Dec 8, 2025

How to Prepare for a PCI Audit: Expert Tips for 2026

By Fraxtional LLC

Summarize the blog with AI

Only 14.3% of organizations maintain full PCI DSS compliance. This statistic should worry you if you're in a sector like FinTech, Crypto, or Private Equity, where data security is non-negotiable. Many businesses struggle to stay compliant, facing challenges that can disrupt operations and jeopardize their reputation.

The PCI audit process is complex, and the stakes are high. With increasing regulatory scrutiny and customer expectations, it can feel like a constant battle to stay ahead. From securing sensitive data to managing third-party risks, there’s a lot to address, and it's easy to miss key steps.

In this blog, we’ll explore how to prepare for a PCI audit, what to expect during the process, and strategies for ongoing compliance. We’ll also cover common pitfalls and provide actionable tips to keep your business secure and compliant long after the audit is complete.

TL;DR

- A PCI audit ensures your business complies with PCI DSS standards to protect payment card data and avoid penalties.

- Key compliance requirements include network security, encryption, access control, malware protection, and secure system development.

- To prepare, define your cardholder data environment, conduct a gap analysis, gather necessary documentation, and engage a certified assessor.

- Failing a PCI audit can result in fines, loss of card acceptance, increased fees, and reputational damage.

- Ongoing compliance involves regular risk assessments, continuous monitoring, and vendor management to stay secure year-round.

What is a PCI Audit?

A PCI audit is a thorough review of your business’s compliance with the Payment Card Industry Data Security Standard (PCI DSS). This audit assesses how well your company handles payment card data, ensuring that all required security measures are in place.

It involves checking that your systems and processes meet specific requirements designed to protect sensitive customer information. The audit examines various areas, including access controls, encryption, and vulnerability management, to confirm that your organization reduces risks to payment card data.

For most businesses, completing a PCI audit is mandatory if they process, store, or transmit payment card information. As of March 31, 2025, all future‑dated requirements of PCI DSS v4.0 will become mandatory. Without passing the audit, your company may face fines, increased scrutiny, or even lose the ability to process payments.

With a clear understanding of the PCI audit, let’s explore the specific requirements that ensure your compliance.

Also Read: Effective Audit Risk Assessment for Financial Firms

Essential PCI DSS Compliance Requirements for 2026

The PCI DSS defines a set of requirements designed to protect cardholder data and payment‑card processes comprehensively. These requirements apply across businesses that process, store, or transmit payment card information, supporting audit readiness and ongoing security controls.

Below are the core requirements your business should address:

- Network Security: Install and maintain network security controls, including firewalls and routers, to protect the cardholder data environment.

- System Configuration Security: Apply secure configurations to all system components, avoiding vendor defaults and hardening access settings.

- Data Protection: Protect stored account and cardholder data using appropriate encryption, masking, or controls to limit exposure.

- Encryption for Data Transmission: Encrypt cardholder data when transmitted over open, public networks to guard against interception or compromise.

- Malware Protection: Protect all systems and networks from malicious software by applying anti-malware controls and regular patching.

- Secure System Development: Develop and maintain secure systems and software, including implementing updates and addressing known vulnerabilities.

- Access Control: Restrict access to system components and cardholder data based on business need to know, and enforce least-privilege access.

- User Authentication: Identify users and authenticate access to system components, including enforcing multi-factor authentication where required.

- Physical Security: Restrict physical access to cardholder data and system components to prevent unauthorized access or misuse.

- Logging and Monitoring: Log and monitor all access to system components and cardholder data; conduct regular review of logs and alerts.

- Regular Testing: Test security systems and networks regularly, including penetration testing and vulnerability scanning at defined intervals.

- Information Security Program: Maintain an information security policy and program to address governance, risk management, and compliance oversight.

With these key requirements in mind, let’s explore how to effectively prepare for and manage the audit process.

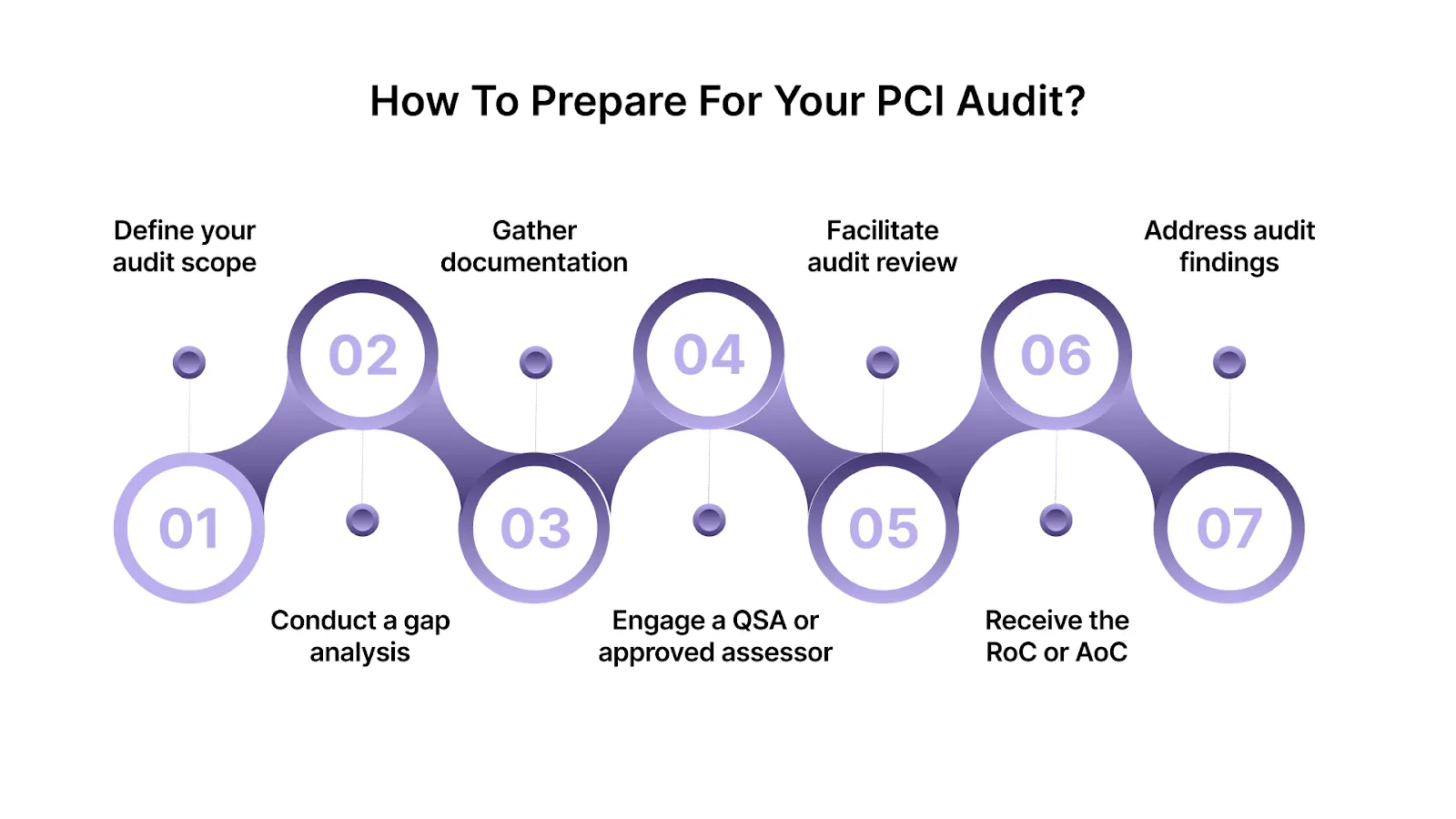

How to Prepare for Your PCI Audit: A Step-by-Step Guide

The audit process starts when an organization accepts that payment card data flows through its systems and must be secured and verified. Preparing for a PCI audit means mapping your cardholder data environment, aligning your controls with required standards, and securing documented evidence of processes.

A well‑planned audit journey reduces surprises and strengthens confidence in audit outcomes for business and investor stakeholders.

Below are key practical steps to guide your team through audit readiness and execution:

- Define and confirm your audit scope

Work with your payment team, IT, and compliance experts to identify every system, network, and process that stores, processes or transmits cardholder data.

- Conduct a gap analysis and remediation plan

Identify missing or weak controls compared to the PCI DSS requirements and create a roadmap to address these issues before the formal audit begins.

- Gather documentation and evidence of controls

Collect network diagrams, policy and procedure records, access logs, vulnerability scan results, and third-party vendor lists ahead of the auditor’s review.

- Engage a Qualified Security Assessor (QSA) or approved assessor early

For entities that require formal audits rather than self‑assessment, selecting a certified QSA ensures correct protocol, scope validation, and credible audit output.

- Facilitate the on‑site or remote audit review

During audit execution the assessor will test controls, interview staff, review configurations and verify evidence of compliance in your cardholder data environment.

- Receive the Report on Compliance (RoC) or Attestation of Compliance (AoC)

Once testing is complete your organization will receive formal documentation that reflects compliance status and identifies any remaining gaps.

- Address audit findings and integrate continuous compliance practices

Even after the audit completes, closing identified gaps and maintaining controls throughout the year helps ensure readiness for the next audit cycle.

Our expert team can perform a comprehensive audit, covering everything from control effectiveness testing to documentation gap analysis and provide you with a prioritized remediation plan. Book your free consultation with Fraxtional today to get the clarity and support your business needs for seamless audit success.

Also Read: Internal Audit Checklist for Effective Financial Assessment & Control

While preparation is key, it’s also important to consider what could happen if you fail your PCI audit.

Consequences of Failing Your PCI Audit and How to Avoid Them

Failing your PCI audit can lead to major financial penalties enforced by your acquiring bank or card‑brand partners. Your ability to accept payment cards may be suspended until you correct the issues and achieve compliance again.

Beyond the audit itself, a failure can trigger legal claims, higher transaction fees, loss of partner trust, and reputational damage.

Below are key consequences your business may face:

- Monthly fines: Payment processors may impose penalties while non‑compliance continues, and fees can escalate depending on the length of time it takes to resolve the issues.

- Loss of card‑acceptance privileges: Your merchant account could be terminated or suspended, preventing you from processing credit/debit card transactions.

- Increased transaction costs: Your acquiring bank might raise interchange or service fees, making every card transaction cost you more.

- Legal and breach liabilities: A non‑compliance finding, especially paired with a breach—can lead to lawsuits, regulatory investigations, and breach recovery costs.

- Damage to reputation and partner relationships: Clients, investors, and partners may lose confidence in your ability to protect payment data, affecting growth and contracts.

- Operational disruption: Being placed on payments industry blacklists (such as MATCH or TMF lists) can restrict business opportunities and vendor relationships.

Let Fraxtional’s experienced executives take the lead on your compliance program. Contact us to learn more about our flexible leadership solutions.

Proven Tips for Ongoing PCI Compliance and Data Protection

Maintaining PCI compliance requires ongoing oversight and regular review to protect cardholder data and support business continuity. Establishing structured monitoring workflows helps you spot and address deviations from standards early.

Here are practical actions to support ongoing monitoring and control of PCI compliance:

- Assign a Compliance Lead:

Appoint a part‑time expert executive or fraxtional CRO consulting services to ensure accountability for control effectiveness and ongoing compliance across your business.

- Conduct Regular Risk Assessments:

Regularly conduct risk assessment services to evaluate your systems, payment flows, third-party access, and regulatory changes, identifying emerging vulnerabilities before the next audit.

- Implement Continuous Monitoring:

Collect comprehensive logs, enforce daily or near‑daily reviews, retain at least one year of audit history, and act on anomalies promptly.

- Monitor Third-Party Vendors:

Ensure all outsourced service providers, sponsor bank partner services, and money transmitter licensing relationships adhere to contractual compliance, undergo regular audits, and provide vendor reports.

- Align with Broader Frameworks:

Integrating your cardholder data protections with anti‑money‑laundering services and SOC2 controls creates a unified assurance platform for investors and regulators alike.

- Update Policies and Training:

Review your security policies, conduct training for relevant staff, refresh incident response plans, and document changes so your control environment remains current.

- Track and Report Key Metrics:

Tracking metrics such as access violations, patch latency, vendor audit completion, and audit‑finding closure rates provides transparency and helps you build trust with investors and auditors.

Following these steps helps maintain compliance between formal audits, reducing risk exposure and supporting your business’s readiness, regulatory posture, and investor assurance.

Conclusion

Achieving and maintaining PCI compliance is not a one-time event; it requires continuous effort and vigilance. By staying ahead of the audit process, addressing gaps, and monitoring security measures consistently, you ensure the protection of both customer data and your business reputation. With the right preparation, you can navigate the complexities of compliance without disruption.

At Fraxtional, we offer expert compliance leadership to help guide your business through PCI audits and maintain ongoing compliance. Contact us today to learn how we can support your business’s security and compliance needs.

FAQs

PCI compliance has four levels based on annual transaction volume. Level 1 applies to businesses processing over 6 million transactions, while Level 4 is for those with fewer than 20,000. Each level has distinct audit requirements.

A PCI compliance checklist outlines the key requirements businesses must meet to comply with PCI DSS standards. It helps identify gaps in areas like encryption, network security, and access control.

There are two types of PCI compliance: Self-Assessment for smaller merchants and External Audit for larger businesses or those with higher transaction volumes. Both involve verifying compliance with PCI DSS standards.

PCI approval is the certification granted to businesses that meet PCI DSS compliance standards. It’s awarded after a successful audit or self-assessment.

Yes, third-party vendors that handle cardholder data must also be PCI compliant. Failure to ensure their compliance can affect your business’s PCI status. Always verify vendor compliance before engaging them.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.