Feb 5, 2026

What Is Relationship Banking? A 2026 Guide for FinTech & Sponsor Banks

By Fraxtional LLC

Summarize the blog with AI

Relationship banking used to mean having a banker who understood your business. Today, for U.S. FinTechs and sponsor banks, it means something far more concrete.

Relationship banking is no longer about access or familiarity. It is about trust demonstrated through governance, transparency, and operational discipline. For FinTechs, strong banking relationships directly affect sponsor bank approvals, program stability, and long-term scalability. Sponsor banks determine whether partnerships can withstand regulatory exams without introducing unacceptable risk.

This guide explains what relationship banking really means and its benefits in a modern FinTech–sponsor bank context. You'll learn how strong banking relationships now function as a strategic advantage rather than a baseline requirement.

Key Takeaways

- Relationship banking is now defined by control, not connection. Sponsor banks care about governance, evidence, and oversight, not familiarity.

- Bank partnerships depend on how well risk can be supervised. Growth matters less than clarity, accountability, and continuous monitoring.

- Strong banking relationships reduce friction and disruption. They speed approvals, stabilize programs, and improve long-term economics.

- Most relationship failures come from avoidable oversight gaps. Late escalation, weak change management, and poor vendor visibility erode trust.

- Fractional leadership has become a requirement, not a fallback. Accountable decision-makers are essential to sustaining trust beyond automation.

What Actually is Relationship Banking

At its core, relationship banking is a long-term banking relationship built on repeated interactions, shared information, and mutual reliance, rather than one-off transactions. Traditionally, this model allowed banks to make better credit and risk decisions by understanding a customer's business over time.

In a FinTech–sponsor bank context, the meaning is narrower and more operational.

Here, a banking relationship is not defined by tenure or personal rapport. It is the ongoing evaluation of how well risk is identified, managed, and escalated. For sponsor banks, relationship banking is the mechanism that allows partnerships to scale while remaining exam-ready.

In practical terms, relationship banking today sits at the intersection of:

- Governance and decision-making authority

- Compliance program design and execution

- Third-party and fourth-party risk management

- Reporting cadence and issue escalation

When these elements are weak, banking relationships become fragile. When they are mature, sponsor banks gain confidence, and FinTechs gain durability.

Suggested Read: Key Activities to Enhance Bank Compliance Management

Let's understand why building strong bank relationships has become materially harder over the past few years.

Why Bank Relationships Became Harder After BaaS Scrutiny

Bank–FinTech relationships did not become more demanding by accident. They tightened in response to regulatory pressure and real supervisory findings.

Over the last few years, U.S. banking regulators have made it explicit that sponsor banks remain fully responsible for the activities of their FinTech partners. This includes not only the FinTech itself, but also its vendors, processors, and other downstream third parties.

Guidance from federal regulators has consistently emphasized third-party risk management, ongoing monitoring, and clear accountability within banking-as-a-service programs.

As scrutiny increased, sponsor banks raised their standards. What once passed as "good enough" documentation or informal oversight is no longer sufficient. Banks now expect:

- Clear ownership of compliance and risk decisions

- Documented control frameworks tied directly to products and services

- Ongoing monitoring, testing, and reporting, not point-in-time reviews

- Early disclosure of issues, changes, and incidents

For FinTechs, this shift has made bank relationships harder to establish and easier to lose. Initial approvals take longer. Annual reviews are more detailed. Small gaps that once went unnoticed can now trigger heightened scrutiny or remediation demands.

Importantly, this is not a temporary tightening. The direction of travel is clear: relationship banking now operates under continuous supervision, not episodic trust. Sponsor banks are expected to prove control at all times, and FinTech partners are judged by how well they enable that control.

Let's see what this shift delivers in return and the concrete benefits strong banking relationships create for both FinTechs and sponsor banks.

Key Benefits of Relationship Banking for FinTechs & Sponsor Banks

When relationship banking is treated as an operating model rather than a slogan, the benefits are tangible and measurable. For both FinTechs and sponsor banks, strong banking relationships reduce friction, lower risk, and create long-term stability.

1. Faster sponsor bank approvals and renewals

FinTechs with clear governance, documented controls, and consistent reporting move through onboarding and annual reviews more efficiently. Sponsor banks can assess risk more quickly when information is structured, current, and repeatable, reducing back-and-forth and approval delays.

2. Lower regulatory and operational risk

Strong banking relationships surface issues earlier. Regular reporting, defined escalation paths, and ongoing monitoring reduce the likelihood of surprises during regulatory exams. This directly lowers the risk of enforcement actions, program pauses, or remediation orders that disrupt operations.

3. Greater program stability under regulatory scrutiny

Banking relationships tend to break during stress events, not during growth periods. FinTechs that operate with relationship banking discipline are better positioned to withstand exams, audits, and supervisory inquiries without sudden changes to their sponsor bank arrangements.

4. Improved long-term economics

As sponsor banks gain confidence in a FinTech's risk posture, the oversight burden decreases. Over time, this can translate into better commercial terms, fewer restrictions, and greater flexibility to expand into new products or geographies. Trust compounds when risk remains predictable.

5. Stronger alignment between business growth and compliance

Relationship banking aligns growth with control. Instead of compliance lagging behind product expansion, governance and risk management scale alongside the business. This reduces internal strain and supports sustainable growth.

Taken together, these benefits explain why relationship banking has become a competitive advantage.

Fraxtional works with FinTech leadership teams to turn relationship banking from a concept into an operating model. We help sponsor banks see clear ownership, consistent reporting, and defensible oversight from day one. Contact us today!

Now, let's shift perspective and examine relationship banking from the sponsor bank's perspective.

What Relationship Banking Looks Like From the Sponsor Bank Side

Sponsor banks evaluate banking relationships through a control lens. The core question is simple: "Can this FinTech operate in a way that ensures the bank meets its regulatory obligations at all times?"

Everything else flows from that assessment. In practice, strong banking relationships share a few consistent characteristics.

- First, ownership is clear. Sponsor banks expect defined accountability for compliance, risk, and issue management. When responsibilities are fragmented or unclear, relationships deteriorate quickly, especially during exams or incidents.

- Second, governance is active, not symbolic. Banks look for evidence that decisions around products, changes, vendors, and expansion follow a structured approval process. Relationship banking breaks down when FinTechs treat governance as documentation rather than a decision-making discipline.

- Third, oversight is continuous. One-time due diligence is no longer enough. Sponsor banks expect regular reporting, test results, and risk indicators that demonstrate how controls perform over time. Consistency matters more than perfection.

- Fourth, issues surface early. Strong bank relationships are built on early disclosure, not surprise remediation. Sponsor banks place significant weight on how quickly and transparently a FinTech escalates problems, incidents, or regulatory concerns.

- Finally, third-party risk is controlled end-to-end. Banks increasingly assess not just FinTech but also its processors, vendors, and service providers. A weak fourth-party risk posture is often a deciding factor in relationship stress or termination.

From the sponsor bank's perspective, relationship banking is ultimately a risk-management tool. It determines whether a partnership can scale, survive regulatory scrutiny, and remain commercially viable over time.

Next, let's move from perspective to execution and outline the operating system that supports strong banking relationships in 2026.

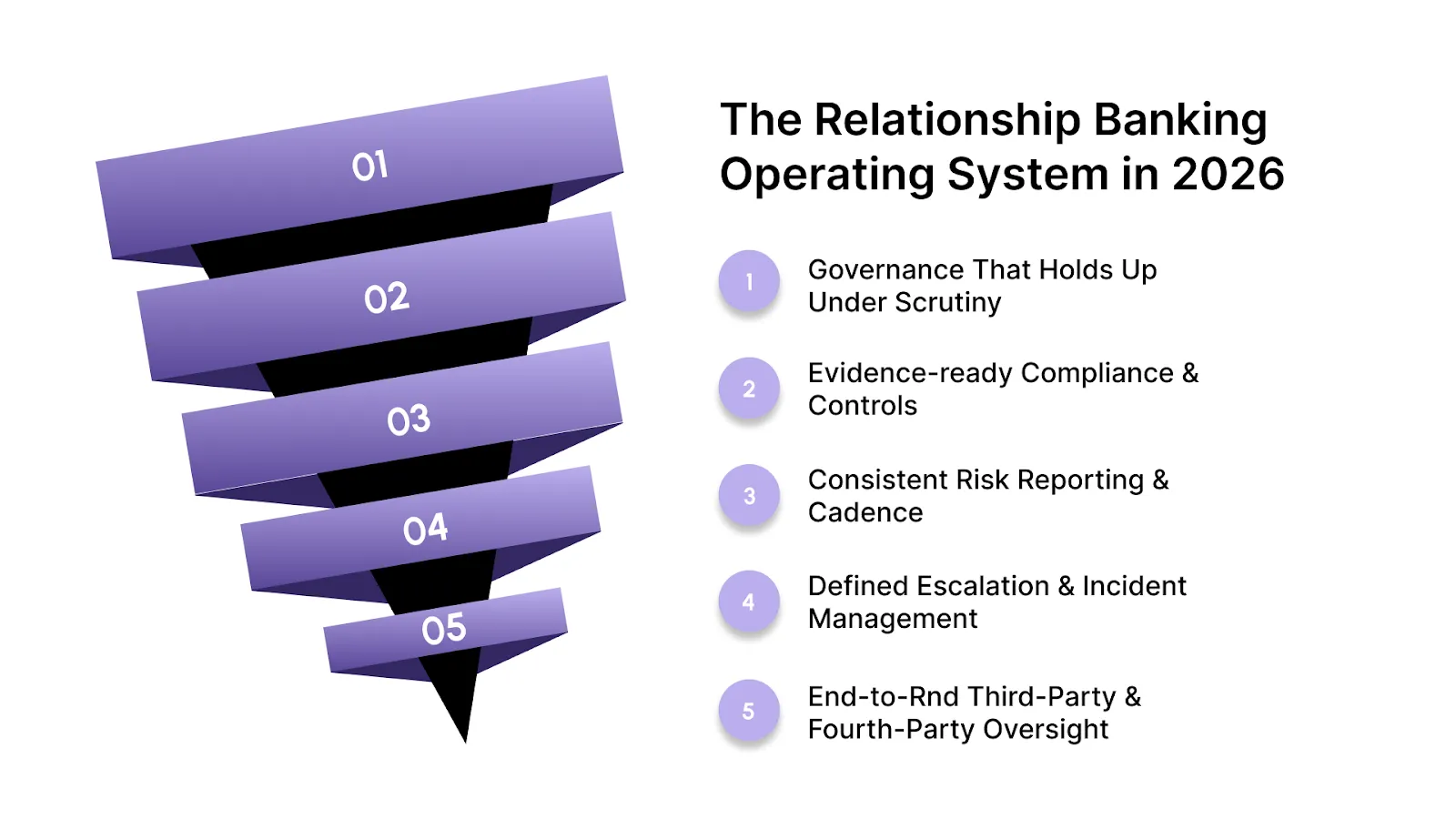

The Relationship Banking Operating System in 2026

By 2026, relationship banking is no longer informal or personality-driven. For FinTechs and sponsor banks, it operates as a defined system built to withstand regulatory review, growth, and inevitable stress events.

Sponsor banks now evaluate relationships based on whether a FinTech has an operating model that can be supervised on an ongoing basis, not just approved once.

Strong banking relationships consistently rest on five core components.

1. Governance That Holds Up Under Scrutiny

Effective relationship banking starts with decision-making authority.

- Sponsor banks expect documented governance structures that define who approves products, signs off on changes, accepts risk, and owns remediation.

- Informal approval processes or founder-led decisions without risk input are frequent sources of regulatory concern.

A durable banking relationship requires governance that is active, repeatable, and traceable.

2. Evidence-ready Compliance & Controls

Relationship banking depends on proof.

- Policies, procedures, and controls must map directly to products and risk exposure, not exist as generic templates.

- Sponsor banks increasingly expect FinTechs to produce control narratives, testing results, and issue tracking that can be reviewed on demand.

This expectation reflects a broader regulatory trend. FinTechs that cannot show how controls operate in practice often struggle to maintain bank confidence over time.

3. Consistent Risk Reporting & Cadence

Healthy bank relationships rely on rhythm.

- Monthly or quarterly risk reporting, key risk indicators, and issue updates allow sponsor banks to identify trends before they become problems.

- Irregular or ad hoc reporting is often interpreted as a lack of control, even when issues are minor.

From a sponsor bank's perspective, predictable reporting reduces supervisory risk. It also limits last-minute information requests during exams, which is a common source of relationship strain.

4. Defined Escalation & Incident Management

No program operates without issues.

- What differentiates strong banking relationships is how quickly and transparently those issues are escalated.

- Sponsor banks expect predefined thresholds for incidents, regulatory inquiries, control failures, and customer impact events.

Delayed disclosure, not the incident itself, is what escalates supervisory response.

5. End-to-Rnd Third-Party & Fourth-Party Oversight

Now, sponsor banks assess the entire ecosystem surrounding a FinTech.

- This includes processors, KYC vendors, cloud providers, and other critical service partners. Regulators have made it clear that banks remain responsible for these relationships, even when services are outsourced.

- As a result, FinTechs with mature vendor due diligence, contract controls, and monitoring programs are significantly easier for banks to supervise. Weak third-party oversight can be one of the fastest ways to undermine a banking relationship.

Together, these elements form the operating system behind modern relationship banking.

If you recognize the operating model but don't have senior ownership to run it, Fraxtional provides fractional risk and compliance leaders who embed directly into governance, reporting, and escalation routines, not just documentation. Schedule a call with us!

Now, let's turn this operating model into action, outlining how FinTechs can begin building a strong banking relationship within a defined, practical timeline.

How to Build a Strong Banking Relationship in 90 Days

If you're trying to strengthen a bank relationship in 2026, the fastest way to build credibility is to align your operating model to what U.S. regulators already expect sponsor banks to do with third parties: plan, diligence, contract, monitor, and exit in a risk-based way.

A practical 90-day plan should do one thing: make your risk posture legible, your controls provable, and your oversight continuous.

Days 1–30: Make Risk Legible

This month focuses on creating a clear view of "what is happening" and "who owns it.”

Deliverables that sponsor banks can actually use:

- A product + funds-flow map (what happens, where, and with whom)

- A third-party/fourth-party inventory (processors, KYC/KYB, fraud, cloud, dispute ops)

- Clear decision ownership (who approves product changes, vendors, and risk acceptance)

This directly supports the "planning" and "risk assessment" expectations laid out in interagency third-party risk guidance.

Days 31–60: Build the Evidence Pack

Sponsor banks don't just need policies. They need evidence that controls exist and work.

Evidence that tends to unblock reviews:

- Policies/procedures mapped to your actual product (not generic templates)

- A control narrative (how monitoring happens, how alerts are handled, how issues are logged)

- Vendor due diligence files + contract highlights (SLAs, audit rights, incident notification)

Regulators explicitly call out due diligence, contract structuring, and ongoing monitoring as core elements of third-party oversight.

Days 61–90: Operationalize the Cadence

This is where a "banking relationship" becomes durable: predictable reporting, clean escalation, and fewer surprises.

What "good" looks like

- Monthly risk reporting with clear KRIs (fraud, disputes, AML alerts, vendor performance)

- A defined escalation playbook (what triggers escalation, timelines, named owners)

- A change-management routine (new product/geo/vendor changes routed through approval gates)

This maps to the interagency focus on ongoing monitoring throughout the life cycle of a third-party relationship.

So here's the final crux:

In 90 days, you're not trying to eliminate risk. You're trying to demonstrate that risk is governed, monitored, and communicated in a way that keeps a sponsor bank exam-ready while continuing to grow the partnership.

Common Mistakes That Break Bank Relationships

Most bank relationships don't fail because a FinTech is "bad." They fail because oversight becomes unprovable or surprises become too frequent.

U.S. regulators have been consistent on what constitutes good: third-party relationships should be managed across the full life cycle (planning, due diligence, contract structure, ongoing monitoring, and exit). When a FinTech partner makes that life cycle harder to execute, the relationship weakens fast.

Here are the failure patterns that recur:

1) Treating relationship banking like a warm connection, not an operating model

If the "relationship" depends on a few individuals rather than repeatable governance and reporting, it breaks the moment there's turnover, an exam, or an incident. A bank's oversight cannot be episodic. It has to be continuous and risk-based.

2) Underestimating third-party and fourth-party exposure

Sponsor banks are increasingly focused on nested vendor relationships and downstream dependencies. When a FinTech can't clearly explain who touches funds, data, onboarding, fraud controls, or dispute operations, the bank's ability to supervise collapses.

3) Weak change management (the “we already launched it” problem)

One of the fastest ways to damage a banking relationship is shipping product changes, new geographies, or new vendors without a documented approval path. Sponsor banks need to demonstrate control over what they sponsor.

If changes are made after the fact, trust erodes, and reviews become stricter.

4) Late escalation and "surprise risk.”

Incidents happen. The relationship-breaking move is delayed disclosure or unclear escalation thresholds. That's when a manageable issue becomes a supervisory problem.

In coverage tied to the Synapse collapse, Reuters reported an estimated $85 million shortfall between what depositors were owed and funds held at partner banks, affecting tens of thousands of customers with frozen or missing balances.

Sponsor banks interpret this kind of event as a worst-case proof of why early visibility matters.

5) Operating without "exam-ready" evidence

Policies alone don't protect a bank relationship.

Sponsor banks need artifacts they can produce during exams, including monitoring results, issue logs, vendor files, testing schedules, and evidence of consistent oversight. Governance, documentation, and monitoring should scale with risk and criticality.

6) Ignoring explicit supervisory signals

Finally, some relationships break because partners treat enforcement actions as "someone else's story." They're not.

For example, in June 2024, the Federal Reserve issued an enforcement action against Evolve Bank & Trust that, among other things, restricted new fintech partner activity without supervisory approval. This is a clear signal that weak oversight can directly constrain program growth.

That kind of constraint impacts every FinTech connected to the program.

These are avoidable mistakes, but only if relationship banking is treated like a system: clear governance, continuous monitoring, disciplined change management, and early escalation.

How Fraxtional Strengthens Relationship Banking on Both Sides

Relationship banking breaks down when expectations aren't translated into day-to-day decisions. This is where Fraxtional operates.

Fraxtional sits at the intersection of FinTech execution and sponsor bank expectations, providing fractional risk and compliance leadership that turns oversight requirements into an operational, defensible, and sustainable approach.

In the context of relationship banking, that means helping FinTechs and sponsor banks answer the questions regulators actually ask: Who owns risk? How is it monitored? How do you know controls work? What happens when something goes wrong?

Every engagement starts with clarity:

- Mapping risk exposure across products, vendors, and jurisdictions

- Aligning compliance frameworks with sponsor bank and regulatory expectations

- Embedding leadership oversight into governance and change-management routines

- Translating monitoring, audits, and reviews into clear narratives for boards and bank partners

The result is not just better documentation, but stronger banking relationships. Fraxtional's role is simple but critical: ensure that relationship banking is supported by leadership, not left to assumptions.

Partner with Fraxtional to build compliance and risk systems that scale with your growth and hold up when sponsor banks and regulators look closest.

Conclusion

Automation can prove compliance. It does not sustain trust.

Tools and platforms have made governance measurable and more efficient, but they haven't changed what regulators, sponsor banks, and investors ultimately look for: clear ownership and defensible judgment.

That's why relationship banking still hinges on leadership.

In a high-scrutiny environment, software keeps controls running, but people keep relationships intact. Sponsor banks don't just assess dashboards or reports. They assess whether a FinTech's risk posture is understood, governed, and actively managed by accountable leaders.

For FinTechs that want durable bank relationships, fractional risk and compliance leadership is no longer a stopgap. It's the assurance layer that makes growth credible, oversight sustainable, and trust repeatable.

Fraxtional brings that assurance to relationship banking by pairing operational discipline with senior judgment, helping FinTechs and sponsor banks move faster without sacrificing control. Reach out to us today!

FAQs

Yes, but it increases complexity. Each sponsor bank will expect independent oversight, reporting, and approval workflows. Without strong governance, multi-bank setups often slow growth rather than accelerate it.

The most common triggers are delayed disclosure of issues, weak third-party oversight, and undocumented product changes. Exits usually happen after trust erosion, not a single compliance failure.

Examiners look at whether oversight is continuous, documented, and enforced. Banks are assessed on their ability to monitor FinTech partners, escalate issues, and prove control across vendors and products.

In regulated banking ecosystems, yes. Favorable pricing and fast launches mean little if a sponsor bank restricts activity or pauses programs due to oversight concerns.

Generic policies, outdated risk assessments, and missing vendor files are common red flags. Sponsor banks expect documentation that reflects how the business actually operates today.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.

Now Accepting:

BTC

ETH

USDC

USDP