Jun 27, 2025

Internal Control and Audit Procedures for Effective Management

By Fraxtional LLC

Summarize the blog with AI

Internal controls and audit procedures are essential for effective risk management and compliance. They help organizations safeguard assets, ensure accurate reporting, and prevent fraud. Key points include:

- Internal controls: Policies and processes to manage risks and improve operational efficiency

- Audit procedures: Techniques auditors use to test the design and effectiveness of controls

- Types of controls: Preventive (stop issues before they occur) and detective (identify issues after they occur)

- Benefits: Reduce fraud, ensure regulatory compliance, and enhance accountability

- Importance: Critical for maintaining trust, protecting resources, and supporting business growth

Internal control and audit procedures are at the core of every well-governed organization. They not only help detect and prevent errors or fraud but also ensure compliance with regulatory requirements and promote operational efficiency.

According to the 2024 ACFE Report to the Nations, more than half of occupational frauds occur due to a lack of internal controls or an override of existing internal controls, with 32% attributed to the absence of controls and 19% to management override.

While frameworks like COSO provide a strong foundation, many fast-growing companies struggle to implement internal controls effectively. That’s where platforms like Fraxtional come in, empowering compliance teams to operationalize controls, automate testing, and reduce audit fatigue.

Whether you’re building your compliance program from the ground up or looking to refine your existing framework, understanding these procedures is essential. This blog will dive into:

- What internal controls are and why they matter

- The role of audit procedures in verifying controls and compliance

- Key types of audits and when to use them

- Steps to improve internal control effectiveness

- How internal controls align with broader risk management goals

Let's understand how to approach internal control and audits in a way that supports growth and reduces regulatory risk.

What Are Internal Controls?

Internal controls are the policies, procedures, and processes your organization puts in place to safeguard assets, ensure accurate financial reporting, and promote operational efficiency. They help prevent errors, fraud, and compliance issues by providing clear guidelines on how tasks should be performed and monitored.

Here’s why internal controls matter for your business:

- Protect Your Assets: Internal controls help secure your physical and digital assets from theft, misuse, or loss.

- Ensure Accurate Reporting: They support reliable financial and operational data, which is crucial for decision-making and regulatory compliance.

- Promote Accountability: Clear roles and responsibilities within controls make it easier to identify errors or irregularities and hold people accountable.

- Support Compliance: They help your business meet legal and regulatory requirements, reducing the risk of penalties.

- Improve Efficiency: Well-designed controls streamline processes, helping your team work smarter and reduce waste.

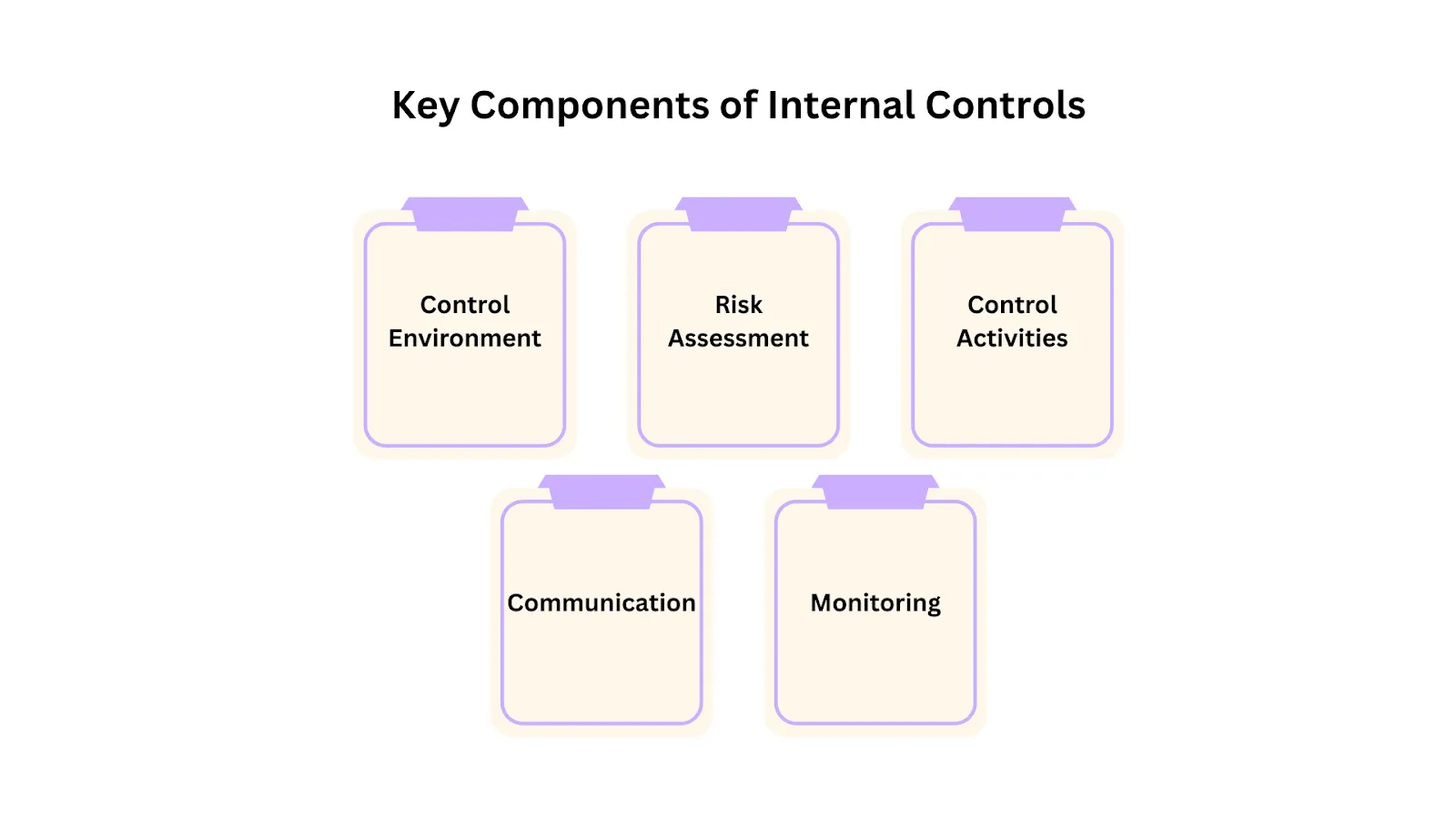

Key Components of Internal Controls

To build an effective internal control system, your organization needs to focus on several core components. Each plays a vital role in protecting your business, reducing risks, and ensuring smooth operations.

- Control Environment

This is the foundation of your internal controls. It includes your company’s core values, ethical standards, management philosophy, and the tone set by leadership. When leaders prioritize integrity and compliance, it creates a culture where everyone understands the importance of controls and follows them consistently. A strong control environment encourages accountability and supports all other control activities. - Risk Assessment

Risk assessment involves identifying potential risks that could stop your business from achieving its goals. These risks might be financial, operational, or regulatory. Once identified, you analyze the likelihood and impact of each risk. This helps you prioritize where to apply controls and how to allocate resources efficiently. A thorough risk assessment ensures you focus on the most critical areas that need protection. - Control Activities

These are the specific policies and procedures you put in place to mitigate identified risks. Control activities can take many forms, including requiring approvals before transactions, performing regular reconciliations, restricting access to sensitive data, and enforcing segregation of duties. These activities are your frontline defense to prevent errors, fraud, and compliance failures. - Information and Communication

Effective internal controls depend on the flow of relevant information across your organization. This means ensuring everyone knows their roles and responsibilities related to controls. It also involves timely communication about any changes in policies, procedures, or risk factors. When information is transparent and accessible, employees can act accordingly to maintain control effectiveness. - Monitoring

Monitoring involves regularly reviewing and testing your controls to verify they are working as intended. This can be done through ongoing activities or periodic assessments like internal audits. Monitoring allows you to detect control failures early and make improvements before small issues turn into big problems. It’s an essential feedback loop that helps maintain and strengthen your internal control system over time.

In the next section, let’s explore the main types you should consider implementing.

What Are the Types of Internal Controls?

Every internal control program has its limits, but implementing the right mix of controls can significantly help your organization meet its objectives and reduce risks. The two main types of internal controls you should focus on are preventive and detective controls.

- Preventive Controls

These controls are designed to stop errors or problems before they happen. By catching issues early, preventive controls reduce the need to find and fix mistakes later. They can be manual, like requiring manager approvals, or automated, such as system access restrictions. Automated controls are particularly valuable because they lower the risk of human error and make audit processes more efficient. Examples include:- Segregation of duties to prevent conflicts of interest

- Approval workflows for expenses above a certain amount

- Background checks during hiring

- Physical security measures like alarm systems and device locks

- Detective Controls

While preventive controls aim to stop issues, detective controls help you find problems that slip through the cracks. They act as a safety net, identifying discrepancies or errors before they escalate. Detective controls work best alongside preventive ones, providing ongoing assurance that your control system is effective. Common examples include:- Regular physical inventory counts

- Reconciliation of accounts

- Matching financial statements with supporting documents

At Fraxtional, our compliance squads combine preventive and detective controls to strengthen your internal systems. From automated approval workflows to real-time alerts for unusual transactions, we help you stay ahead of risk while keeping audits efficient. Ready to simplify compliance? Talk to our team.

What Are Audit Procedures?

Audit procedures are the specific steps and methods auditors use to collect and evaluate evidence during an audit. Whether the audit is internal or external, these procedures ensure the audit is thorough and accurate.

Auditors typically select one or more types of audit procedures based on the audit’s goals and the areas being tested. Not every procedure applies to every audit, but together, they form the foundation of effective audit testing.

Internal audits tend to be ongoing and cyclical, helping organizations continuously manage risk. External audits usually focus on a specific point in time and provide an independent assessment.

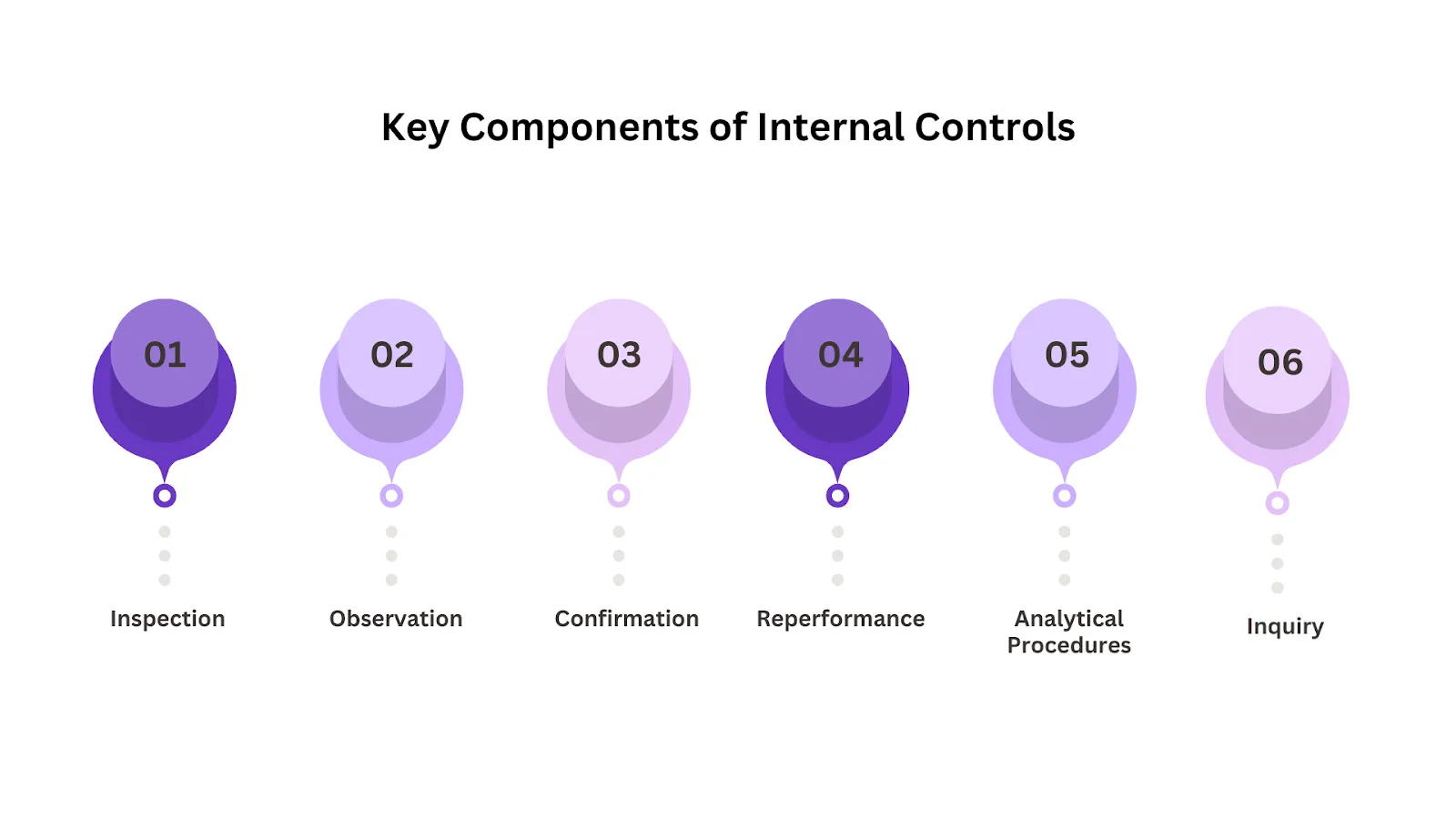

Here are the six key audit procedures you should know:

1. Inspection

This procedure involves examining documents, records, or physical assets to collect evidence about how effectively your controls are operating. Inspection allows auditors to verify the existence, accuracy, and completeness of information.

Example: Reviewing detailed transaction logs for unusual entries, assessing compliance reports to ensure regulatory adherence, or physically inspecting the security measures protecting cryptocurrency hardware wallets.

Inspection helps auditors confirm that what is documented and reported matches reality, forming a factual basis for further testing.

2. Observation

Observation means watching processes and activities as they occur in real time. This lets auditors see firsthand whether your team follows prescribed controls and procedures.

Example: Observing your customer onboarding process to ensure that identity verification complies with Know Your Customer (KYC) regulations.

By witnessing how controls are applied day-to-day, auditors gain valuable insight into operational effectiveness and identify gaps between policy and practice.

3. Confirmation

Confirmation involves obtaining direct verification from external third parties or internal personnel to corroborate information or conditions relevant to the audit.

Example: Requesting a bank to confirm your account balances and verify compliance with transaction limits.

This procedure provides independent assurance that key data points are accurate, trustworthy, and not solely reliant on your internal records.

4. Reperformance

Reperformance is the independent execution of tasks or processes originally carried out by your staff. This verifies whether those activities were performed correctly and effectively.

Example: Recalculating risk assessments or redoing compliance reviews on a sample of transactions to confirm accuracy.

Reperformance acts as a control check, validating the consistency and reliability of your control activities.

5. Analytical Procedures

Analytical procedures consist of reviewing and comparing financial and operational data to identify patterns, trends, or anomalies that may indicate risk or control weaknesses.

Example: Comparing monthly transaction volumes or fee structures against previous periods to spot unexpected spikes or declines that could signal fraudulent activity or process errors.

These analyses help auditors focus attention on areas requiring deeper investigation, making audits more efficient and targeted.

6. Inquiry

Inquiry involves asking questions of knowledgeable individuals within your organization or external partners to gain a clearer understanding of processes, risks, and controls.

Example: Interviewing compliance officers to learn how newly introduced regulations are integrated into your control framework and monitored over time.

Example: Audit Procedures in a Fintech Risk Management Audit

Imagine your fintech company wants to assess the effectiveness of its fraud prevention controls. Here’s how auditors might approach it:

- Identify key risks

Determine the main risks, such as fraudulent transactions, identity theft, or unauthorized access. - Evaluate control design

Review how your fraud detection systems, transaction monitoring, and customer authentication processes are designed to mitigate these risks. - Test control implementation

Perform tests like inspecting transaction alerts, observing fraud investigation processes, and reperformance of monitoring rules on sample transactions. - Assess control effectiveness

Analyze test results and data trends to see if the controls detect and prevent fraud as intended. - Report findings and recommendations

Document any weaknesses found and suggest improvements, such as enhancing alert thresholds or adding employee training on fraud indicators.

Also Read: Comprehensive Guide to Internal Audits and Their Importance

Each audit procedure serves a purpose, but applying them consistently and strategically can be a challenge, especially when teams are balancing competing priorities.

That’s where Fraxtional can help. By embedding these procedures directly into your audit calendar, Fraxtional ensures that reviews happen on a regular cadence without adding stress to internal teams. These reviews are thoughtfully scheduled, so you’re not scrambling during audit season. Instead, your team stays ahead, prepared, organized, and continuously aligned with compliance goals.

When to Use Each Audit Procedure?

Choosing the right audit procedure is all about matching the method to your specific audit goals and the nature of the area being reviewed. Different procedures reveal different types of information, so understanding when to use each one helps you get the most accurate and meaningful insights from your audit.

Here’s a breakdown to help you decide:

- Inspection

Use inspection when you need to verify the existence, accuracy, and completeness of physical assets, documents, or records. This is especially important when you’re dealing with high-value transactions, contracts, or compliance reports that require concrete proof.

Example: If you want to confirm that purchase orders match invoices and payments, inspecting these documents is the way to go. - Observation

Observation is best when you want to see how well your team follows procedures in real time. This is particularly useful for assessing processes that rely heavily on human action, such as security protocols or customer onboarding.

Example: Watching your staff perform identity checks can reveal whether your KYC policies are consistently applied or if there are gaps needing attention. - Confirmation

Turn to confirmation when you need independent verification from outside parties or other internal teams. This is critical for validating information that cannot be verified solely through internal documents.

Example: Confirming bank balances or verifying third-party vendor agreements ensures that your records align with external sources. - Reperformance

Use reperformance to test whether control activities and processes are carried out correctly and consistently by independently replicating the work. This is essential for validating calculations or compliance checks.

Example: Recalculating interest on loans or redoing sample compliance audits can confirm accuracy and adherence to policies. - Analytical Procedures

Analytical procedures are your go-to when you want to quickly identify trends, anomalies, or irregularities in data. These help pinpoint areas of risk or concern that might require deeper investigation.

Example: Spotting unusual spikes in payment volumes or comparing financial ratios over time can highlight potential fraud or errors. - Inquiry

Inquiry is effective when you need to understand the context behind controls and processes. By asking the right questions, you can uncover insights about how risks are managed and whether policies are being followed.

Example: Interviewing compliance managers about new regulations helps you understand how those rules are implemented and monitored across the organization.

Fraxtional Tip: Use control self-assessments to validate effectiveness between audits.

Auditors follow a structured approach to test controls in practice, balancing design and operational effectiveness to provide reliable assurance. Let's take a look at the "How" in the next section.

How Do Auditors Test Internal Controls?

The way auditors decide which internal controls to test depends on several factors, such as your company’s size, complexity, and the nature of your business. A key starting point is a risk assessment conducted by your internal audit team. This helps determine which business units, processes, and systems fall within the scope of testing.

Once the scope is defined, auditors identify the internal controls connected to those areas and rank them based on the level of risk they address. This risk ranking guides the overall testing strategy and the depth of testing required.

Testing internal controls means auditors perform procedures to evaluate two main things:

- Design Effectiveness: Are the controls properly designed to prevent or detect issues?

- Operational Effectiveness: Are the controls actually working as intended in day-to-day operations?

Throughout this process, auditors document all testing activities, including any weaknesses or control gaps they find. Identified issues must be addressed promptly to reduce risk.

Finally, the testing results and remediation progress are regularly communicated to your management, executive leadership, and key stakeholders. This transparency helps ensure your control environment remains strong, risks are minimized, and your business objectives stay on track.

Also Read: Effective Audit Risk Assessment for Financial Firms

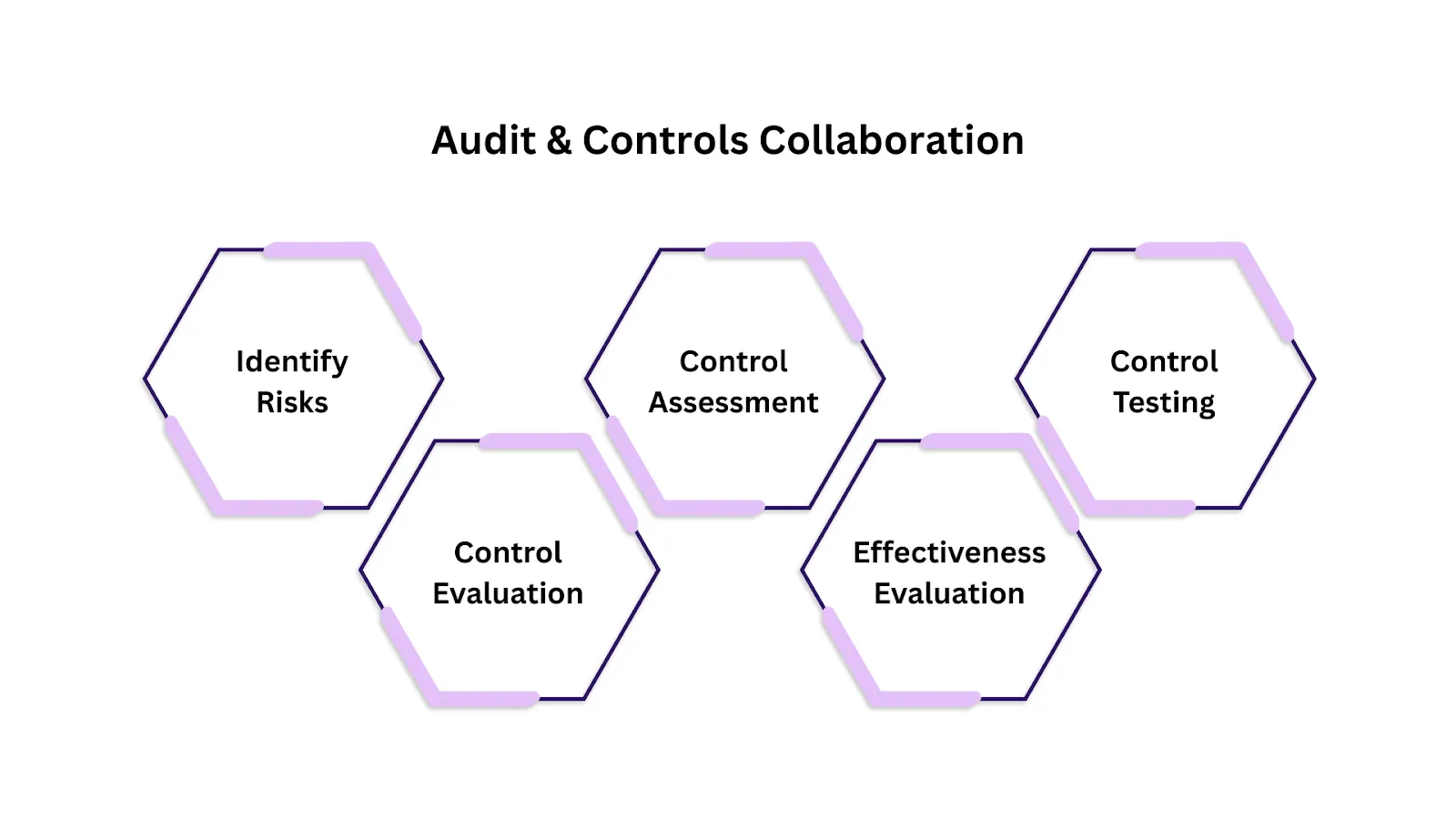

How Audit Procedures and Internal Controls Work Together

Let’s consider a growing fintech company that handles digital payments. An audit helps ensure their internal controls around transaction compliance and fraud prevention are working effectively to protect customer funds and meet regulatory requirements.

Identify Key Risks

Action: The company begins by assessing risks related to payment processing, such as fraudulent transactions, money laundering, system errors, and regulatory non-compliance.

Outcome: They develop a detailed list of risks that could impact transaction integrity and compliance with laws like AML (Anti-Money Laundering).

Evaluate the Control Design

Action: Next, the company reviews how their controls are designed to address these risks. This includes transaction monitoring systems, KYC (Know Your Customer) verification processes, approval workflows for large transfers, and secure data handling policies.

Outcome: They gain insight into whether these controls are properly structured—for example, whether automated fraud detection tools and manual approval steps are in place and appropriately scoped.

Test Control Implementation

Action: Auditors then carry out procedures such as inspecting transaction logs, observing compliance teams in action, and reperformance by independently testing transaction approvals and monitoring alerts.

Outcome: They gather proof that the controls are actually being used as intended, confirming, for instance, that alerts are generated for suspicious transactions and KYC checks are consistently completed.

Assess Control Effectiveness

Action: Using data analytics and trend analysis, auditors assess whether these controls are truly effective at minimizing risks. This involves reviewing past incidents, false positives/negatives in fraud detection, and regulatory findings.

Outcome: The company understands which controls are working well and which areas require strengthening—for example, finding that some fraudulent activities still slip through, highlighting a need for enhanced machine learning models or staff training.

Fraxtional use AI to automatically surface financial anomalies as they happen. This real-time insight allows teams to investigate irregularities before they escalate, improving audit readiness and enabling a more proactive compliance approach. In turn, this builds trust with both auditors and stakeholders.

Report Findings and Recommendations

Action: Finally, auditors compile their findings and present recommendations, including follow-up inquiries with compliance officers and leadership to discuss implementation challenges.

Outcome: The company receives a clear report detailing control gaps and actionable steps, such as improving transaction monitoring rules, updating KYC policies, or increasing ongoing employee compliance training.

How Fraxtional Can Help Simplify Your Internal Controls and Audit Procedures

Understanding the complexities of internal controls and audit procedures can be challenging, particularly in fast-paced, highly regulated industries such as fintech and financial services. That’s where Fraxtional steps in as a trusted partner.

Fraxtional offers cutting-edge, AI-driven solutions to streamline your compliance and audit processes. From automated risk assessments to real-time monitoring and intelligent audit workflows, Fraxtional helps you:

- Strengthen your internal controls with continuous, data-backed insights

- Simplify audit preparation with efficient evidence collection and documentation

- Identify and mitigate risks proactively before they become costly issues

- Ensure regulatory compliance with automated updates on changing laws and standards

- Empower your teams with intuitive tools that reduce manual effort and human error

With Fraxtional, you gain a comprehensive, scalable platform designed to keep your organization secure, compliant, and audit-ready, so you can focus on growing your business with confidence.

Conclusion

Strong internal controls and robust audit procedures are the backbone of any well-governed organization. They protect your assets, ensure accurate reporting, promote accountability, and support compliance—all while helping your business operate efficiently and with integrity.

By understanding how to design, test, and monitor these controls effectively, you reduce the risk of fraud, errors, and regulatory penalties. By choosing the right audit procedures tailored to your goals, you can get a clearer, more actionable view of your company’s risk landscape.

If you’re ready to build or enhance your internal control framework and make audits less daunting and more insightful, partnering with the right technology and expertise is key.

Explore how Fraxtional can help you transform your compliance and audit processes, making risk management smarter, faster, and more reliable.

Next Read: How to Create an Effective Compliance Program: Key Steps & Best Practices

FAQs

Internal controls are the policies and processes your organization uses to manage risks and ensure compliance. Audit procedures are the methods auditors use to test and evaluate whether those controls are working effectively.

Internal controls should be reviewed regularly, at least annually, and whenever there are significant changes in operations, regulations, or technology to ensure they remain effective and relevant.

No. Internal audits help your organization monitor and improve controls continuously, while external audits provide an independent, objective assessment required by regulators or stakeholders.

Automation reduces manual errors, speeds up evidence collection, enables real-time monitoring, and ensures audit trails are complete, making compliance and audits more efficient and accurate.

Weak controls increase the risk of fraud, financial misstatements, regulatory penalties, and operational inefficiencies, which can harm your organization’s reputation and financial health.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.

Now Accepting:

BTC

ETH

USDC

USDP