Feb 5, 2026

7 Best Strategies for Private Equity Risk Management

By Fraxtional LLC

Summarize the blog with AI

Risk has always been part of private equity. What's changed is where value actually breaks down.

Today, a growing share of losses in PE-backed companies occurs after the deal closes, driven by operational failures, regulatory exposure, weak governance, and poor execution, rather than by pricing alone. U.S. regulators have increased scrutiny on PE-owned businesses in regulated sectors, making control, oversight, and accountability material factors in portfolio performance and exit outcomes.

This shift has elevated private equity risk management from a diligence task to a value-protection discipline.

Effective risk management now spans the full deal lifecycle, from pre-close assessment to post-acquisition oversight and exit readiness. Funds that rely solely on point-in-time diligence often discover issues too late, when remediation is costly, and use is limited.

This guide outlines the best strategies for private equity risk management in 2026. The objective is not to avoid risk. It's to control it early, monitor it continuously, and prevent it from quietly compounding inside the portfolio.

A Quick Glance

- Value loss in PE now happens post-close, not at pricing. Operational, regulatory, and governance failures drive most downside.

- Diligence alone doesn't manage risk. Risk must be owned, monitored, and revisited through exit.

- Independent risk challenge improves decisions. It offsets deal-team bias and surfaces issues early.

- Strong risk management protects exit value. Buyers reward clear governance and defensible risk controls.

- Fraxtional provides the leadership needed to ensure risk ownership and governance remain clear throughout the process.

What Private Equity Risk Management Really Means

At its core, private equity risk management is the structured process of identifying, assessing, and actively managing risks that can impair returns after capital is deployed. This includes financial risk, but more critically, operational, regulatory, governance, and execution risk inside portfolio companies.

What makes private equity different from other asset classes is timing and control. PE funds assume ownership, influence strategy, and are exposed to how well a business is governed day-to-day. That means risk doesn't end at close. It compounds or stabilizes based on post-acquisition decisions.

This is where distinctions matter:

- Private equity risk assessment focuses on identifying and sizing risk at specific points, such as pre-close or during major portfolio changes.

- Private equity risk management is ongoing. It governs how risks are monitored, escalated, and addressed over time.

- Private equity risk advisory supports both by providing an independent perspective, especially when internal teams are too close to the deal or portfolio company.

Funds that blur these lines often overinvest in diligence and underinvest in oversight. The result is the late discovery of issues that were visible earlier but not actively managed.

Effective private equity risk management treats risk as something to be owned, revisited, and governed, not documented once and forgotten.

Suggested Read: How Fractional Leadership Has Reshaped Private Equity Operations

Why Traditional Private Equity Risk Approaches Fall Short

Many PE funds still approach risk as a front-loaded exercise. Heavy diligence before close, followed by lighter-touch oversight once the deal is done. That model no longer matches where value is actually lost.

- First, point-in-time diligence doesn't age well.

Risk profiles change quickly after acquisition as companies scale, enter new markets, add vendors, or change leadership. A clean diligence report can become outdated within months if risks aren't actively revisited. - Second, deal-team bias distorts risk signals.

Teams closest to the transaction are often incentivized to move forward rather than slow down and challenge assumptions. Without an independent risk lens, early warning signs are rationalized rather than addressed. - Third, post-close ownership is often unclear.

Funds may identify risks during diligence, but fail to assign clear accountability once the portfolio company is operating. When no one owns remediation, issues linger until they surface during audits, regulatory inquiries, or exit prep. - Finally, risk is treated as a portfolio company problem, not a fund-level one.

Many funds lack a consolidated view of risk across assets. This makes it harder to spot patterns, allocate resources, or explain risk posture to investment committees and buyers.

The result is a gap between what funds think they've managed and what's actually happening inside the portfolio. That gap is where value erosion occurs.

If your fund relies heavily on pre-close diligence but lacks post-close risk ownership, Fraxtional helps deal teams identify where oversight breaks down and establish clear accountability before risk compounds inside the portfolio. Schedule a call with us!

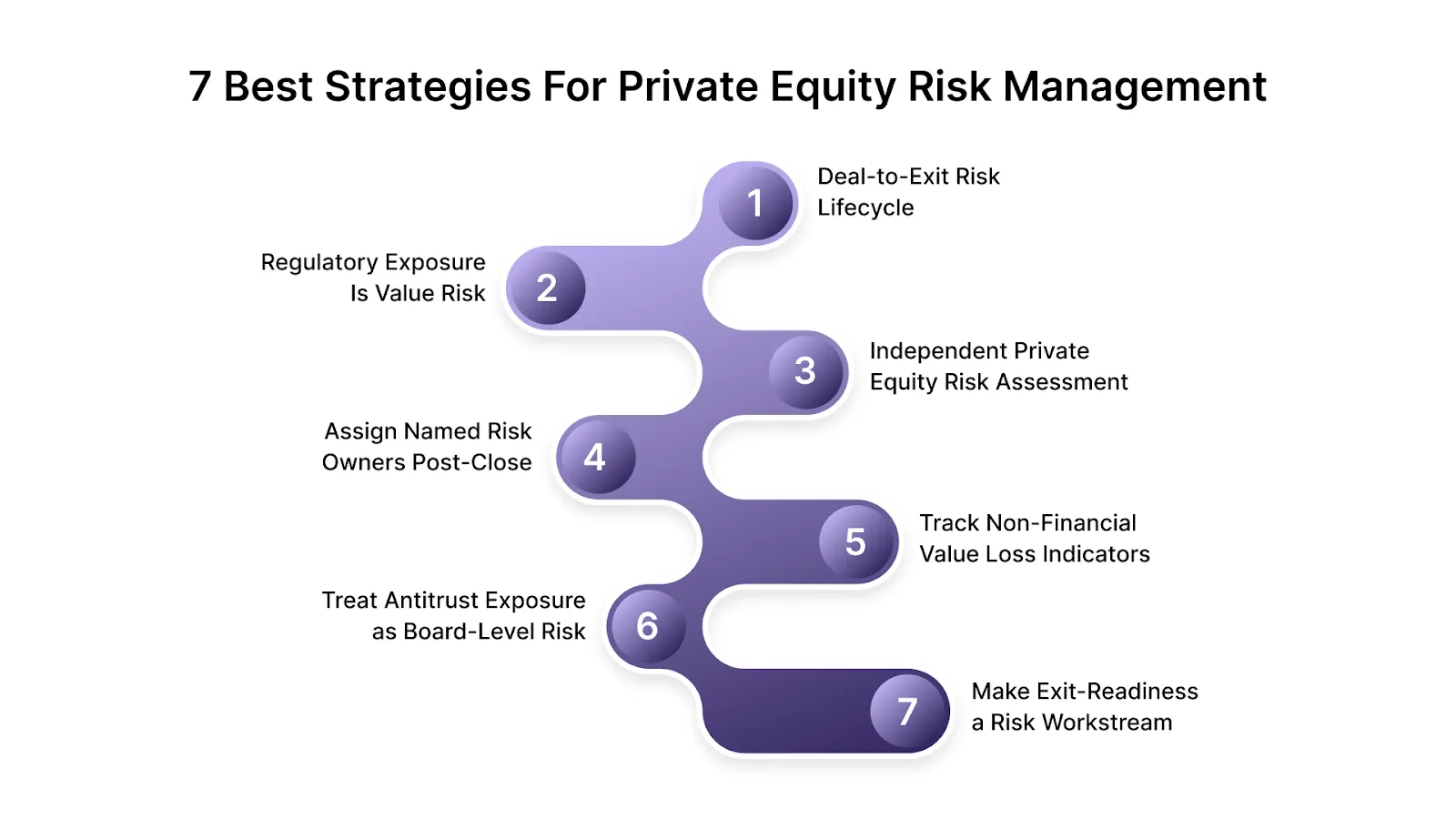

7 Best Strategies for Private Equity Risk Management

Private equity risk management is easiest to get wrong when it's treated as a one-time diligence output. The highest-performing funds run it as a repeatable system that protects value through deal, hold, and exit.

1) Build a Deal-to-Exit Risk Lifecycle, Not a Diligence Binder

A risk memo that isn't revisited becomes obsolete fast. Your risk posture changes with add-ons, new geographies, new vendors, and leadership turnover. Regulators explicitly frame risk governance as a lifecycle obligation in multiple contexts, not a point-in-time event.

What "best" looks like:

- Pre-close baseline → 90-day post-close reset → quarterly portfolio updates → pre-exit defensibility review.

2) Treat Regulatory Exposure as Value Risk, Not "Compliance Risk.”

Regulatory action can change a portfolio company's growth path overnight: restrictions, remediation mandates, monitoring, customer refunds, and brand damage. For regulated portfolios, this becomes a return driver, not a back-office issue.

A useful signal of enforcement intensity: DOJ reported $6.8B in False Claims Act settlements and judgments in FY2025 (with a large share tied to healthcare). That's not "industry noise." It's a material downside risk for any government-reimbursed or government-facing asset.

What "best" looks like:

- Map revenue to regulatory touchpoints (healthcare reimbursement, financial services compliance obligations, consumer protection exposure) and price remediation time into the value plan.

3) Run an Independent Private Equity Risk Assessment Alongside Financial/Legal Diligence

Deal teams are structurally incentivized to close. That bias doesn't make teams irresponsible; it makes independent challenge essential.

Independent assessment becomes even more important when regulators are actively probing PE-related market behavior and roll-up strategies. In May 2024, the FTC and DOJ launched a public inquiry seeking information on serial acquisitions and roll-ups across the U.S. economy.

What “best" looks like:

- An IC-ready risk assessment that calls out the top 5 "return killers," assigns owners, and ties each risk to a monitoring plan.

4) Assign Named Risk Owners Post-Close (Fund + Portfolio)

A risk without an owner becomes a future surprise. Post-close is when risk management usually breaks down: the fund assumes management owns it, and management assumes the fund owns it.

In practice, regulators look for accountability when things go wrong. When accountability is vague, the cost of remediation and the time to resolution both rise.

What "best" looks like:

- One named owner at the fund level (board/ops partner) and one at the portfolio level for each material risk area (regulatory, cyber, vendor, safety, financial controls).

5) Track "Non-Financial" Leading Indicators that Predict Value Loss

Financial KPIs are lagging indicators. Most portfolio failures are visible earlier through operational signals: spikes in complaints, audit findings, incident volume, declines in third-party performance, or unresolved control gaps.

This is especially true in healthcare and consumer-facing markets where regulators and enforcement agencies react to patterns, not quarterly results.

What “best” looks like:

- A compact portfolio risk dashboard that includes KRIs (not just KPIs) and forces escalation before a problem becomes a regulator's problem.

6) Treat Antitrust & Roll-Up Exposure as a Board-Level Risk

If your strategy involves consolidation, treat antitrust as a core diligence stream, not a legal afterthought. Regulators are openly signaling a greater focus on roll-ups and serial acquisitions, and PE sponsors have been increasingly named in that context.

The FTC announced a settlement with Welsh, Carson, Anderson & Stowe tied to allegations of a roll-up scheme (administrative resolution despite other litigation developments). Reputable reporting also indicates the FTC's continued willingness to litigate PE deals in healthcare-adjacent markets.

What “best” looks like:

- Pre-close antitrust risk memo, integration guardrails, and post-close acquisition playbook that anticipate regulator questions early.

7) Make Exit-Readiness a Risk Workstream, Not a Last-Minute Cleanup

Buyers don't just buy EBITDA. They buy defensibility: clean governance, clean controls, and a risk story that holds up under scrutiny. Weak controls can delay diligence, reduce valuation, or force escrow and indemnity concessions.

In a coverage of the Synapse collapse, Reuters reported an estimated $85 million shortfall between what depositors were owed and funds held at partner banks, affecting tens of thousands of customers with frozen or missing balances.

It is a vivid example of ecosystem risk becoming value destruction.

What “best” looks like:

- “Buyer-grade” risk narrative, documented control environment, incident history with remediation evidence, and third-party oversight that can withstand questions.

These strategies matter because they directly change outcomes, especially when scrutiny increases or exits approach.

How These Top Strategies Protect Returns

Private equity risk management isn't about creating more processes. Done right, it protects returns by reducing the specific events that derail value creation: regulatory shocks, operational breakdowns, delayed exits, and surprise remediation.

Here's what the payoff looks like in practice.

1) Fewer post-close surprises that force expensive remediation

The biggest value leaks aren't usually "unknown unknowns." They're known risks that weren't assigned, tracked, or escalated until they became urgent. A lifecycle model (pre-close → post-close reset → ongoing monitoring) catches drift early, when fixes are cheaper and less disruptive.

2) Faster decision-making under scrutiny

Private markets are getting more visible to regulators, and that changes the cost of being unprepared. The SEC has described the private investment sector as roughly $24 trillion, and enhanced risk reporting has been part of the regulatory push to monitor systemic exposure.

Funds that already operate a tight risk cadence can respond more quickly when questions arrive from LPs, lenders, regulators, or buyers.

3) Stronger LP confidence during diligence and re-ups

LP expectations have become more structured. The ILPA DDQ explicitly asks managers to describe their risk management approach and identify which risks are monitored and measured, including a distinction between investment risk and enterprise risk.

Funds that can show repeatable risk ownership, monitoring, and escalation don't just "answer the DDQ." They build credibility that carries into fundraising and co-invest conversations.

4) Cleaner exits and fewer valuation haircuts

Buyers don't just diligence performance. They diligence whether the company is governable: controls, vendor oversight, incident history, and whether the risk story is defensible. When those pieces are already documented and owned, exits move faster, with fewer last-minute fixes, fewer surprise findings, and fewer deal protections demanded.

Funds that operationalize risk early experience fewer disruptions at exit. Fraxtional helps PE firms translate risk oversight into buyer-ready narratives that withstand diligence and protect valuation. Contact us today!

Next, let's translate these strategies into execution and learn how to implement them.

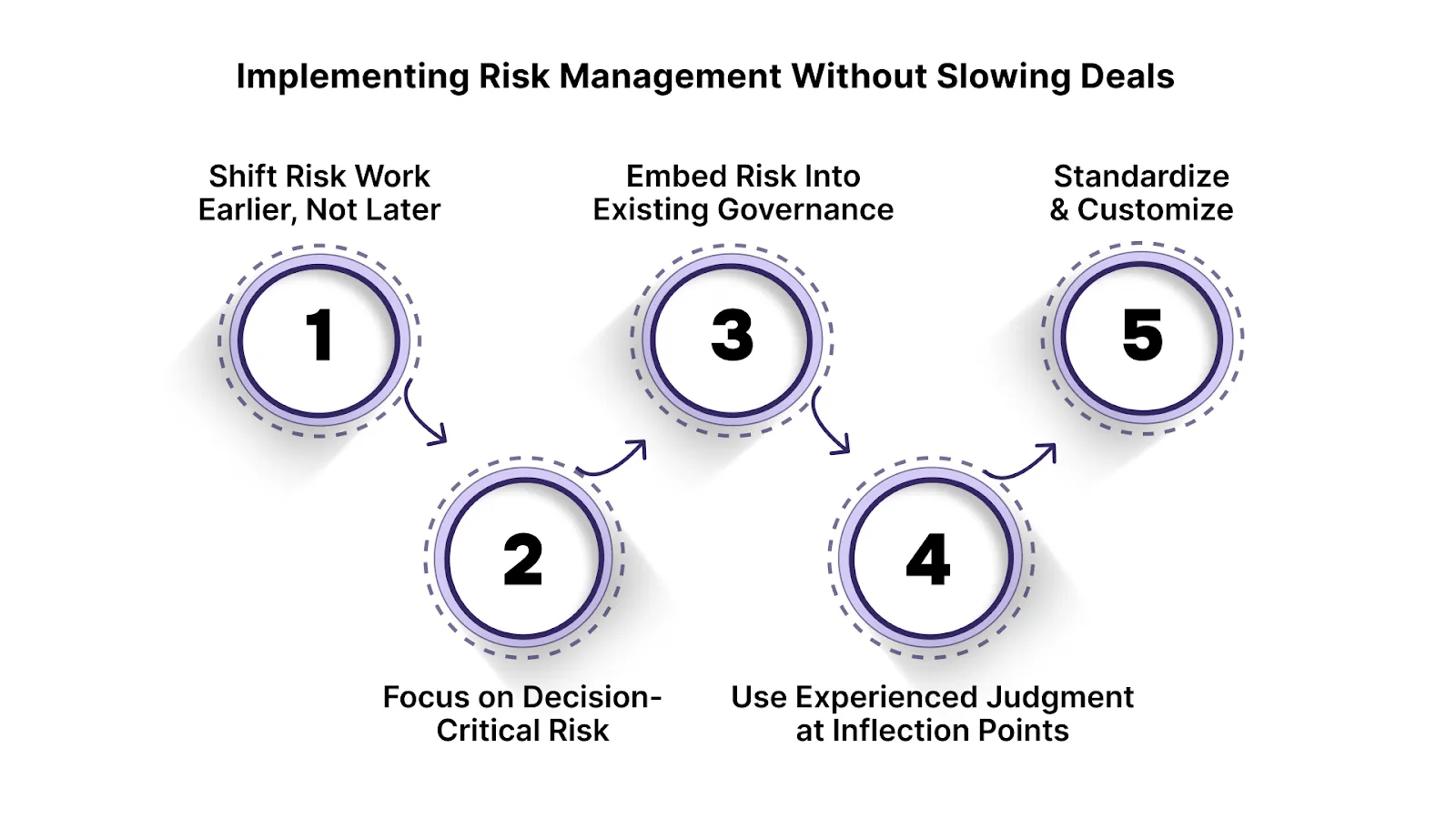

Implementing Risk Management Without Slowing Deals

The most common objection to stronger risk management in private equity is the perceived speed constraints. Deal teams worry that additional reviews, assessments, or oversight will delay closes or distract management post-close. In practice, the opposite is often true.

When risk management is structured correctly, it reduces friction instead of adding it.

1. Shift Risk Work Earlier, Not Later

Delays usually happen when risks surface late. Regulatory, operational, or governance issues discovered post-close are harder to fix and almost always slow growth plans. Early identification and planning are more effective than reactive remediation.

Funds that integrate targeted risk assessment alongside diligence avoid reopening issues after signing, when leverage is lower, and timelines are tighter.

2. Focus on Decision-Critical Risk

Not every risk needs a deep dive. What slows deals is unfocused risk work. High-performing funds focus on risks that can materially affect valuation, scalability, or exit timing, including regulatory exposure and control gaps in core operations.

This approach aligns with how investment committees make decisions: prioritizing downside scenarios that meaningfully change outcomes.

3. Embed Risk Into Existing Governance

Risk management slows deals when it runs as a separate track. It accelerates decisions when it's embedded into board materials, operating reviews, and integration plans.

Instead of adding meetings, funds that integrate risk into existing cadences reduce rework and avoid last-minute escalations. This structure also reflects regulator expectations around integrated governance and oversight.

4. Use Experienced Judgment at Inflection Points

Speed breaks down when teams face unfamiliar risk. This is where targeted private equity risk advisory adds value. Independent, senior-level input during acquisitions, add-ons, or geographic expansion helps teams make better-informed decisions.

Regulators and LPs increasingly expect funds to demonstrate that complex risks are reviewed by individuals with appropriate experience and authority, not just documented.

5. Standardize & Customize

Funds that develop repeatable risk templates, reporting formats, and escalation thresholds move faster from deal to deal. Standardization reduces debate over process, while customization focuses attention on asset-specific risks.

The result is a risk function that supports execution instead of competing with it.

When implemented this way, private equity risk management becomes an enabler. Deals move faster because fewer issues resurface unexpectedly, and portfolio teams spend less time reacting and more time executing.

How Fraxtional Supports Private Equity Risk Management

Private equity risk management breaks down when insight doesn't translate into action. This is where Fraxtional operates.

Fraxtional works at the point where risk data, diligence findings, and monitoring outputs need to be translated into clear decisions for deal teams, operating partners, and investment committees.

Rather than replacing internal teams or tools, Fraxtional provides fractional risk leadership that adds independent judgment and accountability across the investment lifecycle.

Every engagement starts with clarity:

- Mapping material risk across portfolio companies, vendors, jurisdictions, and regulatory regimes

- Aligning risk assessments and monitoring tools with fund-level governance and IC expectations

- Embedding senior ownership into post-close oversight, board cadence, and escalation routines

- Translating audits, reviews, and incidents into defensible narratives for LPs, lenders, regulators, and buyers

The result is a risk model that scales with the portfolio. Automated where efficiency matters, but led by experienced judgment where credibility and accountability matter most.

Partner with Fraxtional to build private equity risk management systems that enable faster decisions and withstand scrutiny from diligence, regulators, and buyers.

Conclusion

Risk tools can surface issues. They don't decide what to do next.

In private equity, risk management ultimately comes down to judgment. Dashboards, models, and reports help quantify exposure, but they don't assign ownership, weigh trade-offs, or defend decisions when scrutiny increases. Investment committees, LPs, regulators, and buyers still look for accountable leadership behind every risk call.

That's why the future of private equity risk management isn't automated or manual. It's both.

Systems help monitor risk at scale. Leadership determines whether risk is understood, governed, and acted on in a timely manner. Funds that recognize this difference are better positioned to protect value post-close and exit on stronger terms.

Fraxtional brings that balance to private equity by pairing structured risk oversight with senior judgment, turning risk management from a reactive function into a strategic advantage across the deal lifecycle. Reach out to us today!

FAQs

By focusing on decision-critical risks rather than exhaustive analysis. Funds prioritize risks that could affect valuation, delay growth, or affect exit timing, and defer lower-impact issues to post-close oversight.

Early signals include repeated audit findings, rising customer complaints, vendor instability, delayed remediation, and frequent control overrides. These usually appear well before financial performance declines.

Funds benefit from a portfolio-level risk view that aggregates common exposures across assets. This helps identify patterns, allocate operating resources, and brief investment committees more effectively.

Risk becomes board-level when it affects regulatory exposure, capital allocation, reputation, or exit readiness. At that point, oversight must move beyond management reporting to active board engagement.

Yes. Buyers increasingly value clean governance, documented controls, and defensible risk narratives. Strong risk management reduces friction in diligence and limits price adjustments or deal protections.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.

Now Accepting:

BTC

ETH

USDC

USDP