impact of a risk through controls, policies, or monitoring.

Example: Adding multi-factor authentication and transaction monitoring to reduce fraud attempts.

3. Risk Transfer

Risk transfer shifts some exposure to another party through contracts, outsourcing, or insurance.

Example: Purchasing cyber insurance or outsourcing specialized compliance monitoring.

4. Risk Acceptance

Risk acceptance acknowledges a risk but chooses not to act immediately because the impact is low.

Example: Accepting minor internal process delays while monitoring them regularly.

Understanding these responses allows businesses to apply more structured strategies for managing risk across operations.

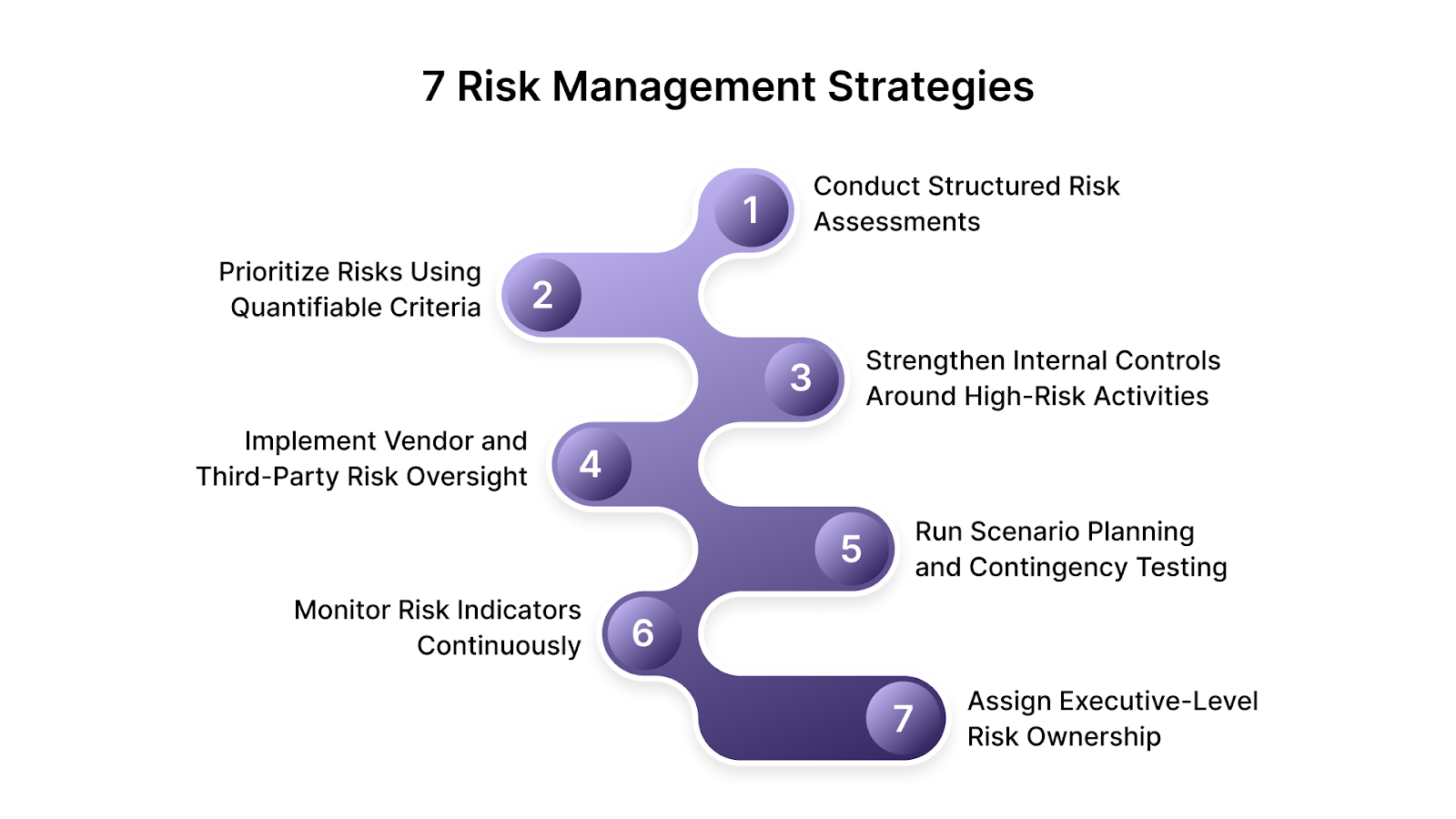

7 Risk Management Strategies Businesses Should Use in 2026

Strong risk programs do not rely on one tactic. They combine structured assessments, control design, and leadership oversight to address operational, financial, and regulatory exposure.

The following strategies reflect how businesses in regulated environments manage risk in practice.

1. Conduct Structured Risk Assessments

Risk assessments should go beyond periodic checklists. Businesses should run function-level assessments covering operations, compliance, finance, cybersecurity, and vendor relationships.

Each review should map risks to specific workflows such as onboarding, transaction processing, reporting, or vendor access.

Document findings in a risk register that includes the risk description, owner, likelihood score, potential financial or regulatory impact, and mitigation plan. Updating this register quarterly helps leadership track unresolved issues and identify emerging risks early.

2. Prioritize Risks Using Quantifiable Criteria

Not every risk requires immediate remediation. Leadership teams should rank risks using a structured scoring framework that considers likelihood, operational impact, financial loss potential, regulatory exposure, and reputational consequences.

For example, a high-probability fraud vulnerability in onboarding may score higher than a rare system outage risk because of direct financial and compliance implications. Using a standardized scoring model ensures risk prioritization is consistent across departments.

3. Strengthen Internal Controls Around High-Risk Activities

Internal controls are the operational backbone of a risk program. Controls should focus on areas where financial loss, fraud, or regulatory exposure is most likely.

Examples include:

- Dual approvals for high-value transactions or vendor payments

- Segregation of duties between transaction initiation and reconciliation

- Automated transaction monitoring rules for unusual behavior patterns

- Periodic access reviews for employees handling financial or customer data

These controls create accountability and reduce the likelihood that a single failure can lead to major exposure.

4. Implement Vendor and Third-Party Risk Oversight

Many modern businesses rely heavily on external providers for payments, identity verification, cloud hosting, and fraud monitoring. Weak vendor oversight can create operational and compliance risks even when internal controls are strong.

An effective third-party risk process should include:

- pre-contract due diligence assessments

- review of security and compliance documentation

- service-level performance monitoring

- incident reporting requirements

- periodic vendor reassessments

This is especially important for fintech companies that depend on payment processors or onboarding partners.

5. Run Scenario Planning and Contingency Testing

Risk programs should test real-world disruption scenarios rather than relying solely on documentation. Scenario planning allows leadership teams to evaluate response readiness before incidents occur.

Common exercises include:

- simulating a payment processor outage

- testing response to a fraud spike

- evaluating procedures for data access incidents

- running tabletop exercises for regulatory investigations

These simulations help clarify escalation procedures and expose gaps in communication or decision-making.

6. Monitor Risk Indicators Continuously

Risk monitoring should occur continuously rather than only during audits or compliance reviews. Organizations should track measurable indicators that signal rising exposure.

Examples of key risk indicators include:

- increases in fraud attempts or chargebacks

- repeated control failures

- unresolved audit findings

- vendor service disruptions

- abnormal transaction patterns

Monitoring these indicators enables leadership to identify emerging risks early and adjust controls before issues escalate.

7. Assign Executive-Level Risk Ownership

Risk programs often fail because ownership is fragmented across departments. Each major risk category such as compliance, operational risk, fraud risk, or vendor risk, should have a clearly defined owner responsible for oversight and reporting.

In larger organizations this responsibility may sit with a Chief Risk Officer or Head of Compliance. Growth-stage companies may rely on fractional risk leadership to establish governance structures until a full-time role becomes necessary.

Many companies address this gap by working with Fraxtional, which provides experienced compliance and risk leaders on a fractional basis. These executives help structure governance, conduct risk assessments, and guide regulatory readiness without requiring a full-time hire.

Once these strategies are in place, businesses can better translate risk planning into practical decision-making across operations.

Examples of Risk Management Strategies in Practice

Risk management strategies become clearer when you apply them to real operational situations. The following examples show how businesses typically respond when a risk becomes visible.

1. Fraud Monitoring Example

You may notice an increase in synthetic identity fraud during customer onboarding. When that happens, the response is not limited to investigation but control improvement.

You can strengthen identity verification, add behavioral monitoring, and introduce transaction alerts for unusual patterns. This is a risk mitigation strategy, where you reduce the likelihood and impact of fraud through stronger controls.

2. Vendor Risk Example

You may discover that a critical vendor lacks clear incident reporting procedures. If that vendor supports payments, onboarding, or infrastructure, the risk can affect your entire operation.

You can respond by tightening vendor oversight, requiring stronger reporting obligations, or adding an alternative provider to reduce dependency. This approach reduces vendor concentration risk and improves operational resilience.

3. Low-Impact Risk Example

Not every issue requires immediate remediation. You might identify a minor reporting delay in an internal workflow that does not affect compliance or financial accuracy.

In this situation, the practical response is to document the issue, monitor it periodically, and review it during governance meetings.

This reflects a risk acceptance strategy, where the exposure is acknowledged and tracked rather than immediately eliminated.

Applying these responses consistently requires a structured process that ensures risks are identified, prioritized, and managed across the organization.

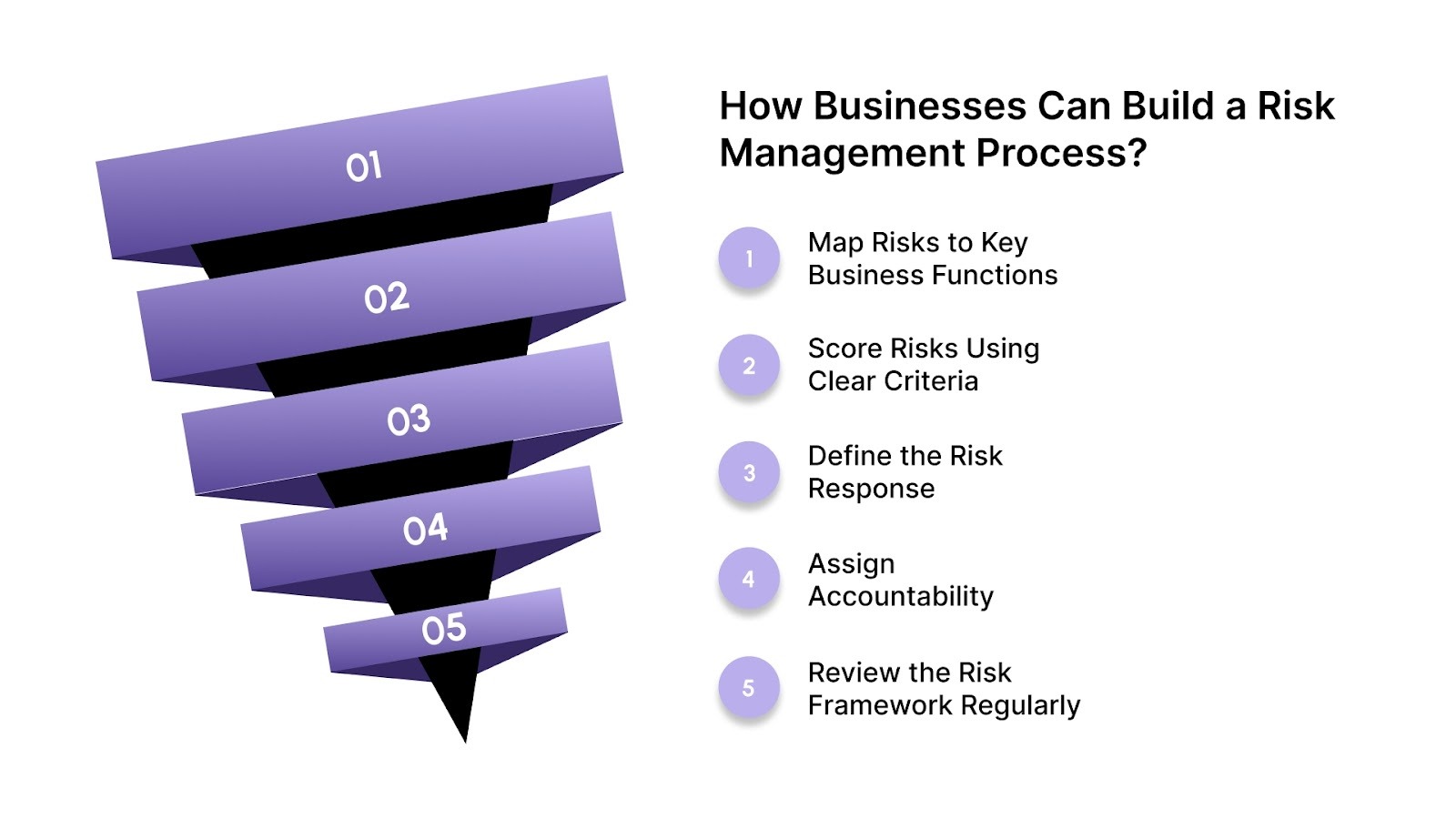

How Businesses Can Build a Risk Management Process That Works

Risk management works best when it follows a defined process. Without structure, risks are often addressed only after they disrupt operations or trigger compliance issues. A clear framework helps leadership detect exposures early and respond before they escalate.

Step 1: Map Risks to Key Business Functions

Identify risks across functions where failures can create financial or regulatory exposure. For many fintech and financial companies, this includes customer onboarding, payment processing, transaction monitoring, vendor integrations, and data access systems.

Document these risks in a central risk register with details such as the affected process, potential impact, and the responsible team.

Step 2: Score Risks Using Clear Criteria

Evaluate risks based on likelihood, financial exposure, operational disruption, and regulatory impact. A scoring model helps leadership distinguish between minor operational issues and risks that could affect licensing, reporting obligations, or fraud exposure.

Step 3: Define the Risk Response

Each risk should have a documented response strategy. Most organizations apply four responses: avoid, mitigate, transfer, or accept.

For example, fraud exposure may be mitigated through stronger monitoring controls, while regulatory risk may be avoided by delaying entry into a new market.

Step 4: Assign Accountability

Every major risk should have an owner responsible for monitoring controls and reporting unresolved issues. In regulated businesses, this often sits with compliance leaders, risk managers, or operational heads overseeing payments and onboarding workflows.

Step 5: Review the Risk Framework Regularly

Risk registers and controls should be reviewed periodically to reflect operational changes. Many companies run quarterly risk reviews to evaluate control failures, vendor performance issues, and emerging regulatory exposure.

With a structured process in place, businesses can manage risks systematically rather than reacting to problems after they occur.

How Fraxtional Supports Risk Management for Regulated Businesses?

Fraxtional provides fractional risk and compliance leadership to fintech companies, banks, crypto firms, and private-equity backed financial businesses. Instead of hiring a full-time executive, companies gain access to experienced compliance leaders who guide risk programs, regulatory readiness, and governance.

This model allows organizations to strengthen compliance oversight and risk management without the cost or delay of a permanent executive hire.

Fraxtional services include:

- Fractional Compliance Leadership (CCO, CRO, CAMLO, MLRO): Senior executives embed into your leadership team to oversee compliance programs, risk governance, and regulatory escalation processes.

- AML and Financial Crime Compliance Programs: Development and oversight of AML frameworks, transaction monitoring controls, SAR reporting processes, and sanctions screening programs.

- Risk Assessments and Compliance Program Development: Enterprise risk assessments, policy and procedure development, and governance frameworks aligned with regulatory expectations.

- Licensing and Regulatory Readiness Support: Guidance for money transmitter licensing, regulatory examinations, and preparation for sponsor bank or regulator reviews.

- SOC 2 Readiness and Independent Audit Support: Assistance with control documentation, audit preparation, and compliance program maturity for regulated financial organizations.

- Sponsor Bank Partnership and Regulatory Advisory: Support for fintech companies working with sponsor banks, including compliance program alignment and reporting oversight.

Strong risk management requires experienced oversight and structured governance. Fraxtional helps regulated businesses build those capabilities while maintaining flexibility as the company grows.

Wrapping Up

Businesses face growing exposure to fraud, compliance obligations, vendor dependencies, and operational failures. Strong risk management strategies help organizations identify high-impact risks early and implement controls that protect operations and regulatory standing.

Fraxtional provides fractional compliance and risk leadership for fintech companies, banks, and regulated financial businesses. Their experienced executives help build risk frameworks, conduct assessments, and strengthen governance without hiring a full-time leader.

Contact Today to learn how Fraxtional can help your organization strengthen risk oversight and build a structured compliance program.

FAQs

1. What is the difference between risk management and risk mitigation?

Risk management is the broader process of identifying, evaluating, and managing risks across a business. Risk mitigation is one specific response within that process, focused on reducing the likelihood or impact of a particular risk through controls or safeguards.

2. How do companies measure the effectiveness of a risk management program?

Organizations often track metrics such as control failures, incident response times, unresolved audit findings, and fraud loss trends. These indicators help leadership evaluate whether risk controls are working as intended.

3. What is a risk register and why do companies use it?

A risk register is a centralized document that lists identified risks, their potential impact, and assigned owners. It helps organizations track mitigation efforts, monitor unresolved issues, and maintain visibility across leadership teams.

4. How does third-party risk affect regulated businesses?

Vendors that handle payments, infrastructure, or customer data can introduce operational and compliance risks. If a vendor experiences a failure or security incident, it can disrupt operations or trigger regulatory scrutiny for the business relying on that provider.

5. When should a company bring in external risk or compliance leadership?

Many organizations seek external leadership when internal teams lack specialized regulatory expertise or when growth increases oversight requirements. Fractional risk or compliance leaders can help establish governance frameworks and manage regulatory expectations.

FAQs

Risk management is the broader process of identifying, evaluating, and managing risks across a business. Risk mitigation is one specific response within that process, focused on reducing the likelihood or impact of a particular risk through controls or safeguards.

Organizations often track metrics such as control failures, incident response times, unresolved audit findings, and fraud loss trends. These indicators help leadership evaluate whether risk controls are working as intended.

A risk register is a centralized document that lists identified risks, their potential impact, and assigned owners. It helps organizations track mitigation efforts, monitor unresolved issues, and maintain visibility across leadership teams.

Vendors that handle payments, infrastructure, or customer data can introduce operational and compliance risks. If a vendor experiences a failure or security incident, it can disrupt operations or trigger regulatory scrutiny for the business relying on that provider.

Many organizations seek external leadership when internal teams lack specialized regulatory expertise or when growth increases oversight requirements. Fractional risk or compliance leaders can help establish governance frameworks and manage regulatory expectations.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.