Nov 13, 2025

Fractional CRO Strategy for Fintech Growth Explained

By Fraxtional LLC

Summarize the blog with AI

FinTech strategy used to mean product expansion and user growth.

Now, it means passing a regulator’s test before you pass a market’s.

Every funding round, sponsor-bank partnership, and licensing application now hinges on one question: can this company manage risk at scale?

The answer increasingly comes from outside the payroll.

Fractional Chief Risk Officers are becoming central to how fintechs and challenger banks grow. Beyond compliance oversight, they shape markets, partnerships, and timing decisions that determine whether a company scales responsibly or stalls under scrutiny.

This shift follows sharper oversight.

Regulators in the U.S. and U.K. have tightened expectations around outsourcing, data handling, and consumer protection.

The OCC’s expanded third-party risk guidance and the FCA’s operational-resilience tests now reach even non-bank firms.

For fintechs built on sponsor-bank infrastructure, these frameworks decide access to payment rails, investor trust, and long-term credibility.

Founders can no longer separate growth from governance. A funding round that once depended on user metrics now turns on the firm’s ability to demonstrate risk maturity. Sponsor banks no longer ask if compliance exists, but who owns it.

Fractional CROs bring that ownership.

They move compliance from reaction to structure, building risk systems that accelerate licensing, strengthen bank integrations, and inspire investor confidence.

In modern finance, that’s called strategy.

Key Takeaways

- FinTech strategy today begins with regulatory trust, not just market traction.

- Fractional CROs bring senior risk leadership to startups that can’t yet justify full-time roles.

- They align growth plans with compliance expectations from banks, investors, and regulators.

- The model delivers enterprise-grade governance that scales with agility and cost efficiency.

- Fraxtional embeds fractional CROs who turn risk management into a core part of fintech strategy.

How Fractional CROs Bridge the Gap Between Banking Discipline and FinTech Growth

FinTechs move fast; banks move within boundaries. Both models work until they have to work together.

In banking, risk has always been part of strategy. Capital allocation, product rollout, and regulatory engagement operate under established governance models tested, layered, and deliberate.

FinTechs, by contrast, scale through speed, integrations, and market fit before governance frameworks catch up. That difference creates friction the moment a startup enters a sponsor-bank review or investor audit.

Fractional Chief Risk Officers bridge that divide. They bring the same discipline banks rely on but adapt it to the tempo of high-growth environments. Instead of imposing rigid frameworks, they translate regulatory expectations into operating systems that founders can sustain.

In early stages, they help define risk appetite, clarifying which licenses, partnerships, or market entries align with the company’s capacity and compliance obligations.

As growth accelerates, they formalize controls across data privacy, AML, and operational resilience, ensuring the business can meet due diligence without losing momentum.

For banks, a fractional CRO signals reliability; for founders, it’s access to institutional-grade governance without institutional weight.

The result is a shared language between innovators, investors, and regulators, one that turns risk management from a checkpoint into a strategic lever for scale.

The governance logic that defines banking can feel foreign to fintech founders used to iteration and speed. A fractional CRO makes it actionable, turning broad regulatory expectations into specific business behaviors.

That translation is where their real influence begins.

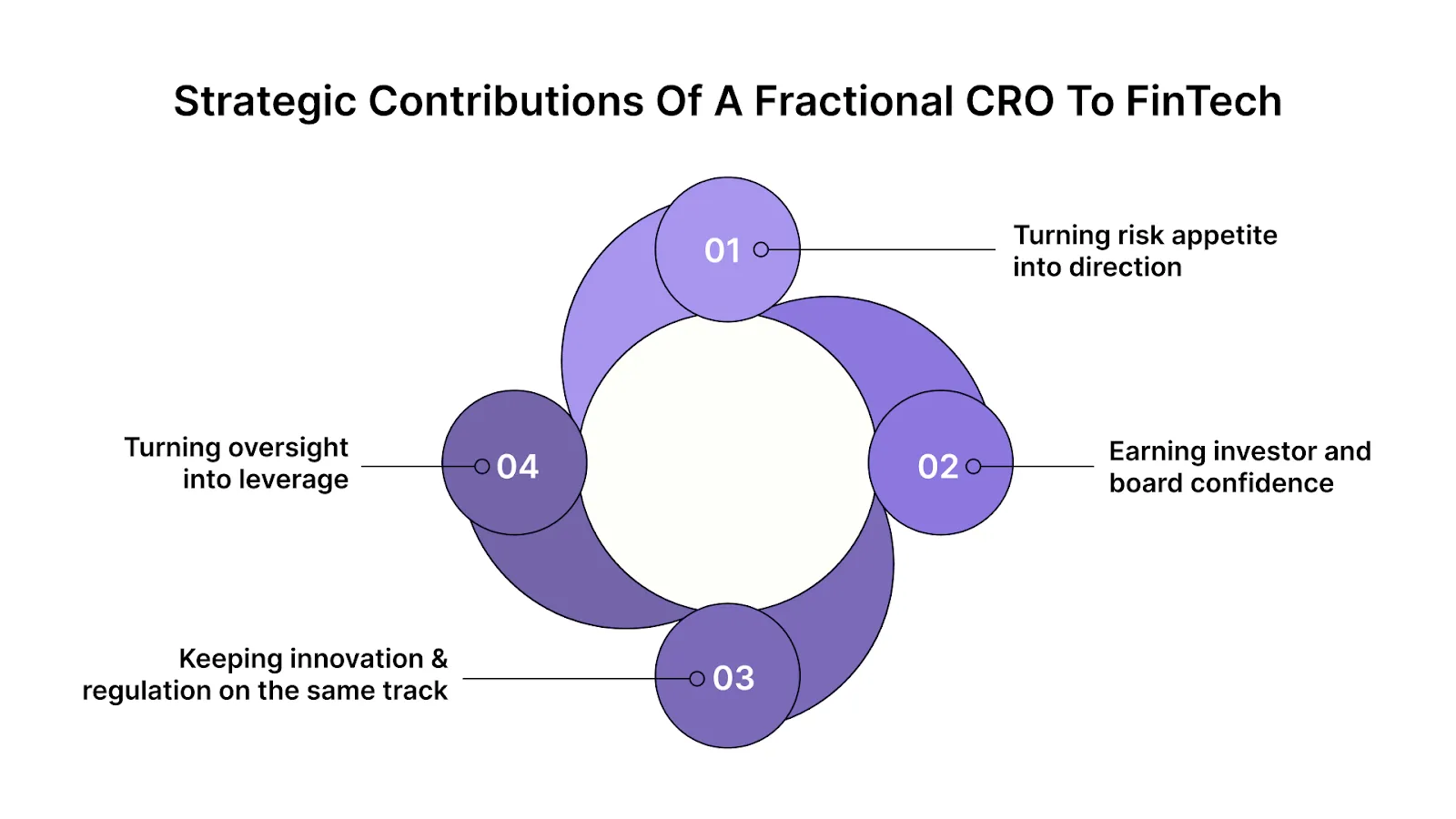

Strategic Contributions of a Fractional CRO to FinTech

In fintech, where new products, licenses, and partnerships develop in parallel, the fractional CROs work to ensure that speed doesn’t dilute control or clarity.

1. Turning risk appetite into direction

Most fintechs grow before they fully understand their tolerance for risk. A fractional CRO establishes that foundation early, outlining credit exposure limits, data-use parameters, and vendor thresholds.

Once those markers are set, the business can expand without stepping into blind spots.

2. Earning investor and board confidence

Investors now look for operational discipline alongside innovation. Fractional CROs give them that assurance through structured reporting, risk dashboards, and defined ownership.

Boards gain visibility into exposure; investors gain confidence that growth is being managed, not just pursued.

3. Keeping innovation and regulation on the same track

Product launches often race ahead of compliance. A fractional CRO integrates risk evaluation into development cycles, aligning release timelines with regulatory expectations.

It prevents last-minute course corrections and ensures that new offerings meet both market and oversight demands.

4. Turning oversight into leverage

Sponsor banks and regulators judge fintechs by the quality of their governance. Fractional CROs create tangible proof, control matrices, incident protocols, and vendor scorecards that stand up to external review.

That credibility accelerates partnerships and market access, apart from avoiding penalties.

Together, these shifts redefine how fintechs view governance. Risk is no longer the brake on growth; it’s the infrastructure that sustains it. Fractional CROs make that infrastructure flexible, measurable, and credible enough to support expansion without compromise.

Engagement Models That Work for FinTechs

The CRO function has traditionally been built for banks, full-time, hierarchical, and supported by large compliance teams.

Fintechs, by contrast, operate lean. They need the same judgment and structure, but in a format that fits their growth curve.

Fractional CROs bridge that gap through engagement models tailored to stage, funding, and regulatory exposure.

1. Advisory for early-stage fintechs

Seed and pre-Series A companies often face compliance questions before they even launch from sponsor banks, regulators, or investors.

Fractional CROs engage as advisors here, creating the initial risk map, defining appetite, and setting up basic reporting and due diligence protocols. The goal is to create a credible structure early enough to earn trust.

2. Embedded leadership during growth and licensing

Once a fintech starts scaling, the stakes rise. Sponsor-bank reviews, licensing applications, and cross-border partnerships demand continuous oversight.

Fractional CROs often step into interim or embedded roles at this stage, guiding policy design, vendor oversight, and board governance while training internal teams to manage risk independently over time.

3. Continuous assurance for mature or regulated entities

For licensed digital banks or payment institutions, fractional CROs provide periodic independent assurance, validating control design, reviewing third-party risks, and preparing the firm for audits.

This model preserves internal efficiency while maintaining external credibility with regulators and partners.

Across all these models, the value remains consistent: access to executive-level risk leadership that scales with the business.

Why the Fractional Model Is Redefining Risk Leadership

Traditional governance assumes stability.

Fintech assumes change.

That’s where the fractional model fits; it provides continuity without rigidity.

Full-time CROs make sense for institutions with predictable structures and steady regulatory scope. But in fintech, where new integrations, product pivots, and market entries happen quarterly, fixed roles can become outdated as quickly as the frameworks they design.

The fractional model answers that problem with mobility.

It allows companies to access deep regulatory and operational expertise precisely when the need peaks during licensing, fundraising, or sponsor-bank negotiations and scale it down when systems stabilize. Instead of growing a department, fintechs grow capacity.

This flexibility does more than save cost. It changes how governance evolves. Fractional CROs bring experience drawn from multiple institutions and regulatory environments.

That cross-sector visibility helps fintechs benchmark their practices against banks, payments firms, and digital asset platforms, ensuring their controls are current, not copied.

For investors, it reduces operational risk exposure.

For regulators, it signals credible oversight.

For founders, it keeps control aligned with ambition.

That combination, agility with accountability, is what defines the next generation of fintech strategy.

How Fraxtional Enables FinTechs to Scale with Confidence

Fraxtional’s model is built around precision, embedding seasoned Chief Risk Officers who understand both the language of regulators and the urgency of startups.

Each engagement begins with clarity: mapping the firm’s risk environment, identifying pressure points across partnerships, data systems, and controls, and designing governance that can evolve with growth.

From there, fractional CROs operate as part of the leadership team, guiding strategy, overseeing remediation, and preparing founders for the scrutiny that comes with scaling.

Fraxtional’s strength lies in adaptability. Whether a company is preparing for a sponsor-bank review, expanding internationally, or pursuing a digital banking license, the engagement model adjusts to its stage and exposure.

The outcome remains consistent: visible, defensible, and sustainable governance that accelerates growth.

For emerging fintechs, this can mean the difference between meeting regulatory expectations and exceeding them.

Partner with Fraxtional to embed seasoned CRO leadership into your fintech strategy.

Conclusion

The fintech landscape no longer rewards speed alone. It rewards foresight, the ability to scale under scrutiny, and still retain control.

Fractional CROs represent that shift. They bring the discipline of banking and the agility of startups into one structure, giving fintechs the maturity of an institution without the inertia of one.

For investors, they create assurance, for regulators, accountability, and for founders, clarity.

Fraxtional sits at the center of this evolution, delivering risk leadership designed for growth, built for credibility, and aligned with how fintechs actually operate.

Because in finance, growth only counts when it can stand up to oversight.

FAQs

A fractional Chief Risk Officer (CRO) provides senior-level risk oversight on a flexible basis. They help fintechs build governance frameworks, manage regulatory obligations, and align growth plans with risk appetite — without the need for a full-time executive.

Full-time CROs are costly and often unnecessary during early or mid-growth stages. Fractional CROs bring the same depth of expertise during critical periods, licensing, sponsor-bank reviews, or fundraising, then scale down once systems mature.

They interpret complex banking standards and translate them into actionable processes. From vendor risk mapping to AML controls and board-level reporting, fractional CROs ensure fintechs meet sponsor-bank and regulatory expectations with agility.

The right time is when external scrutiny increases, typically during regulatory licensing, funding rounds, or partnership negotiations. Early engagement helps fintechs build credible risk systems before compliance gaps slow expansion.

Consultants advise and step out once reports are delivered. A fractional CRO embeds within the organization, owns outcomes, and provides ongoing oversight — shaping decisions that affect growth, governance, and investor confidence.

Fraxtional embeds experienced CROs who understand both startup velocity and regulatory precision. They build scalable frameworks for third-party risk, operational resilience, and compliance, enabling fintechs to grow responsibly and earn lasting trust.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.

Now Accepting:

BTC

ETH

USDC

USDP