Jan 27, 2026

How to Use a Gap Assessment Template Reviewers Actually Expect

By Fraxtional LLC

Summarize the blog with AI

Information security and compliance controls are rarely challenged during routine operations. Scrutiny begins during audits, sponsor bank reviews, and regulatory examinations, when reviewers test whether controls are documented, owned, enforced, and supported by evidence rather than stated intent.

In regulated financial businesses, a gap assessment template becomes the mechanism that exposes whether governance aligns with real execution. Reviewers examine how controls operate across AML, information security, vendor oversight, and risk management, looking for traceable ownership, reproducible evidence, and defensible escalation paths. When documented controls diverge from operational reality, reviews slow, questions multiply, and remediation expands under pressure.

This guide explains what a gap assessment template is in a compliance and risk context, how banks and regulators evaluate it, and what must be included for it to withstand audit, sponsor bank, and regulatory scrutiny.

Key Takeaways

- A gap assessment template must validate control operation, ownership, evidence, and escalation under audit, sponsor bank, and regulatory testing conditions.

- Effective gap assessments map regulatory text directly to control design, execution testing, evidence validation, and governance accountability.

- A practical gap assessment template documents required artifacts, retention standards, and sampling readiness to support retrospective audits and lookbacks.

- Gaps must be prioritized based on statutory exposure, sponsor bank tolerance, and exam risk rather than internal impact assumptions.

- Closing gaps depends on evidence-first remediation, assigning owners with enforcement power, and timelines aligned to regulatory urgency.

What Is a Gap Assessment in Compliance and Risk Management?

A gap assessment in compliance and risk management is a structured evaluation of how an organization’s existing controls, governance, and documentation compare against explicit regulatory, supervisory, and sponsor bank expectations.

It focuses on control design, operating evidence, ownership clarity, and regulatory defensibility rather than theoretical alignment or high-level maturity scoring.

Why Gap Assessments Matter for Regulated Financial Businesses

Regulated financial institutions rely on gap assessments to translate regulatory obligations into provable execution, particularly when external reviewers evaluate control effectiveness under real operating conditions rather than stated policy intent.

- Regulatory Control Coverage: Identifies missing or partially implemented controls across BSA, AML, OFAC, licensing, and information security requirements tied to specific statutes and guidance.

- Sponsor Bank Due Diligence Readiness: Surfaces gaps that commonly trigger sponsor bank rejections, including unclear control ownership, weak escalation paths, and undocumented operational practices.

- Audit and Exam Defensibility: Validates whether controls produce reviewable, time-bound evidence that withstands regulator testing, independent audits, and lookback examinations.

- Risk Rating and Prioritization Accuracy: Aligns remediation priorities with regulatory impact and inherent risk severity, not internal perception or generic heat maps.

- Governance and Accountability Validation: Tests whether compliance roles, committee oversight, and management reporting operate as documented, with traceable decision authority.

Gap Assessment Framework for Regulated Financial Businesses

A compliance gap assessment is executed through a defined framework that aligns regulatory text to observable control operations.

- Regulatory Requirement Mapping: Applicable statutes, supervisory guidance, licensing obligations, and sponsor bank standards are mapped directly to required control outcomes.

- Control Design Evaluation: Each control is assessed against regulatory intent, including objective, scope, thresholds, frequency, and escalation criteria.

- Operational Execution Testing: Controls are tested for actual performance, consistency, reviewer actions, and adherence to documented procedures.

- Evidence and Audit Trail Validation: Required artifacts are verified for completeness, retention, traceability, and suitability for retrospective testing.

- Governance and Ownership Assessment: Roles, escalation authority, and oversight structures are evaluated for documented accountability and real decision-making authority.

- Gap Classification and Severity Scoring: Identified gaps are categorized and scored based on regulatory exposure, sponsor bank tolerance, and exam risk.

A compliance gap assessment converts regulatory expectations into verifiable control requirements. It replaces assumptions with documented, testable readiness before banks, regulators, or investors review the program.

If your team needs experienced compliance leadership to review gaps, interpret regulatory expectations, and guide remediation ahead of audits or sponsor bank reviews, Fraxtional provides fractional expertise that embeds directly with your organization.

What a Practical Gap Assessment Template Includes

A practical compliance gap assessment template translates regulatory expectations into auditable checkpoints. It documents control intent, operating reality, evidence quality, and regulatory exposure in a single working artifact.

A well-built gap assessment template functions as an exam-ready control ledger. It links regulatory text to operational proof and exposes weaknesses before external review occurs.

If third-party relationships affect your compliance posture, understanding how regulators evaluate vendor oversight becomes part of the gap assessment itself. See Third-Party Risk Assessment Guide and Best Practices.

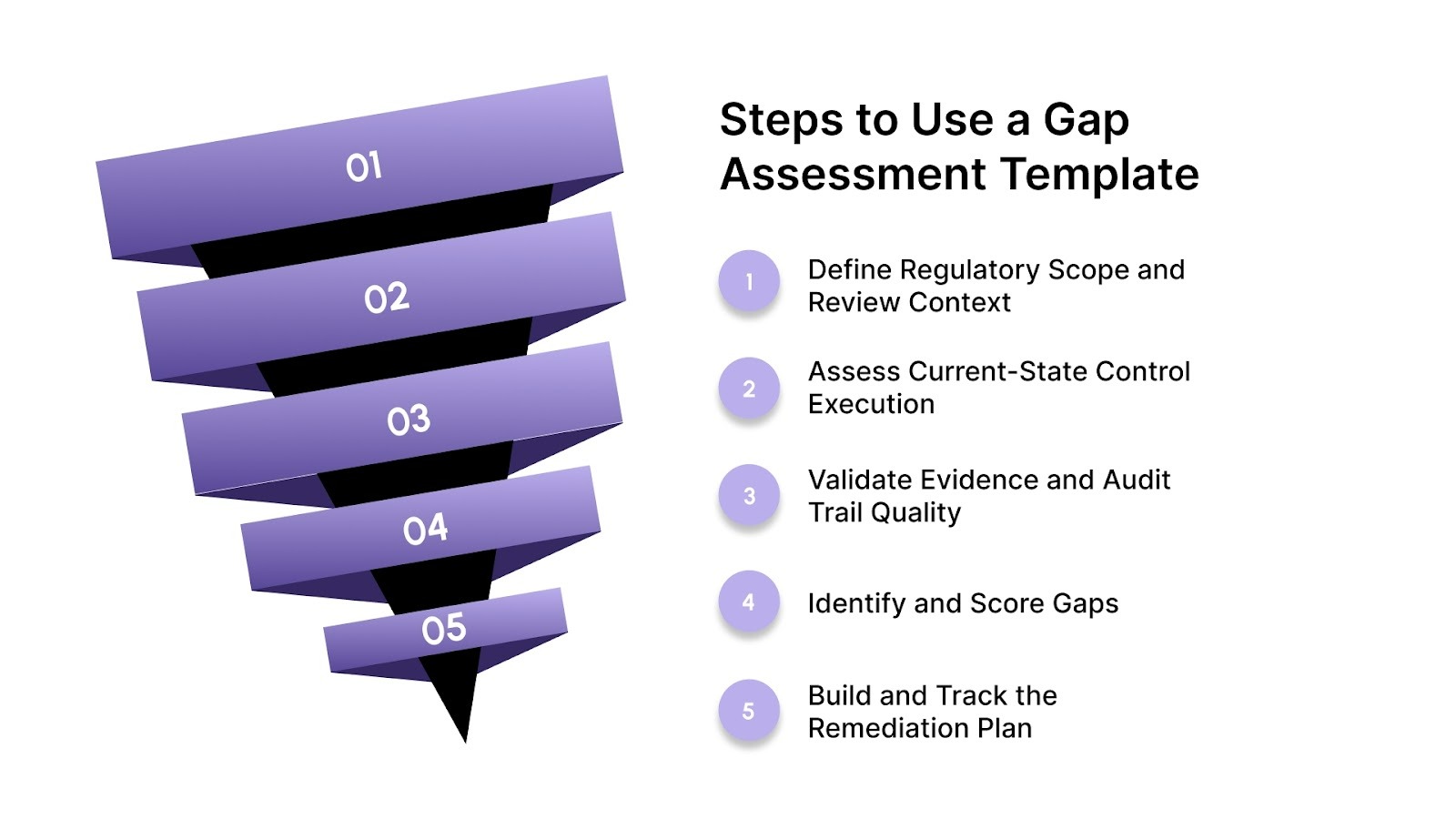

How to Use a Gap Assessment Template Step by Step

A gap assessment template is only effective when applied with regulatory scope, execution testing, and evidence discipline, converting documented expectations into verifiable, review-ready control outcomes.

Step 1: Define Regulatory Scope and Review Context

Establish the exact regulatory, audit, and sponsor bank standards the assessment must satisfy to prevent misaligned testing and incomplete coverage.

- Regulatory Scope Definition: Identify applicable statutes, guidance, licensing obligations, and sponsor bank requirements driving control expectations and review depth.

- Review Trigger Identification: Clarify whether the assessment supports audit prep, sponsor bank onboarding, exam response, or internal remediation planning.

- System and Product Mapping: Map products, transaction flows, and systems in scope to avoid assessing controls disconnected from actual risk exposure.

Step 2: Assess Current-State Control Execution

Evaluate how controls operate in practice, not how they are described, focusing on frequency, thresholds, reviewer actions, and consistency.

- Control Operation Testing: Verify controls execute at stated cadence with documented decision logic and defined thresholds.

- Role and Responsibility Validation: Confirm named owners actively perform reviews and hold escalation authority.

- Workflow Alignment Check: Guarantee operational workflows match documented control procedures without informal workarounds.

Step 3: Validate Evidence and Audit Trail Quality

Confirm each control produces reproducible, time-bound artifacts that withstand retrospective testing during audits and regulatory lookbacks.

- Evidence Artifact Review: Inspect logs, alerts, reports, approvals, and tickets required to evidence each control cycle.

- Retention and Accessibility Testing: Verify evidence is retained, searchable, and attributable to specific review periods.

- Sampling Readiness Check: Confirm evidence supports independent sampling without reliance on narrative explanations.

Step 4: Identify and Score Gaps

Compare observed execution against regulatory expectations and assign severity based on enforcement risk and external reviewer impact.

- Gap Classification: Distinguish design gaps, execution gaps, governance gaps, and evidence gaps.

- Regulatory Severity Scoring: Score gaps based on statutory exposure, sponsor bank tolerance, and exam escalation risk.

- Reviewer Interpretation Analysis: Document how regulators or banks are likely to interpret each gap during review.

Step 5: Build and Track the Remediation Plan

Translate gaps into sequenced corrective actions with owners, dependencies, and measurable completion criteria.

- Remediation Action Definition: Specify corrective steps tied to regulatory intent, not cosmetic documentation fixes.

- Ownership and Authority Assignment: Assign remediation to accountable roles with approval and escalation authority.

- Progress and Closure Tracking: Track remediation through evidence-based milestones rather than self-attested completion.

A gap assessment template delivers value when applied with execution testing, evidence discipline, and regulatory context. Proper use converts identified gaps into defensible, review-ready remediation outcomes.

Use this list to assess whether your bank’s compliance activities align with what examiners and auditors actually test. That same examiner's focus is detailed in Key Activities to Enhance Bank Compliance Management, which outlines the specific activities reviewers expect to see in practice.

Key Questions to Ask During a Gap Assessment

These questions reflect how auditors, sponsor banks, and regulators probe compliance programs to determine whether controls operate as documented and withstand testing.

Regulatory Scope and Applicability

- Which specific statutes, supervisory guidance, and sponsor bank requirements apply to each product, jurisdiction, and transaction flow?

- Where are regulatory expectations interpreted internally without documented support?

- Which controls exist solely due to historical practice rather than current regulatory obligation?

Control Design and Intent

- What regulatory outcome is each control intended to achieve, and how is success measured?

- Are thresholds, frequency, and escalation criteria explicitly defined or assumed?

- Where does control design rely on manual judgment without documented parameters?

Control Execution

- How often is the control actually performed compared to its documented cadence?

- Who performs the control, and do they have documented authority to escalate or block activity?

- Where do operational workarounds replace documented procedures?

Evidence and Audit Trail

- What artifacts prove the control operated for a specific review period?

- Is the evidence reproducible, time-bound, and attributable to a named reviewer?

- Can evidence support independent sampling without explanation or reconstruction?

Governance and Accountability

- Who owns the control outcome, not just the task execution?

- How are issues escalated, documented, and resolved at the committee or board level?

- Where do governance forums exist without demonstrable decision records?

Third-Party and System Dependencies

- Which vendors, platforms, or engineering teams materially affect control execution?

- How are vendor deficiencies tracked, challenged, and remediated over time?

- Where does system design constrain compliance obligations without documented acceptance?

Remediation and Sustainability

- Which gaps represent isolated failures versus systemic weaknesses?

- Are remediation actions addressing the root cause or only closing documentation gaps?

- How will control performance be validated post-remediation?

Effective gap assessments are driven by precise questions that expose execution risk. These inquiries force alignment between regulatory expectations, operational reality, and defensible evidence before external review occurs.

Use this guide to understand how internal audits are planned, executed, and evaluated across regulated financial institutions. That audit lens is detailed in Comprehensive Guide to Internal Audits and Their Importance, which shows how controls and evidence are reviewed.

Do’s and Don’ts in a Gap Assessment Template for Regulated Financial Businesses

Recurring regulatory and sponsor-bank findings reveal consistent execution failures that determine whether a gap assessment template withstands diligence, audits, and examinations.

An effective gap assessment template distinguishes compliant intent from provable execution. These do’s and don’ts reflect how sponsor banks and regulators actually evaluate risk programs in practice.

See how a fractional Chief Revenue Officer strengthens execution and go-to-market accountability. That execution discipline is critical to scaling revenue functions, and Fractional Chief Revenue Officer: Key Business Impacts explains how it is achieved.

Turning Gap Assessment Findings into an Actionable Remediation Plan

Gap assessment findings only reduce regulatory exposure when converted into sequenced corrective actions that map directly to examiner expectations, bank risk tolerances, and operational dependencies.

- Regulatory Severity Sequencing: Order fixes by enforcement risk, consent order relevance, and sponsor-bank rejection triggers, not internal convenience or effort estimates.

- Control Redesign, Not Patching: Rebuild deficient controls to meet regulatory intent and testing standards rather than layering temporary manual workarounds.

- Evidence-First Execution: Define required artifacts upfront and design workflows to generate reproducible, time-stamped evidence per control cycle.

- Ownership With Enforcement Authority: Assign remediation owners with documented approval rights, escalation power, and accountability for missed timelines.

- Dependency-Aware Timelines: Sequence remediation around data availability, vendor changes, model tuning, and licensing constraints to avoid false completion.

Effective remediation converts identified gaps into regulator-verifiable outcomes. Execution discipline, evidence quality, and sequencing determine whether issues close or resurface during review.

How Fraxtional Approaches Compliance Gap Assessments

Fraxtional delivers compliance gap assessments that identify compliance and operational risk exposure and produce documentation designed to withstand audits, investor reviews, and sponsor bank evaluations.

- Full Risk Mapping: Assesses compliance, product, people, and infrastructure risk across policies, controls, vendors, engineering, and operations.

- Implementation Review: Reviews documented policies and controls alongside actual implementation to identify execution gaps.

- Review-Condition Testing: Evaluates how controls hold up under regulator, auditor, and investor scrutiny.

- Prioritized Risk Findings: Delivers findings organized by severity and urgency with specific, non-generic remediation guidance.

- Compliance-Ready Reporting: Provides professional documentation suitable for board review, sponsor bank evaluation, and audit trail support.

Schedule a risk review with Fraxtional to identify material compliance gaps, receive prioritized remediation guidance, and produce documentation that stands up to sponsor banks, auditors, and investor review.

Conclusion

Compliance and risk programs rarely fail because intent is unclear. They fail when control execution, ownership, evidence, and escalation paths cannot be demonstrated during sponsor bank, audit, or regulatory review. A well-constructed gap assessment template exposes those weaknesses before external scrutiny, forcing alignment between documented controls and how teams actually operate.

A defensible gap assessment template connects regulatory requirements to real workflows, retained evidence, and accountable owners, making remediation measurable and review-ready. For teams preparing for audits, sponsor bank onboarding, or examinations, Fraxtional helps convert assessment findings into documentation and controls that hold up under real-world testing rather than post-review correction.

If your program is approaching external review, speak with Fraxtional to confirm your gap assessment approach is built for examination, not cleanup.

FAQs

Yes. Incomplete scoping, undocumented assumptions, or untracked gaps can be interpreted as acknowledged weaknesses during audits or sponsor bank diligence.

It should be updated when products, transaction flows, vendors, geographies, or regulatory guidance change, not on a fixed annual cadence.

Yes. Regulators and banks expect transparent documentation of deficiencies, severity rationale, and remediation tracking, not sanitized or “pass-only” assessments.

Yes. Gap assessments test control execution against external expectations, while risk assessments focus on inherent and residual risk from the institution’s perspective.

Yes. Sponsor banks may request templates, evidence references, and remediation logs to validate how conclusions were reached and whether issues were independently assessed.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.