Dec 8, 2025

How Substantive Testing Ensures Accurate Financial Audits

By Fraxtional LLC

Summarize the blog with AI

In highly regulated sectors such as FinTech, Cryptocurrency, Private Equity, or Real Estate, financial accuracy is crucial. A single error in reporting can result in regulatory fines or a loss of investor trust. Yet, many businesses still overlook key auditing procedures that could prevent these issues.

Substantive testing ensures financial statements are accurate and free from significant misstatements. In industries where compliance and transparency matter most, businesses must rely on strong auditing practices to avoid hidden risks that can affect decisions and relationships with investors.

In this blog, we’ll explore what substantive testing is, why it’s essential for both businesses and investors, and how it differs from control testing. We’ll also cover best practices, examples, and how technology is changing the auditing process.

TL;DR

- Substantive testing verifies the accuracy of financial statements to ensure compliance and transparency in reporting.

- It involves tests of details (examining specific transactions) and substantive analytical procedures (evaluating financial trends).

- Key regulatory standards like SAS 145 influence risk assessments and documentation practices, guiding the scope of testing.

- When errors are found, businesses must investigate, adjust financial statements, and disclose issues to stakeholders and regulators.

- Best practices include using a mix of tests, ensuring data reliability, and communicating findings promptly to maintain audit quality and investor confidence.

What Is Substantive Testing?

Substantive testing is a key auditing procedure that involves verifying the accuracy of financial statements. It focuses on gathering evidence to confirm whether the financial records are free from significant errors or misstatements. By performing substantive tests, auditors ensure that a company’s financial statements accurately reflect the business's actual financial position.

Now that we understand what substantive testing is, let’s look at why it’s crucial for ensuring accurate financial reporting.

Also Read: Effective Audit Risk Assessment for Financial Firms

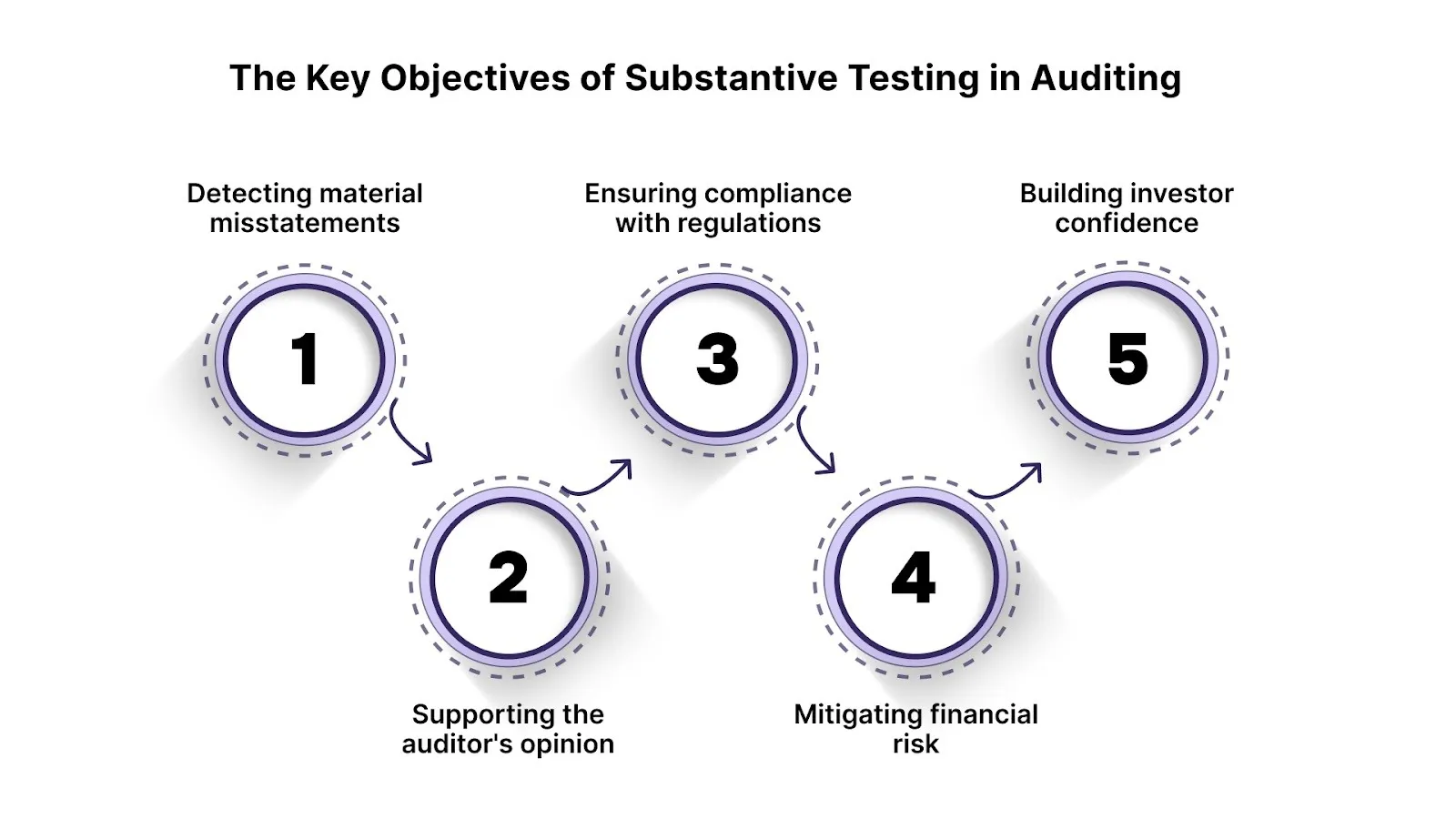

The Key Objectives of Substantive Testing in Auditing

The goal of substantive testing is to provide auditors with evidence that financial statements are free from material misstatements. It helps to verify the accuracy of financial records and ensures that the financial information presented is reliable. Effective substantive testing protects investors by reducing the risk of financial misstatements that could lead to incorrect decisions.

Key goals of substantive testing include:

- Detecting material misstatements: Ensuring the financial records are accurate and reliable by identifying any errors or omissions.

- Supporting the auditor's opinion: Substantive tests provide the necessary evidence for auditors to form an opinion on the financial statements.

- Ensuring compliance with regulations: Verifying that the company’s financial practices align with relevant laws and standards.

- Mitigating financial risk: By identifying discrepancies early, businesses can address potential issues before they become significant economic risks.

- Building investor confidence: Investors rely on accurate financial information to make informed decisions, and substantive testing helps ensure that information is trustworthy.

With these key objectives in mind, let’s explore how substantive testing differs from another vital audit procedure: control testing.

Also Read: Audit Trail Purpose and Importance in Business Compliance

Comparing Substantive and Control Testing in Audits

Substantive testing and control testing are two essential auditing procedures that serve different purposes. While both aim to ensure the accuracy of financial statements, they focus on various aspects of the audit process. Understanding the distinction is critical for both auditors and investors to evaluate the quality of an audit.

Here’s a quick comparison:

Many businesses enhance both control and substantive testing functions by scheduling an Independent Audit alongside compliance reviews, especially in sectors that require Money Transmitter Licensing or SOC 2 Compliance.

Having distinguished between substantive and control testing, it’s essential to break down the different types of substantive tests used in audits.

The Two Key Approaches to Substantive Testing

Substantive tests are primarily divided into two types: tests of details and substantive analytical procedures. Each type has a specific role in verifying the accuracy of financial data, with some being more focused on transactions and others on overall trends and relationships. Both types are essential in forming a complete and reliable audit opinion.

Let’s explore these two types:

1. Tests of Details

Tests of details involve examining specific financial transactions and balances to confirm their accuracy. Auditors will review individual records, such as invoices, receipts, and contracts, to ensure everything is in order. This method helps identify any misstatements at the transaction level.

2. Substantive Analytical Procedures

Substantive analytical procedures focus on evaluating the relationships between financial data. By comparing current data to historical trends or industry benchmarks, auditors can identify any unusual fluctuations that may indicate errors or misstatements. This type of testing provides an overview of financial accuracy rather than verifying individual transactions.

Now that we’ve covered the various types of tests, let’s take a closer look at how substantive testing is actually conducted in audits.

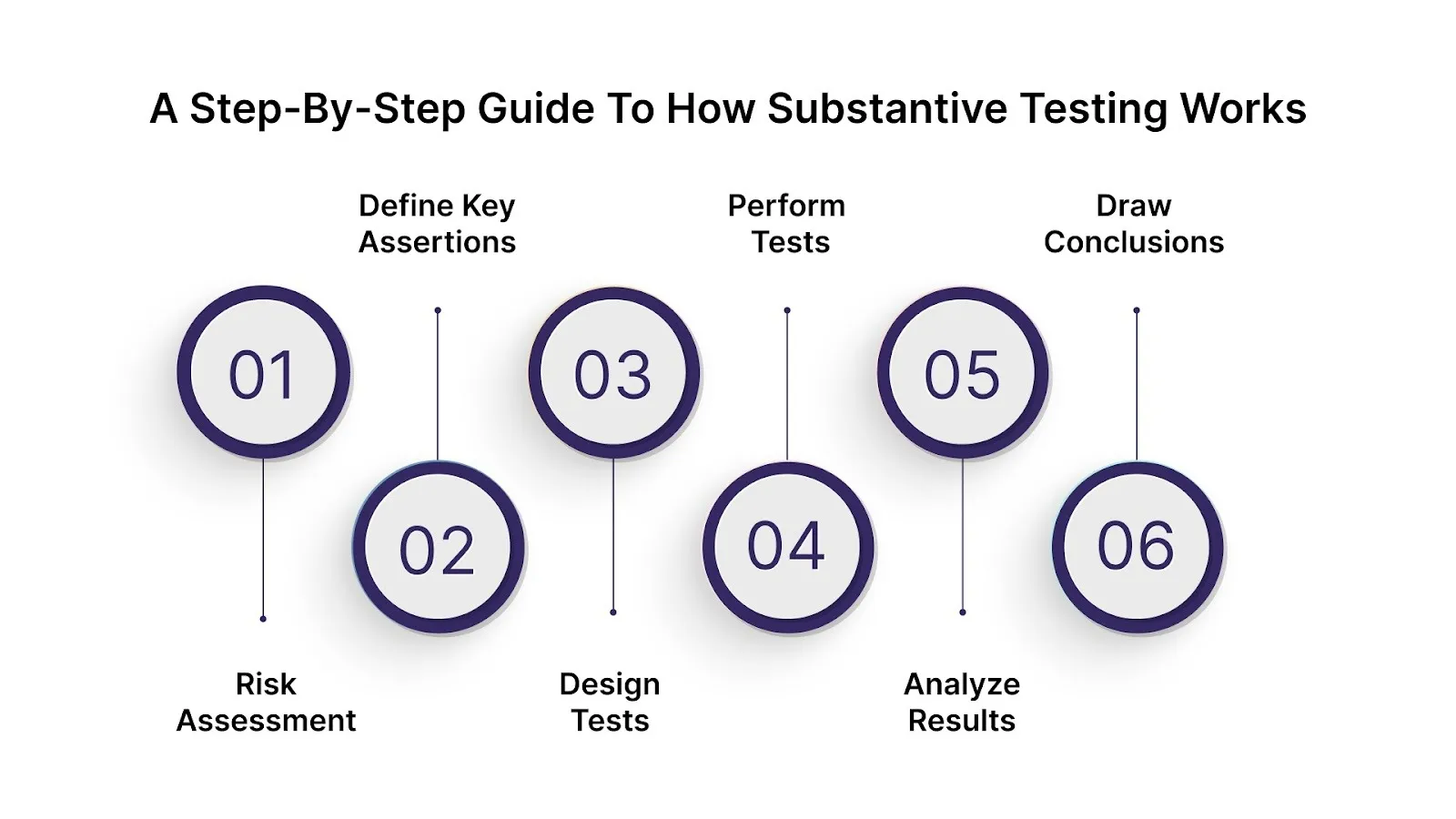

How Substantive Testing is Conducted: A Detailed Walkthrough

Substantive testing involves a series of structured steps that help auditors verify the accuracy of financial statements. The process begins with identifying risks, continues with designing specific tests, and concludes with evaluating the results to ensure that the financial data is free from significant misstatements. This approach ensures that all areas are thoroughly examined. and evaluated

Here’s the step-by-step process of how substantive testing works:

- Step 1: Risk Assessment

Auditors begin by identifying potential risks in the financial statements, based on the company’s industry, operations, and past performance.

- Step 2: Define Key Assertions

Auditors determine which financial assertions, such as accuracy or completeness, need testing to confirm the validity of the financial data.

- Step 3: Design Tests

Based on the identified risks and assertions, auditors select the appropriate type of substantive tests (details or analytical procedures).

- Step 4: Perform Tests

Auditors conduct tests by reviewing financial records, performing calculations, and verifying transactions or balances. In cases where governance gaps arise, companies may engage interim MLRO or CCO executive services to maintain compliance during audits.

- Step 5: Analyze Results

The collected evidence is examined to identify any discrepancies or misstatements in the financial data.

- Step 6: Draw Conclusions

Based on the results, auditors assess the reliability of the financial statements and determine whether they are free from material misstatement.

Once we understand how substantive testing works, it’s critical to know what happens when errors are found during the process.

Also Read: Internal Audit Checklist for Effective Financial Assessment & Control

What Happens When Substantive Testing Finds an Error?

When substantive testing identifies an error in financial statements, both businesses and investors face immediate implications. The discovery may signal deeper issues with data integrity, internal controls, or regulatory compliance. This situation demands clear action to safeguard financial credibility and stakeholder trust.

Here are the key steps and considerations when an error is found:

- Escalation to management and board: Auditors report the error in a management letter and alert the audit committee, prompting senior leadership to review the finding.

- Further audit procedures: The auditor typically performs additional tests to assess the extent of the error’s impact and determine whether it is isolated or symptomatic of wider misstatements.

- Adjustment of financial statements: If the error is material, the business must correct its financial statements, reissue reports, or disclose the issue to investors and regulators.

- Review of internal controls: The business must evaluate whether its control environment failed and take steps to strengthen controls, especially in high-risk segments.

- Investor due diligence implications: Investors reviewing a prospectus or audited report must investigate the root cause of the error, assess the auditor's independence, and evaluate any potential exposure to regulatory or reputational risk.

- Disclosure and regulatory consequences: Publicly-listed entities may need to file restatements, issue disclosures to regulators such as the SEC or FCA, and face heightened review or enforcement actions.

Businesses in regulated sectors may seek Chief AML Officer Consulting Services or Money Laundering Reporting Officer Services to strengthen oversight and ensure compliance following audit findings.

To prevent errors from affecting your financial reporting, it’s essential to implement the best practices for conducting substantive testing.

Best Practices for Substantive Testing in Financial Audits

Effective substantive testing supports reliable financial reporting and assures investors and stakeholders of the audit's quality. It requires thoughtful design, skilled execution, and precise documentation throughout the audit process.

Here are best practices tailored for investor- and business-readers:

- Apply professional skepticism throughout: Auditors should maintain a questioning mindset, critically examining evidence and recognizing signs of error or misstatement.

- Align test design with identified risks: Before auditing, the risk assessment should determine which assertions are at risk, and substantive tests should target those areas specifically.

- Use a mix of test types: Incorporate both tests of details and substantive analytical procedures to achieve more comprehensive coverage of financial statement assertions.

- Ensure data reliability and relevance: The underlying data used in tests must be accurate, complete, and appropriate for the assertions being tested.

- Document evidence and conclusions: Complete documentation of the testing steps, evidence gathered, and conclusions drawn strengthens the audit’s transparency and traceability.

- Adjust scope when findings: If substantive tests reveal unexpected errors or risk factors, auditors should expand procedures and adjust their conclusions accordingly.

- Communicate findings promptly: When businesses identify significant issues through substantive testing, investors should be informed, and the company should take action to correct or disclose them.

- Review and refine testing approaches: For industries such as FinTech, crypto, private equity, or global real estate, testing methodologies may require adaptation for transaction complexity, valuation uncertainty, or cross-border exposures.

By following these best practices, auditors can ensure the accuracy of financial statements; however, let’s examine how SAS 145 influences testing approaches.

Ensure seamless compliance management with Fraxtional’s experienced leadership. Explore our services now.

How SAS 145 Impacts Substantive Testing Procedures

The audit standard SAS 145 places greater emphasis on risk assessment and documentation ahead of performing substantive procedures. It requires auditors to identify classes of transactions, account balances, and disclosures where a misstatement is reasonably possible and potentially material.

For investors and business readers, understanding how SAS 145 impacts audit planning and evidence gathering is crucial for interpreting audit quality.

Here are the key implications of SAS 145 for substantive testing:

- Risk of misstatement drives assertion relevance: An assertion becomes “relevant” when there is both a reasonable possibility the misstatement will occur and a reasonable possibility it will be material.

- Mandatory substantive procedures for significant classes: Auditors must perform substantive procedures for every considerable class of transactions, account balances or disclosures that involve a relevant assertion.

- Stronger focus on IT controls and system risks: The standard requires auditors to identify general IT controls that address risks arising from the use of IT, then evaluate the design and implementation before determining the substantive test scope.

- Documentation burden increases: Documentation must include the auditor’s rationale for significant judgments about risks of material misstatement and how these affect the nature, timing, and extent of substantive procedures.

- Greater investor relevance: For businesses and investors, SAS 145 means that audit firms are expected to target their substantive testing where the greatest risk lies, providing a clearer signal about audit focus and potential financial reporting risks.

To meet the heightened documentation and risk assessment standards outlined in SAS 145, many businesses rely on Fraxtional CRO consulting services to effectively oversee audit preparation and compliance programs.

Conclusion

Substantive testing remains a core element of reliable auditing, giving investors and businesses confidence that financial statements are accurate and compliant. By understanding how it works, along with the impact of standards like SAS 145, investors can better assess audit quality, while businesses can strengthen their financial transparency and credibility.

At Fraxtional, we provide expert financial and compliance oversight tailored to the complex sector, including FinTech, Crypto, Private Equity, and Real Estate. Explore our services today and invest with confidence, knowing your business is supported by trusted professionals committed to clarity and regulatory assurance.

FAQs

Substantive testing is focused on verifying financial data, while internal audits assess overall organizational controls and risk management processes. The former looks for errors in financial statements, while the latter checks if internal processes are functioning effectively.

Even with strong internal controls, errors can still occur in financial reporting. Substantive testing provides an additional layer of assurance by directly verifying the accuracy of financial data, ensuring it aligns with regulatory standards.

Yes, many aspects of substantive testing, especially analytical procedures, can be automated using data analytics tools. However, human judgment is still needed to interpret complex or irregular data that automated tools may not fully address.

Substantive testing helps detect discrepancies in financial data that may indicate fraud or misstatements. By thoroughly examining financial transactions, auditors can identify unusual patterns or errors that might otherwise go unnoticed.

If an auditor fails to perform adequate substantive testing, the risk of missing material misstatements increases. This could lead to an inaccurate audit opinion, potentially causing financial and regulatory problems for the business.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.