Mar 9, 2026

Prepare for the 2026 Nacha Rules Changes: What You Need to Know

By Fraxtional LLC

Summarize the blog with AI

The 2026 Nacha rule changes are set to redefine the way businesses handle ACH transactions, addressing growing fraud risks in the process. These updates are crucial for ensuring the security of electronic payments and reducing operational risks. Without proper preparation, businesses may face compliance challenges and penalties.

Nacha, the governing body of the ACH network, sets the rules that all participants must follow to ensure secure and efficient payment processing. As the ACH network continues to grow, Nacha's role in safeguarding the payment system becomes increasingly important.

This article will outline the key changes to the Nacha rules for 2026, highlight their impact on businesses, and provide actionable steps to prepare.

Quick look

- 2026 Nacha rules introduce stronger fraud monitoring requirements, requiring ACH participants to implement risk-based processes to detect suspicious or unauthorized transactions.

- Two implementation phases begin in March and June 2026, first applying to high-volume originators and service providers and later extending across the ACH network.

- New Company Entry Description standards require businesses to use labels such as PAYROLL for wage payments and PURCHASE for e-commerce transactions.

- International ACH Transaction (IAT) rules are expanding, improving identification and monitoring of payments involving financial institutions outside the United States.

- Organizations preparing for these updates often work with firms like Fraxtional to bring experienced compliance leadership that helps align ACH operations with Nacha requirements.

Which Transactions Are Covered Under the Nacha Rules?

The Nacha Operating Rules govern all transactions processed through the Automated Clearing House (ACH) Network. These rules define how payments are initiated, transmitted, settled, and monitored across financial institutions in the United States.

ACH transactions are categorized using Standard Entry Class (SEC) codes, which indicate the type of payment and how authorization was obtained. These classifications determine which specific Nacha operating rules apply to each transaction.

Common ACH transaction types include:

- PPD (Prearranged Payment and Deposit): Used for recurring or one-time consumer payments such as payroll deposits, insurance premiums, and loan payments authorized in writing.

- WEB (Internet-Initiated Entries): Used for online payments and e-commerce transactions authorized through a website or digital interface.

- TEL (Telephone-Initiated Entries): Payments authorized via telephone instructions, typically used for call-center initiated transactions.

- CCD (Corporate Credit or Debit): Used for business-to-business payments, including vendor payments and corporate fund transfers.

- IAT (International ACH Transactions): Used when a payment involves a financial institution outside the United States, requiring additional data elements for regulatory monitoring.

Each SEC code comes with specific operating rules for authorization, fraud monitoring, and data requirements. The 2026 Nacha rule updates primarily strengthen fraud detection expectations across these ACH transaction types, especially for organizations initiating large transaction volumes.

With this context in place, let’s look at the specific updates introduced in the 2026 Nacha rules.

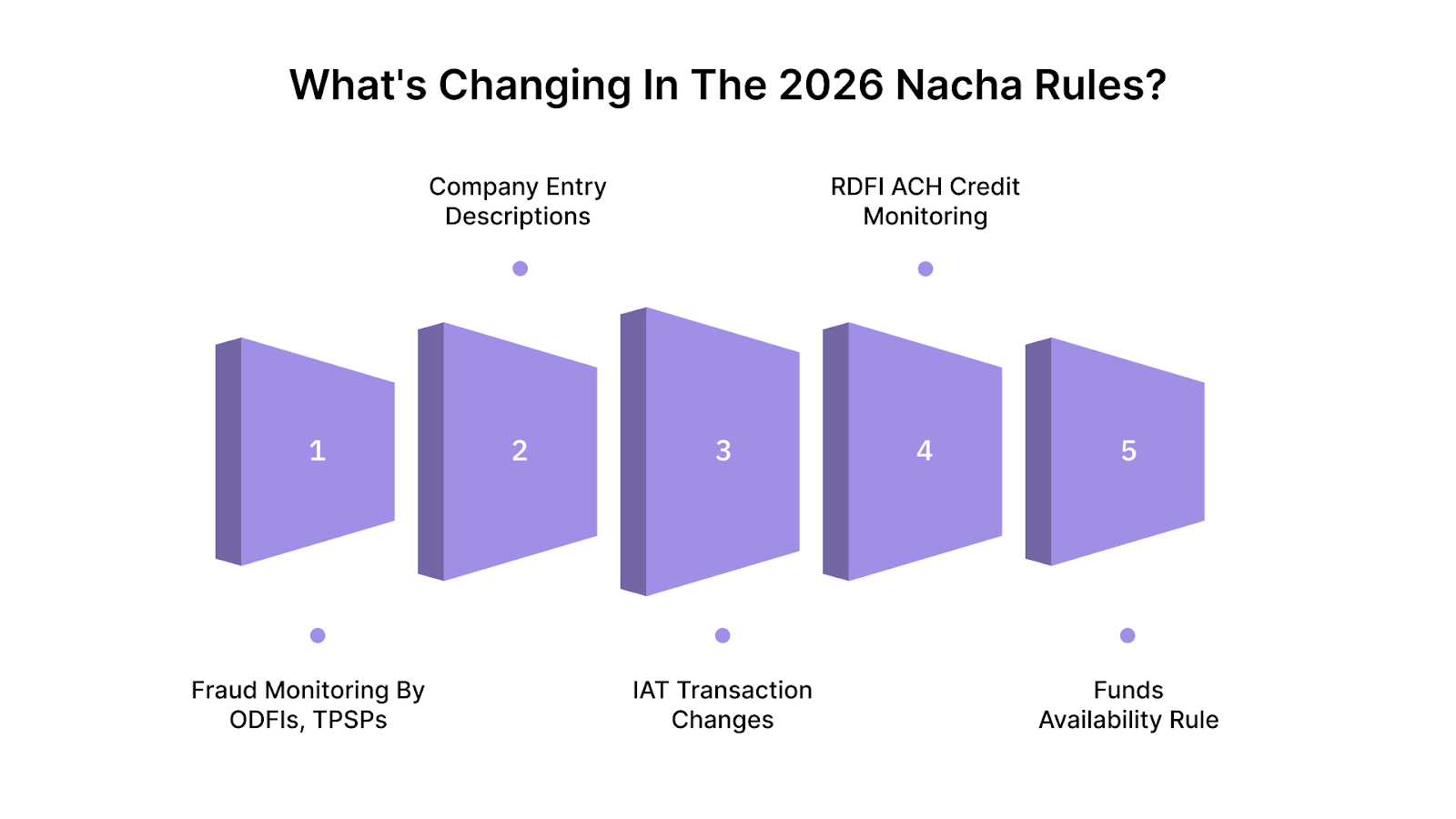

What's Changing in the 2026 Nacha Rules?

The 2026 Nacha rules bring important updates aimed at strengthening fraud prevention and improving the security of ACH transactions. Below are the key updates that businesses need to focus on:

1. Fraud Monitoring by ODFIs, TPSPs, and Non-Consumer Originators

Phase 1 (Effective March 20, 2026):

Non-consumer Originators and Third-Party Service Providers with an annual ACH origination volume of 6 million or more in 2023 must establish risk-based fraud monitoring processes.

Phase 2 (Effective June 22, 2026):

This will apply to all ODFIs and Originators who did not meet the Phase 1 threshold. These entities must implement risk-based processes and procedures to identify and mitigate fraudulent ACH entries.

2. Company Entry Descriptions: PAYROLL and PURCHASE

Effective March 20, 2026:

The use of PAYROLL and PURCHASE company entry descriptions will be standardized for certain types of ACH transactions:

- PAYROLL for salary and wage payments.

- PURCHASE for e-commerce authorized online, typically using the WEB debit SEC code.

This change ensures clarity and reduces the risk of misclassified transactions in the ACH system.

3. IAT Transaction Changes

Effective September 18, 2026:

The definition of International ACH Transactions (IAT) will be updated to ensure all international payments are properly classified and tracked. IATs will now include transactions that originate or are received from a financial institution outside the U.S.

These changes will enhance transparency and facilitate more effective monitoring of international payments.

4. RDFI ACH Credit Monitoring

Effective March 20, 2026 (Phase 1) and June 22, 2026 (Phase 2):

RDFIs with annual ACH receipt volumes of 10 million or more in 2023 will need to implement risk-based fraud monitoring systems to detect unauthorized credit entries.

5. Funds Availability Rule

Effective September 18, 2026

- RDFIs must make funds from non-Same Day ACH credits available by 9:00 AM local time on settlement date, eliminating the earlier 5:00 PM condition.

These changes will require businesses and financial institutions to adjust their existing systems and processes to meet new fraud detection and monitoring requirements.

With these critical changes outlined, let's now explore how these updates will specifically impact your business and the steps you can take to ensure compliance.

Which Organizations Are Impacted by the 2026 Nacha Rules

The 2026 Nacha rules impact a wide range of ACH network participants:

- Non-consumer originators: Any business initiating ACH transactions (e.g., payroll, vendor payments).

- ODFIs (Originating Depository Financial Institutions): Institutions that process and transmit ACH payments.

- RDFIs (Receiving Depository Financial Institutions): Institutions that receive ACH payments on behalf of their customers.

- Third-party service providers (TPSPs): Companies that provide ACH processing services to businesses.

These entities must implement the necessary fraud detection processes and adjust their internal policies to comply with the new regulations.

As businesses and institutions prepare for these changes, it's crucial to understand the impact these updates will have on your operations.

Let’s now look into how these new rules will specifically affect your business and what steps you need to take to stay compliant.

How the 2026 Nacha Rules Impact Your Business

The 2026 Nacha rules will significantly change how businesses involved in ACH transactions operate. From fraud prevention to transaction reporting, several key areas will see major shifts:

1. Increased Compliance Burden

- Businesses will need to establish strong fraud detection and risk-based monitoring systems.

- Existing systems may need to be upgraded or restructured to meet new compliance standards.

2. Enhanced Security Measures

- The standardization of company entry descriptions (e.g., PAYROLL and PURCHASE) helps streamline ACH transactions and reduce errors.

- Financial institutions will need to ensure their systems are capable of handling the increased volume of ACH transactions and fraud detection tasks.

3. New Reporting Obligations

Organizations must ensure proper documentation and annual reviews of their fraud prevention processes, especially for entities impacted by Phase 1 and Phase 2.

With these impacts in mind, it’s crucial for businesses to start planning their compliance strategy.

For organizations managing ACH payments at scale, regulatory updates like these often require specialized compliance leadership. Fraxtional provides compliance experts who help fintech companies, banks, and payment providers strengthen risk monitoring, update policies, and align operations with changing Nacha rules.

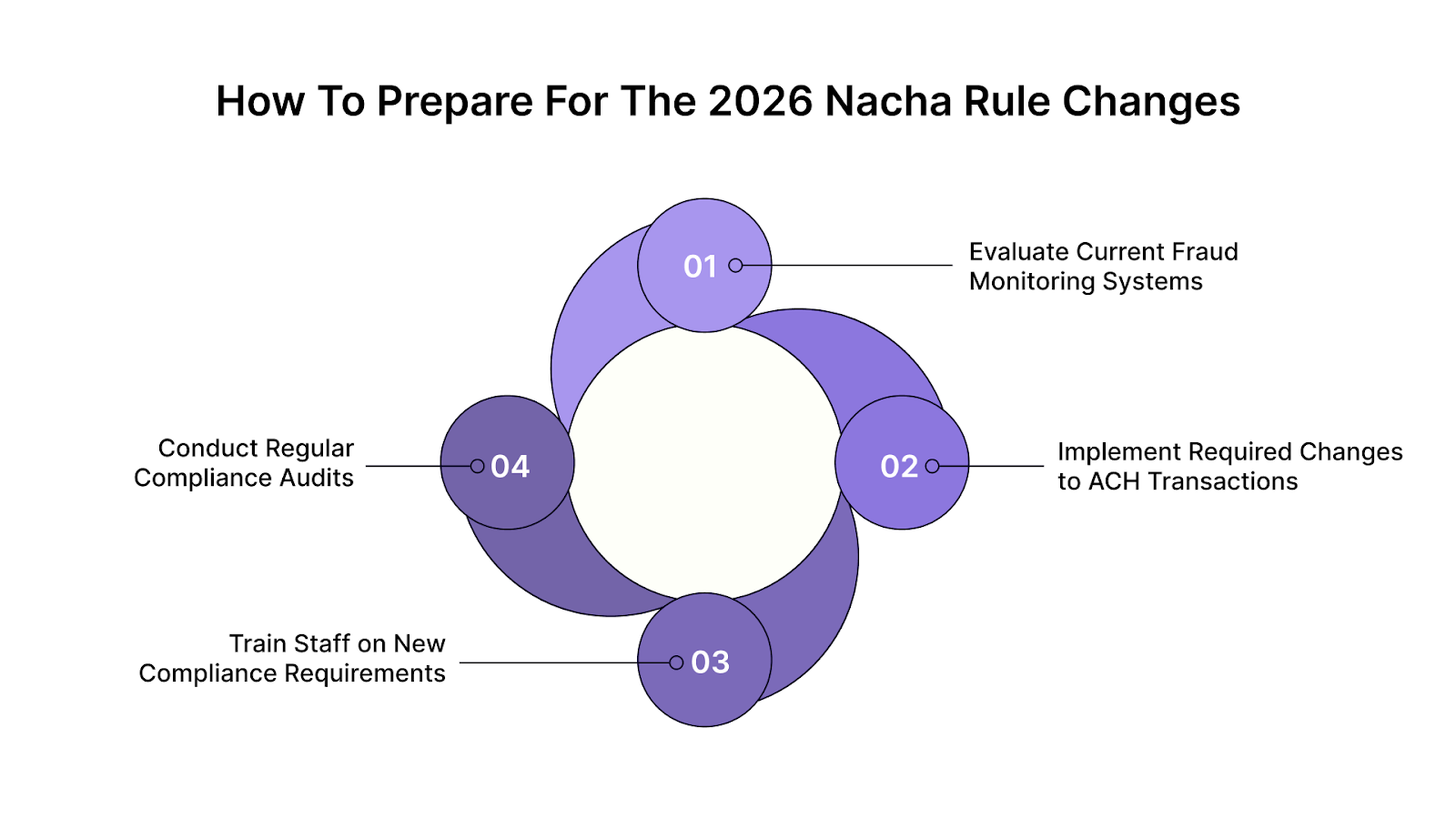

How to Prepare for the 2026 Nacha Rule Changes

Businesses that originate or process ACH payments should begin preparing well before the 2026 deadlines. The following steps can help organizations align their systems and procedures with the new Nacha requirements.

Step 1: Evaluate Current Fraud Monitoring Systems

- Review existing fraud detection systems for gaps, especially in anomaly detection and risk-based monitoring.

- If missing, implement real-time fraud detection tools capable of flagging atypical transactions and account changes.

- Ensure your systems can comply with Phase 1 and Phase 2 requirements, including setting up automated alerts for high-risk transactions.

Step 2: Implement Required Changes to ACH Transactions

- Standardize Company Entry Descriptions: Ensure “PAYROLL” for wage payments and “PURCHASE” for e-commerce transactions in the Company Entry Description field.

- Update systems to classify International ACH Transactions (IATs) according to the new rules by September 2026. Ensure proper codes for international senders and receivers.

Step 3: Train Staff on New Compliance Requirements

- Train teams on fraud detection, the use of “PAYROLL” and “PURCHASE” descriptions, and IAT rules for international transactions.

- Conduct annual refresher training to ensure ongoing compliance with the 2026 Nacha updates.

Step 4: Conduct Regular Compliance Audits

- Perform a gap analysis to identify areas that need updating for the new Nacha fraud monitoring rules.

- Schedule quarterly compliance audits to track the effectiveness of your fraud detection systems and keep documentation updated.

As businesses take these critical steps to prepare for the 2026 Nacha rule changes, partnering with the right compliance expert can help ensure a seamless transition.

Let’s now explore how Fraxtional’s expertise can guide your organization through the process and ensure ongoing compliance.

Ensuring Compliance with the 2026 Nacha Rules Through Fraxtional’s Expertise

Fraxtional specializes in providing fractional compliance leadership and regulatory support to businesses managing the complexities of ACH transactions and fraud prevention.

With years of experience in financial services, fintech, and banking, Fraxtional helps organizations stay ahead of the 2026 Nacha rule changes, ensuring smooth transitions and compliance.

Here’s how Fraxtional can assist in meeting the 2026 Nacha rules:

- Fractional Compliance Leadership: Access experienced senior compliance leaders like CCOs, CROs, and AML Officers on a part-time basis, personalized to your business needs and compliance requirements.

- Regulatory Readiness: Receive strategic advice and support to prepare for the 2026 Nacha updates, ensuring your fraud monitoring and ACH transaction systems are fully compliant.

- Ongoing Compliance Support: Ensure continuous adherence to the 2026 Nacha rules with regular audits and updates, helping you stay compliant as regulations grow.

With Fraxtional’s expertise, your business can navigate the 2026 Nacha rule changes confidently and stay ahead of compliance risks.

Wrapping Up

The 2026 Nacha rule changes require businesses to strengthen fraud monitoring, update ACH transaction procedures, and comply with new entry descriptions. Preparing now will help ensure smooth transitions and avoid penalties.

Fraxtional offers fractional compliance leadership and expert guidance to help businesses meet the new regulations. The team offers strategic support and compliance solutions tailored to your needs.

To ensure seamless compliance with the 2026 Nacha rules, reach out to Fraxtional for expert guidance and personalized solutions today.

FAQs

No. The Nacha 2026 operating rules do not mandate data sharing or participation in fraud consortiums. Institutions may choose to use privacy‑preserving fraud intelligence tools as long as they protect customer data and meet risk‑based control expectations.

A false-pretense payment is an ACH payment that appears authorized but was initiated under deceptive circumstances, such as impersonation or social engineering. The 2026 rules explicitly address this category to strengthen fraud detection.

No specific vendors or technologies are mandated. However, organizations must demonstrate that their controls are risk‑based, documented, and effective in detecting fraud, often requiring modern monitoring platforms rather than manual methods.

While the blog covers the need to prepare, it's worth noting that Nacha enforces its rules through fines, warnings, and escalation, including potential suspension of ACH origination privileges for serious or repeated violations.

The updates were designed to address rising fraud risks in ACH transactions, especially for credit‑push and false‑pretense fraud, expanding traditional fraud controls to be more proactive and risk‑based across the ACH network.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.