Jan 27, 2026

Vendor Management Policy Guide: From Risk Questions to Audit-Ready Execution

By Fraxtional LLC

Summarize the blog with AI

Vendor relationships often expand faster than the controls used to govern them. That gap usually becomes visible during audits, sponsor bank reviews, or licensing diligence, when regulators expect documented third-party oversight rather than informal assurances.

This is why a vendor management policy is a foundational control. Most searches for a vendor management policy stem from regulatory pressure, where compliance leaders need to show that vendor risk is identified, governed, and owned by the organization.

The concern is structural rather than theoretical. Third-party gaps frequently become material risk when vendor reliance grows faster than oversight mechanisms. As outsourcing, cloud services, and embedded partnerships increase, regulatory scrutiny continues to intensify.

A well-constructed vendor management policy defines how vendors are assessed, approved, monitored, escalated, and exited in a way that withstands review.

In this guide, we explain how to operationalize that policy, including the role of SOC 2 reports, ISO 27001 certifications, structured vendor risk assessments, and independent audits.

Key Takeaways

- Auditors and sponsor banks expect vendor due diligence to be supported by verifiable artifacts such as SOC 2 Type II reports, ISO 27001 certifications, and penetration test summaries.

- Vendor risk tiering must be defensible through documented scoring criteria tied to data sensitivity, regulatory impact, and operational dependency.

- Vendor management policies fail review when contractual clauses do not enforce audit rights, breach notification timelines, and liability for vendor-caused incidents.

- Ongoing vendor oversight is evaluated through retained evidence, including reassessment records, issue remediation tracking, and management reporting.

- Vendor termination is treated as a control event, requiring proof of access revocation and certified data disposition to close residual risk.

What Is a Vendor Management Policy?

A vendor management policy is a formal third-party risk control that defines how an organization governs external vendors, contractors, and service providers whose services create regulatory, security, or operational exposure. Regulators and auditors review this policy to confirm that third-party risk is contractually enforceable, actively monitored, and tied to escalation authority.

Key Components of an Effective Vendor Management Policy

The following elements define how vendor oversight is operationalized, reviewed, and enforced across the vendor lifecycle, from initial engagement through termination.

- Third-Party Scope Definition: Clearly identifies which vendors fall under policy coverage, including contractors, subprocessors, technology providers, and outsourced compliance functions.

- Service Level and Performance Standards: Establishes enforceable SLAs tied to uptime, response times, data handling, and issue remediation obligations.

- Control and Oversight Requirements: Documents the specific controls the company maintains over vendors, including access restrictions, reporting obligations, and audit rights.

- Compliance and Security Benchmarks: Specifies mandatory standards vendors must meet, such as SOC 2, ISO 27001, or equivalent regulatory expectations.

- Management Escalation Triggers: Defines conditions requiring management intervention, including control failures, SLA breaches, or regulatory findings.

- Third-Party Liability and Risk Transfer Terms: Outlines indemnification, insurance, and responsibility allocation for vendor-caused incidents.

- Incident Response and Termination Rights: Covers disaster recovery obligations, breach response coordination, and termination rights when standards are not met.

A vendor management policy operates like a compliance contract framework rather than a procedural guide. Its strength is measured by enforceability, escalation clarity, and alignment with regulatory and audit expectations.

Why a Vendor Management Policy Matters for Regulated Businesses

For regulated businesses, a vendor management policy functions as a regulatory control that demonstrates third-party risk ownership. Banks, regulators, and auditors rely on this policy to assess whether vendor risk is identified, contractually controlled, and actively governed rather than informally managed.

- Regulatory Accountability: Establishes documented responsibility for third-party actions that affect compliance obligations, including AML, data protection, and consumer safeguards.

- Bank Sponsorship Eligibility: Serves as a required control during sponsor bank due diligence, particularly for fintech and payments companies relying on outsourced infrastructure.

- Audit and Examination Readiness: Provides a reviewable framework that auditors use to test vendor onboarding, monitoring, escalation, and termination evidence.

- Third-Party Risk Containment: Limits exposure created by vendors with system access, transaction authority, or customer data handling responsibilities.

- Contract Enforceability: Connects compliance expectations to binding contractual terms such as audit rights, breach notification timelines, and remediation obligations.

- Incident Response Coordination: Defines how vendor-related failures are escalated, investigated, and reported within regulatory timelines.

- Licensing and Renewal Support: Supports money transmitter, lending, and virtual asset licensing reviews where third-party reliance is closely examined.

A vendor management policy is evaluated as proof of third-party governance maturity. Its absence or weakness often results in delayed approvals, failed audits, or heightened regulatory scrutiny.

5 Questions That Identify Vendor Risk Potential

Vendor risk is not determined by vendor size or cost. It is determined by how deeply a third party touches regulated systems, sensitive data, and core operations.

These questions are used during onboarding and periodic reviews to determine inherent risk, oversight depth, and approval thresholds.

The questions that drive risk classification

Rather than broad assessments, reviewers focus on a small set of high-impact factors:

- Does the vendor have direct access to production systems, administrative privileges, or live data flows?

- What data does the vendor process or store, where it is hosted, and whether subprocessors are involved?

- Whether a vendor failure would trigger regulatory reporting, bank notification, or customer disclosure?

- How quickly can the service be replaced without breaching recovery objectives or disrupting operations?

- Can the vendor provide current audit reports, security certifications, and documented incident response procedures?

Clear, documented answers to these questions determine risk tiering, due diligence requirements, and escalation authority before contracts are executed.

If vendor oversight is under regulatory or audit review, a structured risk assessment can surface gaps before they become findings. Learn how to evaluate third-party exposure with this Third-Party Risk Assessment Guide and Best Practices.

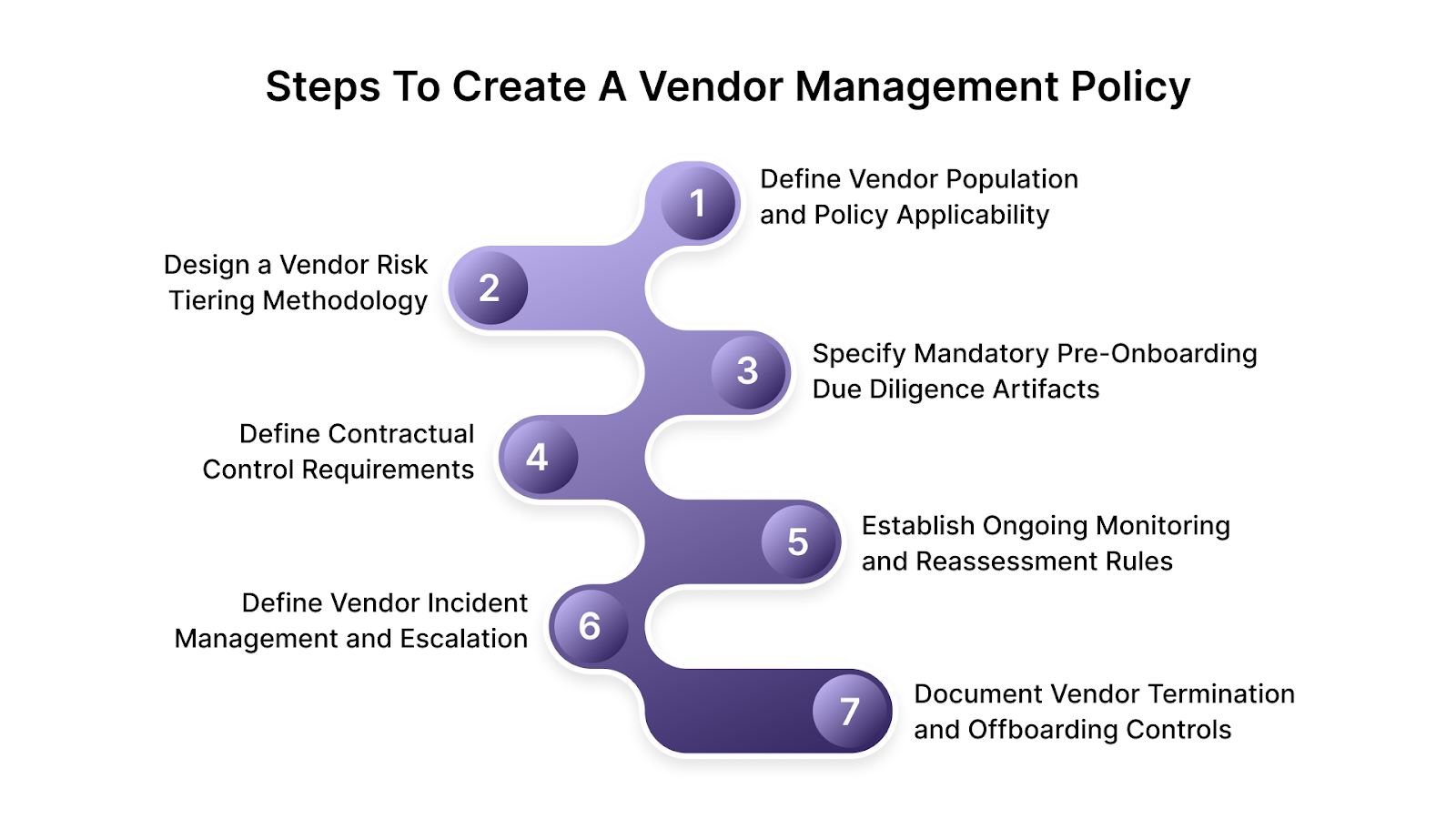

How to Create a Vendor Management Policy Step by Step

A vendor management policy is constructed by defining enforceable decision criteria, mandatory evidence, approval authority, and lifecycle controls for third parties that introduce regulatory, operational, or data risk. Each step below corresponds to a control area that examiners explicitly test.

Step 1: Define Vendor Population and Policy Applicability

Establish exactly which third parties are governed by the policy using objective inclusion rules tied to risk exposure.

Key Tips:

- Applicability Thresholds: Include vendors with production system access, customer PII access, transaction execution authority, compliance outsourcing, or business continuity dependency.

- Vendor Type Mapping: Categorize vendors by function, such as infrastructure, payments, data processing, compliance services, customer support, and analytics.

- Named Accountability: Assign a single internal owner per vendor responsible for risk acceptance and ongoing compliance.

Step 2: Design a Vendor Risk Tiering Methodology

This establishes a consistent way to classify vendors by risk so oversight levels, approvals, and controls are applied proportionately and defensibly.

Key Tips:

- Risk Factors Defined: Score vendors based on data sensitivity, regulatory impact, operational criticality, and substitutability.

- Tier Thresholds Set: Establish numeric or rule-based cutoffs for critical, high, medium, and low risk classifications.

- Control Depth Mapping: Specify which tiers require improved due diligence, executive approval, and board visibility.

Step 3: Specify Mandatory Pre-Onboarding Due Diligence Artifacts

Before a vendor is approved, risk must be assessed using verifiable evidence rather than assumptions. This step defines the exact documents and validations required to confirm a vendor can meet security, compliance, and operational expectations before access is granted or contracts are signed.

Key Tips:

- Security and Control Evidence: Require SOC 2 Type II reports, ISO 27001 certificates, penetration test summaries, or equivalent control attestations.

- Compliance Alignment Review: Validate vendor alignment with applicable regulatory regimes such as AML, data protection, and consumer protection obligations.

- Financial and Operational Viability: Review financial statements, continuity plans, and dependency risks for critical vendors.

Step 4: Define Contractual Control Requirements

Policies alone do not control vendor risk unless the requirements are written into contracts. This step guarantees that compliance, security, and oversight expectations are legally binding and enforceable throughout the vendor relationship.

Key Tips:

- Audit and Inspection Rights: Require contractual rights to request control evidence and conduct audits.

- Breach and Incident Notification Windows: Mandate reporting timelines aligned with regulatory disclosure requirements.

- Risk Transfer Mechanisms: Define indemnification, insurance coverage, and liability allocation for vendor-caused failures.

Step 5: Establish Ongoing Monitoring and Reassessment Rules

After a vendor is approved, oversight must continue throughout the relationship. This step defines how often vendors are reviewed, what events trigger immediate reassessment, and how review evidence is maintained so risk decisions remain current and defensible.

Key Tips:

- Review Cadence by Tier: Require annual reassessments for critical vendors and periodic reviews for lower-risk tiers.

- Trigger-Based Reviews: Mandate reassessments following incidents, scope changes, control failures, or regulatory findings.

- Evidence Retention Standards: Specify documentation retention periods and audit traceability requirements.

Step 6: Define Vendor Incident Management and Escalation

Establishes how vendor-related issues are assessed, escalated, and resolved when they impact systems, data, or compliance obligations.

Key Tips:

- Severity Classification: Define incident categories based on data exposure, service disruption, and regulatory impact.

- Escalation Authority: Identify who approves regulatory notifications, bank communications, and customer disclosures.

- Corrective Action Tracking: Require documented remediation plans and validation of vendor fixes.

Step 7: Document Vendor Termination and Offboarding Controls

When a vendor relationship ends, the risk does not automatically end with it. This step makes sure nothing is left behind that could create future exposure.

Key Tips:

- Access Decommissioning Verification: Require confirmation of revoked credentials and system access.

- Data Disposition Controls: Document data return, certified destruction, or lawful retention requirements.

- Post-Termination Risk Closure: Perform final validation to confirm no ongoing operational or compliance exposure.

If building and executing these controls feels resource-intensive, Fraxtional helps regulated teams translate vendor management requirements into audit-ready policies and workflows that hold up under bank, regulator, and SOC 2 review, without slowing day-to-day operations. Get in touch with us!

Regulatory Requirements That Influence Vendor Management Policies

Vendor management policies are shaped by specific regulatory expectations that govern third-party accountability, outsourcing risk, and control enforceability. Regulators evaluate these policies to confirm that responsibility for compliance remains with the regulated entity, even when activities are outsourced.

- Banking and Financial Regulator Outsourcing Rules

US banking regulators and supervisory bodies require documented third-party oversight, including risk assessments, contract controls, and ongoing monitoring for all material service providers.

- Data Protection and Privacy Obligations

Data protection laws impose explicit requirements for vendor data access limitations, subprocessor disclosures, cross-border data handling, and breach notification coordination.

- Operational Resilience and Business Continuity Standards

Regulators expect policies to address vendor concentration risk, recovery time objectives, and continuity planning for critical third-party services.

- Audit and Assurance Expectations

Examination frameworks require vendors to provide independent assurance evidence, such as SOC reports or equivalent, to validate control effectiveness.

- Accountability and Governance Requirements

Regulatory guidance mandates clear internal ownership, escalation authority, and senior management accountability for third-party risk decisions.

Regulatory requirements shape vendor management policies by defining non-transferable accountability. Policies that fail to reflect these obligations are routinely challenged during examinations and audits.

Common Vendor Management Policy Gaps Found in Audits

Audits and regulatory reviews consistently identify gaps where vendor management policies exist on paper but fail to produce enforceable controls or retained evidence. The table below highlights deficiencies most frequently cited in bank reviews, SOC 2 examinations, and regulatory audits.

These gaps reflect failures in execution and evidence retention rather than policy intent. Auditors evaluate vendor management maturity by tracing from policy language to documented actions.

As regulatory scrutiny increases, aligning vendor oversight with broader compliance priorities becomes critical. Explore proven approaches in Top Compliance Risk Management Strategies for 2025.

Vendor Management Policy Best Practices for Ongoing Oversight

Ongoing oversight validates that vendor risk remains within approved tolerance after onboarding. Regulators and auditors evaluate this phase to confirm that third-party controls are continuously enforced, exceptions are managed, and risk decisions are revisited as conditions change.

- Evidence-Based Review Cycles: Require current control artifacts such as updated SOC reports, penetration test summaries, and compliance attestations at defined intervals.

- Change-Driven Reassessment: Mandate immediate reviews when vendor scope, data access, hosting location, or subcontractor usage changes.

- Centralized Issue Tracking: Maintain a formal register for vendor findings, remediation actions, owners, and closure evidence.

- Management Reporting Cadence: Produce periodic summaries of vendor risk posture, open issues, and escalations for senior leadership review.

- Exception Governance Controls: Document risk exceptions with expiration dates, compensating controls, and executive approval.

Effective oversight is demonstrated through documented reassessments, tracked remediation, and management visibility. Policies that lack these controls fail to show continuous third-party risk governance.

How Fraxtional Supports Vendor Management Policy Execution

Fraxtional supports vendor management policy execution by converting policy language into audit-defensible controls, evidence workflows, and ownership models that meet bank, regulator, and investor scrutiny.

1. Audit-Ready Policy Development

Draft vendor management policies built for sponsor bank reviews, SOC 2 audits, and regulatory exams, with clear control language, ownership, and version tracking.

2. Control Mapping to Real Operations

Aligns vendor oversight requirements to actual systems, vendors, and workflows rather than abstract templates, reducing audit findings tied to policy mismatch.

3. Evidence and Documentation Structure

Establishes documentation standards that show vendor approvals, reviews, exceptions, and remediation in a format auditors can trace and validate.

4. Fractional Compliance Leadership

Provides interim or fractional CCO, CRO, MLRO, and AML leadership to oversee vendor risk decisions, approvals, and escalations.

5. Bank and Audit Review Support

Prepares teams for sponsor bank diligence, independent audits, and SOC 2 reviews by stress-testing vendor controls before formal review.

Fraxtional helps regulated companies move from policy intent to provable execution. Vendor management programs are built to withstand review, not rewritten after findings surface. Connect with Fraxtional!

Conclusion

Vendor risk rarely fails because policies are missing. It fails when oversight cannot be demonstrated under review. Regulators, banks, and auditors assess vendor management by tracing decisions, evidence, and accountability across the full vendor lifecycle.

A defensible vendor management policy closes that gap by connecting risk assessment, contractual controls, ongoing oversight, and incident response into a single, review-ready framework. When those elements are aligned, vendor risk becomes manageable rather than reactive.

For teams preparing for audits, bank partnerships, or licensing reviews, Fraxtional helps translate vendor management requirements into policies and controls that withstand scrutiny. Our compliance leaders work alongside your team to build audit-ready documentation and execution frameworks that hold up when it matters most.

If vendor oversight is coming under review, speak with Fraxtional to guarantee your vendor management policy is built for real-world examination, not post-audit revisions.

FAQs

A vendor management policy should be reviewed at least annually and updated after regulatory changes, audit findings, material vendor incidents, or significant business model changes.

Yes. If monitoring activities are not documented, approved, and traceable to policy requirements, auditors treat the vendor management policy as ineffective.

For regulated companies, formal approval is typically expected at the senior management or board level to demonstrate accountability for third-party risk decisions.

A vendor management policy should require disclosure and oversight of subcontractors when they access systems, data, or regulated processes, not only direct vendors.

Yes. Auditors and sponsor banks use the vendor management policy to test risk tiering, due diligence evidence, contract controls, and ongoing oversight practices.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.