Sep 19, 2025

Fractional Compliance Officer: A 2026 Guide for FinTech Leaders Scaling Risk

By Fraxtional LLC

Summarize the blog with AI

For many FinTech leaders, compliance stops being a back-office function the moment growth accelerates.

New products invite new risks. Sponsor banks raise expectations. Investors ask sharper questions. Regulators expect clear ownership, not just tools or policies. Yet hiring a full-time Chief Compliance Officer too early can strain budgets and lock companies into leadership structures they are not ready to sustain.

U.S. regulators such as the Financial Crimes Enforcement Network (FinCEN) and the Federal Reserve require compliance with evolving rules that fintech companies must address to meet regulatory deadlines and avoid fines.

This tension is why the fractional compliance officer model has gained traction across FinTech, crypto, and payments companies in the United States. It offers experienced compliance leadership without forcing an all-or-nothing executive hire.

This guide breaks down who exactly a fractional compliance officer is, how FinTech leaders are using them, when the model works and when it does not, and what stakeholders expect to see before they trust it.

Key Takeaways

- Fractional compliance officers work when timing, not cost, is the driver. They provide senior oversight as scrutiny rises, but a full-time CCO remains premature.

- Regulators and sponsor banks judge authority, not job titles. Fractional leadership is credible only when independence, escalation rights, and accountability are clear.

- The real risk isn't fractional vs full-time, it's misalignment. Choosing the wrong model for your growth stage creates governance gaps that slow momentum.

- Strong fractional compliance is decision-led, not task-heavy. The role exists to own risk judgments and oversight, not to run daily operations.

- Automation proves controls; leadership defends them. The most resilient compliance programs combine tooling efficiency with experienced human judgment.

Why Compliance Leadership Became a Scaling Bottleneck for FinTech

As FinTech companies grow, compliance stops being a support function and becomes a growth constraint.

In the U.S., FinTechs operate under overlapping federal and state oversight. Depending on the business model, this can include FinCEN, the CFPB, state banking departments, securities regulators, and AML/BSA enforcement bodies. Each adds reporting, monitoring, and governance expectations that evolve year over year.

This is not a marginal burden.

More than 90% of compliance professionals at FinTechs find meeting regulatory requirements “somewhat or very challenging." Around 86% reported paying more than $50,000 in compliance fines last year, and over one-third spent more than $500,000, showing how non-compliance directly impacts financial performance.

The takeaway is simple: compliance risk scales faster than headcount.

Product Growth Often Outruns Governance

Early-stage FinTechs are built to move quickly. Teams iterate, expand into new states, add partners, and launch features on tight timelines. Compliance functions rarely grow at the same pace.

As a result, responsibility fragments:

- Policies exist, but ownership is unclear

- Risk assessments are performed, but not connected to the strategy

- Regulators and banks receive responses, but without consistent executive accountability

Without senior oversight, compliance becomes reactive. That slows approvals, complicates audits, and increases exposure during sponsor bank reviews.

Compliance Risk Now Signals Business Maturity

For investors and sponsor banks, compliance is no longer evaluated in isolation. It is used as a proxy for how well a company manages risk overall.

Weak compliance leadership can affect:

- Valuation during fundraising or acquisition

- Willingness of banks to sponsor or expand partnerships

- Speed of licensing and regulatory approvals

- Credibility with regulators during exams or inquiries

In short, compliance leadership has become a bottleneck because it sits at the intersection of growth, trust, and control. Companies that treat it as an afterthought feel the constraint. Companies that address it strategically regain momentum.

Suggested Read: What a Fractional CCO Does & Why It Matters for Your Business?

That gap between growth and governance is exactly where fractional compliance leadership comes into play.

What Is a Fractional Compliance Officer?

A fractional compliance officer is a senior compliance leader who operates with executive authority on a part-time or scoped basis. The role exists to provide governance, regulatory judgment, and accountability, not to replace internal teams or automate compliance work.

At its core, a fractional compliance officer provides the same leadership functions regulators expect from a full-time executive, including:

- Ownership of the compliance program and risk framework

- Interpretation of regulatory requirements as the business evolves

- Oversight of AML, BSA, fraud, and consumer compliance functions

- Executive-level communication with regulators, sponsor banks, and auditors

- Reporting to founders, boards, or investors on compliance risk

From a regulator's perspective, the key issue is not hours worked. It is authority and independence. Regulators have repeatedly emphasized that compliance leadership must have direct access to senior management and the ability to escalate issues without obstruction.

That expectation applies regardless of whether the role is full-time or fractional.

What a Fractional Compliance Officer Is Not

A fractional compliance officer is not:

- A compliance consultant producing isolated deliverables

- A project-based contractor with no decision-making authority

- A substitute for internal analysts or operational staff

- A compliance tool or RegTech platform

If you're looking for experienced, decision-driven compliance leadership that works seamlessly with your tools and systems, contact Fraxtional today to learn how we can support your company's compliance needs.

Now, understanding the role is only the first step. The harder question is when it makes sense compared to a full-time hire.

Fractional Compliance Officer vs Full-Time CCO in 2026

For most FinTech leaders, this decision is not philosophical. It is situational. Both fractional and full-time models are viable, but the question for FinTechs should be based on the current risk profile and regulatory scrutiny.

Full-Time CCOs are often necessary for larger multinational companies or firms that are heavily involved in regulated activities. However, fractional compliance officers have proven effective during rapid scale-ups or periods of transition in compliance and risk frameworks, often succeeding with mid-market FinTechs that need scalable solutions for regulatory pressures.

Below is how founders, boards, and sponsor banks tend to evaluate fractional versus full-time compliance leadership in practice.

The most common failure is not choosing between fractional and full-time leadership; it is choosing either without aligning the role to the organization’s current risk exposure.

In 2026, effective compliance leadership is defined less by employment structure and more by clear accountability, decision-making authority, and regulator-facing credibility.

Benefits and Challenges of Hiring a Fractional Compliance Officer

Hiring a fractional compliance officer offers FinTech companies a strategic solution to manage regulatory risk and oversight without incurring the full-time costs of a Chief Compliance Officer.

This model is gaining popularity for companies looking to scale quickly while maintaining strong governance and compliance practices. However, like any business decision, there are both benefits and challenges to consider.

Benefits:

- Cost Efficiency: Access senior-level expertise without the overhead of a full-time executive. Significant savings on compliance costs.

- Scalability: Flexible support that adapts as your compliance needs evolve.

- Diverse Expertise: Fractional CCOs bring insights from multiple industries, offering innovative solutions and best practices.

Challenges:

- Partial Availability: Limited time may affect immediate responsiveness during peak scrutiny periods, though this can be managed by specialized providers.

- Limited Coverage: A fractional CCO enhances strategy but doesn't replace the need for comprehensive internal or external compliance resources.

In sum, fractional compliance officers provide valuable, experienced leadership during critical growth phases.

However, to maximize their potential, it's important to align their role with your company's evolving needs and to ensure they are empowered with the necessary authority.

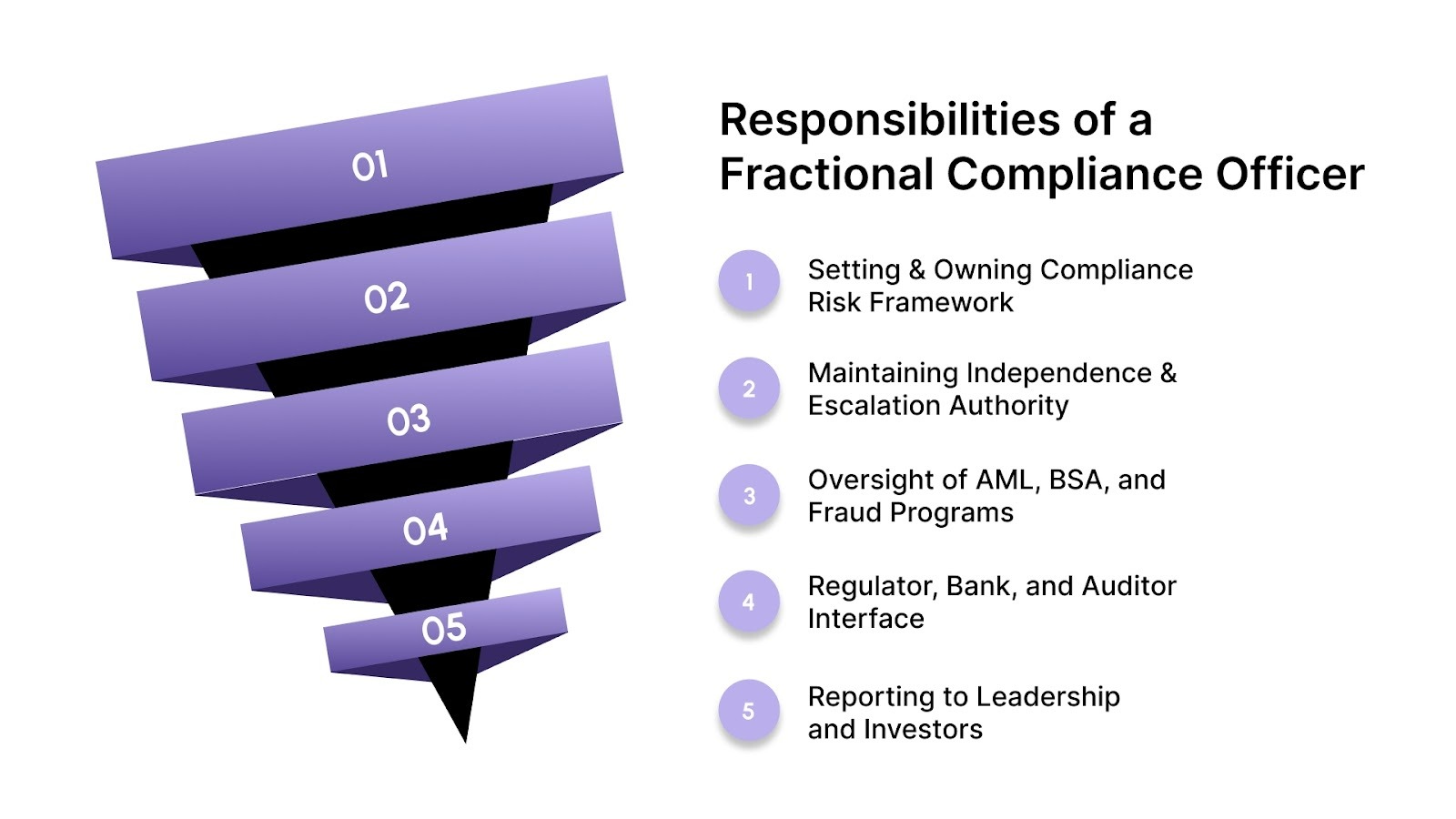

Core Responsibilities of a Fractional Compliance Officer

The value of a fractional compliance officer is not measured by how many tasks they complete. It is measured by how effectively they reduce risk through judgment, structure, and oversight.

In high-growth FinTechs, this distinction matters. Many compliance failures over the last few years occurred in companies that had policies, vendors, and staff, but lacked senior ownership of decisions.

1. Setting & Owning Compliance Risk Framework

A fractional compliance officer is responsible for defining the level of risk the company is willing to accept and where it is not. This includes:

- Interpreting regulatory expectations in the context of the business model

- Translating those expectations into precise risk tolerances

- Aligning leadership on what triggers escalation versus acceptance

Regulatory guidance increasingly emphasizes risk-based approaches rather than prescriptive rules. That shift puts pressure on leadership to make defensible decisions, not just follow checklists. A fractional officer provides that interpretive layer.

2. Maintaining Independence & Escalation Authority

One of the most cited weaknesses in regulatory exams is a lack of independence. Regulators and sponsor banks expect the compliance leader to:

- Operate independently from revenue and product incentives

- Escalate issues without friction or delay

- Communicate concerns directly to senior management or the board

A fractional compliance officer must have this authority clearly documented.

3. Oversight of AML, BSA, and Fraud Programs

While day-to-day monitoring may fall to internal teams or vendors, the fractional compliance officer owns program-level integrity. This includes:

- Reviewing and approving program design

- Ensuring alert thresholds and controls align with risk exposure

- Challenging assumptions made by tools or third parties

Mostly, regulators do not fault companies for using vendors. They fault companies for failing to understand or oversee them. Fractional leadership closes that gap by providing senior review without absorbing operational workload.

4. Regulator, Bank, and Auditor Interface

External stakeholders expect consistency, clarity, and accountability.

A fractional compliance officer typically serves as the primary point of contact for:

- Regulatory inquiries and examinations

- Sponsor bank reviews and remediation discussions

- Independent audits and SOC reporting

This continuity matters. Inconsistent messaging or fragmented ownership are common triggers for extended exams and follow-up actions. A single, experienced voice reduces that risk.

5. Reporting to Leadership and Investors

Effective compliance leadership shows up in reporting, not volume.

A fractional compliance officer is responsible for:

- Translating complex risk issues into clear executive summaries

- Highlighting trends, not just incidents

- Helping leadership understand tradeoffs before decisions are made

Investors increasingly expect structured, repeatable risk reporting rather than reactive updates. Fractional oversight can meet that expectation without building a permanent reporting infrastructure too early.

If you're ready to improve your compliance reporting and ensure your leadership team receives the insights they need, contact Fraxtional today. Let us help you implement strategic reporting that keeps your investors and stakeholders informed and confident in your compliance efforts.

A fractional compliance officer does not replace compliance analysts or investigations teams. Their role is to direct, challenge, and own outcomes, not execute every step.

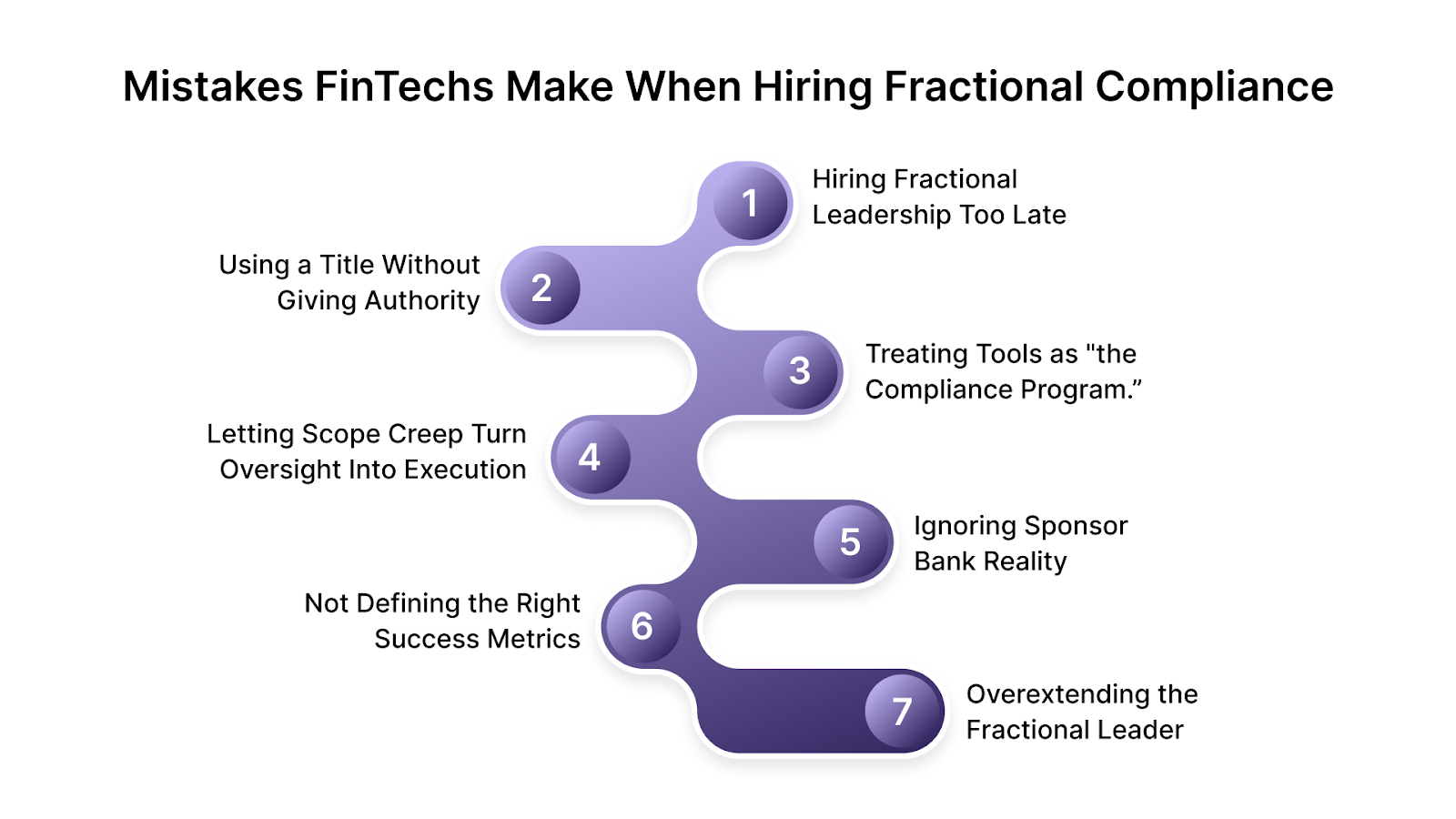

Common Mistakes FinTechs Make When Hiring Fractional Compliance

Fractional compliance works when it creates real accountability. It fails when companies treat it as a label that makes diligence easier. Here are the patterns that show up most often in sponsor bank reviews, investor diligence, and regulatory scrutiny.

1) Hiring Fractional Leadership Too Late

A common trigger is "we'll hire once the bank asks." By then, the company is usually in remediation mode, not building mode. Banks and regulators tend to apply pressure when growth outpaces controls, not when a company feels ready.

Recent sponsor-bank commentary also points out that fintech onboarding can suffer when diligence is inconsistent or treated as a one-time rather than an ongoing process.

2) Using a Title Without Giving Authority

This is the fastest way to lose credibility.

FinCEN has explicitly warned that compliance staff should be empowered with enough authority and autonomy, and that revenue interests should not compromise BSA/AML risk management.

If a fractional compliance officer can't halt a risky launch, escalate issues directly, or set minimum controls, the role becomes performative.

3) Treating Tools as "the Compliance Program.”

Many teams buy tooling first, then try to backfill governance later. Regulators don't view it that way. Tools support monitoring, but they don't replace a person who can explain decisions and their own outcomes.

This comes up in enforcement narratives where the core issue is not missing software but weak oversight, such as delayed SAR filing and KYC gaps tied to leadership failures. The NYDFS settlement with Block over Cash App compliance failures is a good reminder that growth and revenue do not offset weak controls.

4) Letting Scope Creep Turn Oversight Into Execution

Fractional leadership breaks when the officer becomes the default doer:

- writing every procedure

- running day-to-day investigations

- triaging alerts

- chasing vendors

That shift creates a predictable failure: no one is overseeing the program while everyone is busy operating it. Fractional works best when execution is owned internally (or through vendors), and the fractional leader owns governance, escalation, and program integrity.

5) Ignoring Sponsor Bank Reality

Some FinTechs optimize for initial onboarding and underestimate how quickly expectations expand after launch.

Banks are expected to maintain oversight of fintech partners through due diligence and ongoing monitoring, and sponsor-bank ecosystems add layers of complexity, including fourth-party risk.

A fractional compliance officer should be set up to manage that lifecycle, not just "get through onboarding.”

6) Not Defining the Right Success Metrics

A surprising number of engagements have no clear measures beyond "be available." Better diligence-aligned metrics look like:

- risk assessment cadence and board reporting rhythm

- evidence of escalation and closure

- audit readiness improvements

- sponsor bank issue resolution times

Investors and banks don't reward effort. They reward repeatable governance.

7) Overextending the Fractional Leader

Stakeholders will ask: "How many clients are they covering?" Even if no one asks directly, it shows up indirectly through delays, inconsistent documentation, and missed follow-ups.

By 2026, "fractional" is accepted. "Unavailable" is not.

Also Read: Regulatory Risk and Compliance Management Best Practices

The contrast becomes clear when you look at what strong fractional compliance does differently. Let's see ahead.

What "Good" Fractional Compliance Looks Like?

Today, the debate is no longer whether compliance leadership is fractional or full-time; it’s whether governance is real. Stakeholders want evidence that compliance leadership is empowered, independent, continuous, and credible with regulators.

Below is what strong fractional compliance leadership looks like in practice, and why it holds up under sponsor bank reviews and regulatory diligence.

1. Authority Is Written Down, Not Implied

A credible fractional compliance officer has formal authority that's easy to evidence: reporting lines, escalation rights, and decision ownership. That lines up with how regulators evaluate programs.

- For example, FINRA's AML program rule requires written programs and senior management approval, reinforcing the idea that compliance cannot live as an informal "advisory" function.

2. Program Is Risk-Based, Not Template-Based

Effective fractional compliance officers do not “plug in” generic policies. They own and maintain a risk assessment that actively drives program design and resourcing.

- This approach mirrors regulatory expectations under frameworks like the FFIEC BSA/AML Manual, which assess programs relative to the institution’s risk profile, not against static templates.

3. Independent Testing & Follow-Through Are Built In

Good programs don't just do audits. They close the loop. FFIEC guidance emphasizes independent testing (audit) as a core element of assessing program adequacy.

4. Sponsor Bank Readiness Is Treated as Ongoing, Not One-Time

A capable fractional compliance officer treats sponsor bank oversight as continuous, not episodic.

This includes:

- Clear contractual compliance obligations

- Evidence of ongoing monitoring

- Readiness for enhanced reviews as risk changes

Recent regulatory guidance (2024) reinforced expectations around third-party risk management, particularly for fintechs delivering deposit-related products. Fractional leadership must anticipate, not react to, these pressures.

5. Compliance Leader Can Explain Decisions Under Scrutiny

In enforcement actions, regulators rarely cite a lack of tools. The recurring issue is weak oversight and poor decision-making.

The hallmark of effective fractional compliance leadership is the ability to:

- Explain why controls were designed a certain way

- Defend risk decisions with documentation

- Demonstrate awareness of growth-driven risk

The coordinated state action against Block / Cash App ($80M penalty) underscores that regulators will escalate when BSA/AML oversight fails to keep pace with scale.

Now, making all this work consistently requires more than a model. It requires an exemplary leadership approach. This is where a partner like Fraxtional becomes essential.

How Fraxtional Makes Fractional Compliance Credible

Most FinTechs don't struggle with knowing they need compliance leadership. They struggle with making fractional leadership stand up under scrutiny.

That's where Fraxtional operates.

Fraxtional works at the point where compliance data, tooling, and documentation must turn into defensible decisions. This is the gap that regulators, sponsor banks, and investors focus on most, and where many fractional models fall short.

Rather than replacing internal teams or automation, Fraxtional's fractional compliance officers sit above them. They provide the judgment layer that regulators still expect.

Their role is to:

- Interpret what monitoring tools, audits, and reports actually mean

- Decide what matters now versus later

- Escalate issues before they become findings

- Ensure reported metrics match the company's real risk posture

The result is a compliance function that is efficient enough to keep pace with growth, and human enough to hold up when regulators, banks, or investors push deeper. That balance is what defines effective fractional compliance in 2026.

Partner with Fraxtional to build compliance leadership that scales with growth and withstands increased scrutiny.

Conclusion

Automation has made compliance measurable. It has not made it accountable. Regulators, sponsor banks, and investors still expect a named compliance leader who can explain risk decisions, defend tradeoffs, and take responsibility when growth creates pressure. Tools and dashboards support that work, but they do not replace judgment.

This is where the fractional compliance officer model has matured. Not as a shortcut, and not as a cost play, but as a way to introduce senior oversight at the moment companies need credibility more than scale.

For FinTechs experiencing rapid growth, the choice is no longer between software and leadership. It is about using both correctly. Automation keeps systems efficient. Fractional leadership keeps them trusted.

Fraxtional brings that balance into practice by pairing experienced compliance leadership with modern tooling, helping companies scale with confidence while staying defensible under scrutiny. Contact us today!

FAQs

Yes, regulators focus on authority and effectiveness, not employment status. As long as the fractional compliance officer has documented independence, escalation rights, and direct access to senior leadership, the model is generally acceptable during U.S. regulatory exams.

There is no standard hour requirement. What matters is ongoing involvement, not time logged. Regulators and banks care more about responsiveness, continuity, and decision ownership than whether the role is part-time or full-time.

In many cases, yes, provided the authority is clearly defined. Companies often authorize fractional compliance officers to approve policies, risk assessments, and audit responses, especially when the role is positioned as executive-level oversight rather than advisory support.

Sponsor banks generally accept fractional models when the compliance officer is credible, available, and empowered. Banks become concerned when the role appears symbolic, overstretched, or disconnected from day-to-day risk oversight.

Most companies transition when regulatory activity becomes continuous rather than episodic, such as frequent exams, multi-product expansion, or international exposure. Fractional leadership often serves as a bridge that reduces risk during this transition rather than delaying it.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.

Now Accepting:

BTC

ETH

USDC

USDP