Feb 13, 2026

Guide to Transaction Monitoring in AML: What Regulators and Sponsor Banks Expect

By Fraxtional LLC

Summarize the blog with AI

You can build strong products and secure sponsor bank partnerships, but ineffective AML transaction monitoring can still stall you by missing real risk while flooding your team with useless alerts. This is one of those compliance headaches no one talks about until the day you’re explaining why your team is buried in false alerts while regulators and examiners are waiting for credible SAR narratives.

Bad alerts drown your compliance analysts, slow investigations, and cause genuine risks to slip through unnoticed, at exactly the moment your company is scaling product usage or entering new corridors. Recent research shows that traditional AML transaction monitoring systems generate very high false positive rates, leading to inefficiency and operational strain even for large financial institutions.

In this blog, we will explain what is transaction monitoring, why it matters to regulators and sponsor banks, how it works, and what separates compliance drama from compliance confidence.

Key Takeaways

- Transaction monitoring is an ongoing AML control that continuously tracks customer transactions to detect unusual or suspicious behavior, not just one-off checks.

- Regulators and sponsor banks focus on how effective and risk-aligned monitoring is, emphasizing documented oversight and timely SAR decisions rather than specific tools.

- Strong programs rely on senior compliance leadership, regular tuning, independent validation, and well-documented escalation and investigation processes.

- Rapid growth, new products, crypto exposure, or system changes often reveal monitoring gaps, making proactive adjustments essential to avoid missed risks or false positives.

- Fraxtional helps organizations integrate regulator-ready oversight, aligning monitoring and documentation to protect institutions and maintain sponsor bank confidence.

What Is Transaction Monitoring in AML

Transaction monitoring is where AML stops being theoretical and starts showing up in your day-to-day operations. It is the continuous review of customer transactions to spot behavior that looks unusual, inconsistent, or potentially suspicious based on risk. Not once. Not at onboarding. Every day, as money actually moves.

Here is how regulators think about it:

- Ongoing review of transactions, not periodic spot checks

- Behavior analysis across time, volume, velocity, and counterparties

- Alerts that are explainable, reviewable, and consistently escalated

- Clear linkage between alerts, investigations, and SAR decisions

This is why regulators view transaction monitoring as an operational control, not a policy exercise. A written AML policy means little if your monitoring does not surface real risk.

Also Read: How Fractional C-Suite Roles Are Reshaping Leadership in 2025

Understanding what transaction monitoring is lays the foundation for seeing why this ongoing oversight is essential for protecting financial institutions from risk and regulatory exposure.

Why Transaction Monitoring Is Critical for Financial Institutions

Transaction monitoring exists because risk does not announce itself upfront. It shows up quietly, over time, in how money actually moves through your systems. And once it is missed, the consequences surface fast.

Here is the real business impact behind the control:

- Detects illicit activity early by flagging patterns linked to money laundering, fraud, and misuse of financial products

- Protects regulatory standing by demonstrating active oversight, not passive policy compliance

- Reduces reputational exposure when issues arise, and regulators ask what you knew and when

- Safeguards partner relationships, especially with sponsor banks that carry downstream liability

Also Read: AI in Leadership: Embracing Innovation and Responsibility

To see why transaction monitoring matters so much, it helps to understand how these changed approaches function within real systems.

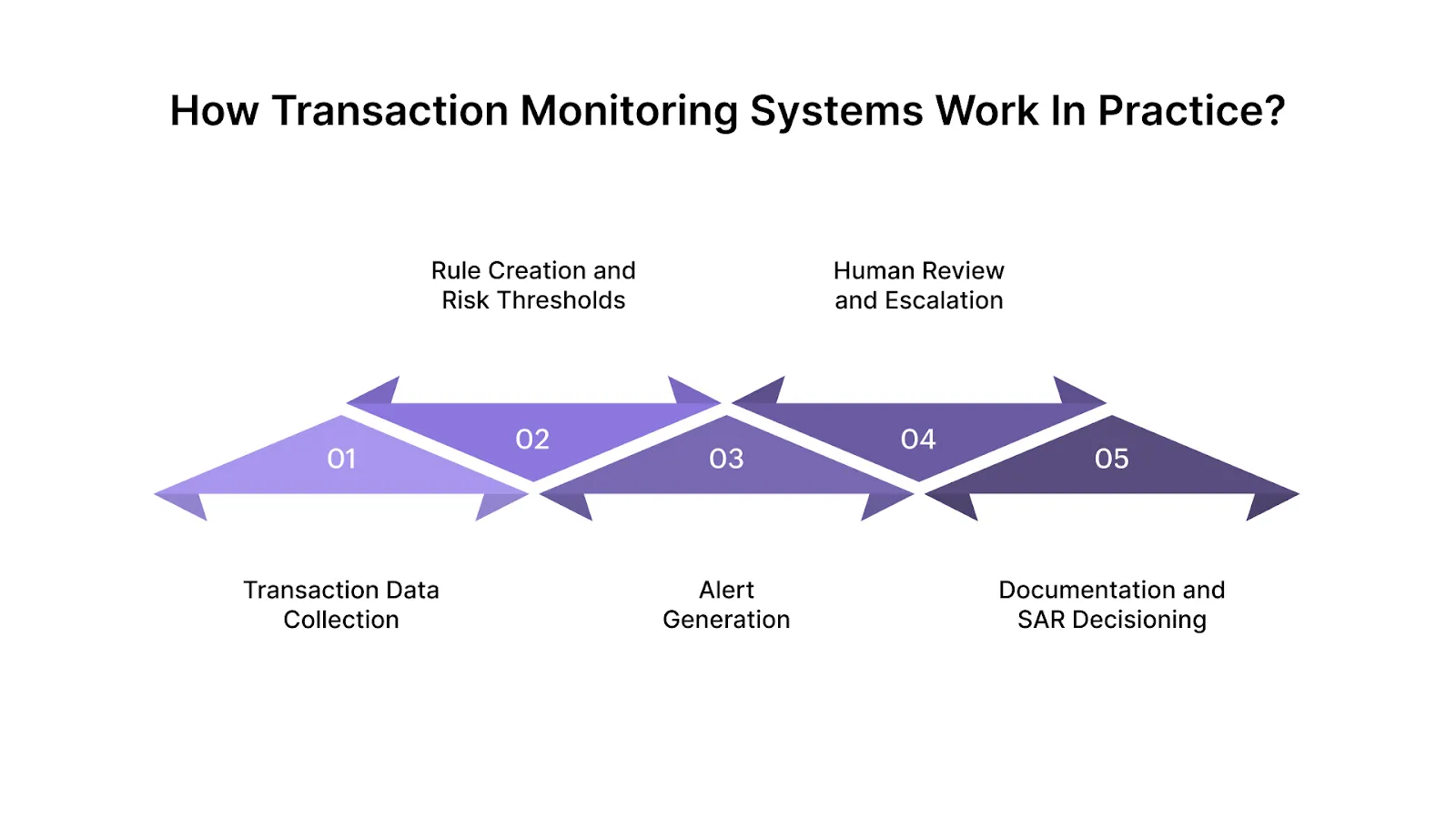

How Transaction Monitoring Systems Work in Practice

Behind every AML program that actually works is a cycle, from raw data flowing in to human decisions flowing out. Transaction monitoring systems tie together technology, rules, human review, and regulatory reporting so that suspicious activity doesn’t just sit in a queue; it gets acted on.

Here’s how that chain functions in reality:

- Transaction Data Collection: Systems ingest all relevant transaction data, transfers, deposits, withdrawals, payment flows, and related metadata from internal ledgers and external feeds. This continuous data stream forms the foundation of monitoring.

- Rule Creation and Risk Thresholds: Compliance teams establish rules and risk thresholds based on customer risk profiles, products, and behavior scenarios. These rules decide what counts as unusual. Many institutions now integrate behavior analytics and dynamic thresholds alongside static rules.

- Alert Generation: When transactions deviate from expected patterns or cross thresholds, the system generates alerts for further scrutiny. This step turns raw noise into actionable signals.

- Human Review and Escalation: Compliance analysts assess alerts to filter true positives from false alarms. They may escalate substantiated concerns to senior compliance or risk teams for deeper investigation.

- Documentation and SAR Decisioning: For cases that rise to suspicious activity, documented findings drive decisions on whether to file Suspicious Activity Reports (SARs) with regulators. Regulators emphasize the quality and consistency of these reports.

Why False Positives are Common: Traditional rule-based systems cast wide nets to avoid missing real threats, but this often catches lawful transactions as well, creating false positives that overload teams and drain resources.

Why Tuning and Oversight Matter More Than Tooling: Tools create alerts, but only well-tuned rules and disciplined human oversight turn those alerts into regulator-ready decisions. Effective systems change with risk, rather than simply generating noise.

Seeing transaction monitoring in action helps clarify why different monitoring models are needed.

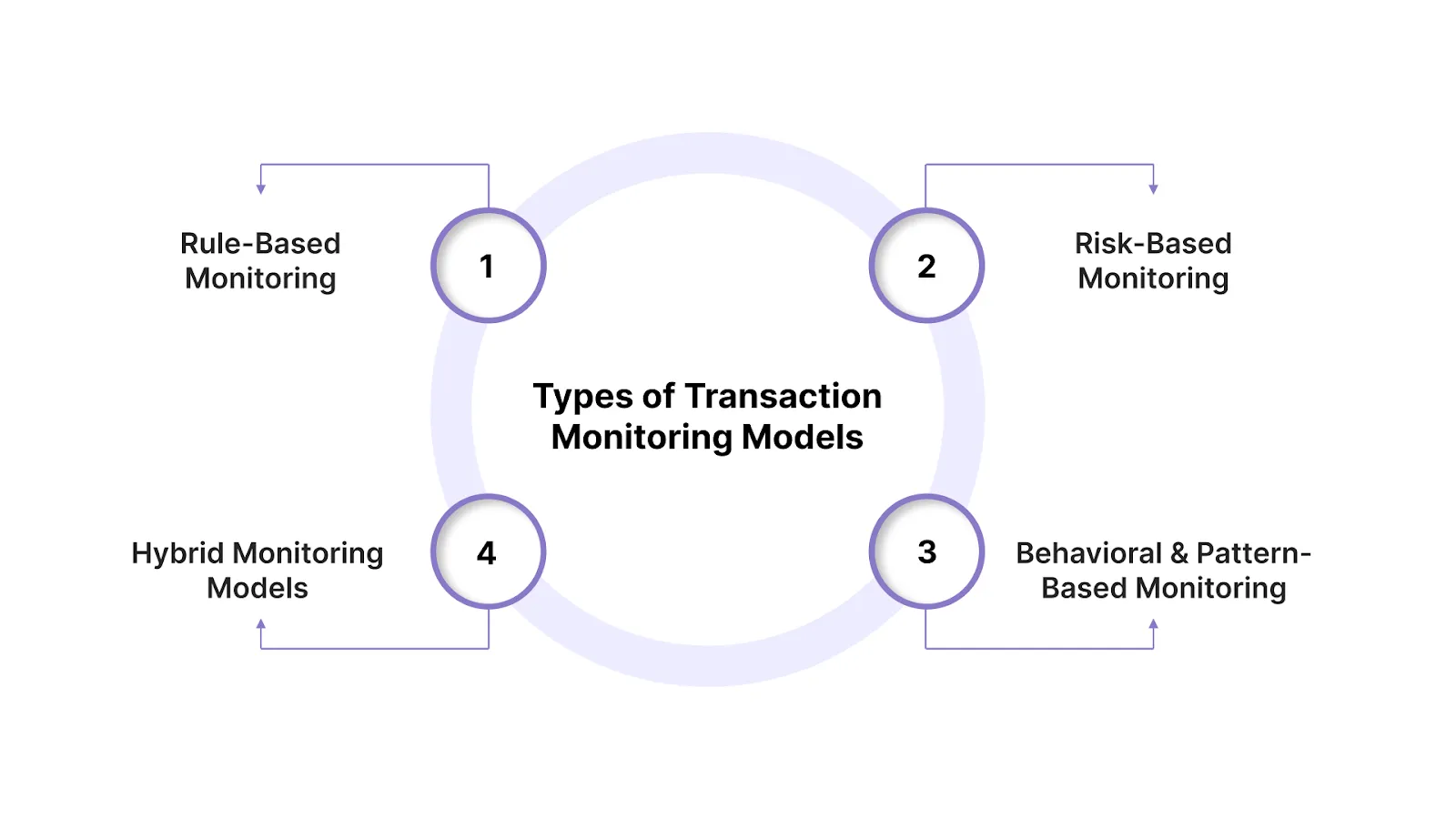

What Types of Transaction Monitoring Models Are Used Today

Transaction monitoring has matured beyond simple alerts; it now includes several distinct models that institutions use to spot suspicious activity in ways that fit their risk, data maturity, and operational capacity.

Here’s how the main models stack up:

- Rule-Based Monitoring

- Uses predefined rules and thresholds to flag activity (e.g., high-value transfers, frequent transactions).

- Easy to explain to auditors and regulators, but rigid and often generates many false positives.

- Risk-Based Monitoring

- Prioritizes alerts based on customer and transaction risk profiles.

- Allocates compliance effort where risk is highest, reducing noise and focusing scrutiny.

- Behavioral and Pattern-Based Monitoring

- Goes beyond static rules to watch how behavior changes over time.

- Uses analytics to understand normal patterns and spot anomalies that rules miss.

- Hybrid Monitoring Models

- Combines rule logic with analytics, machine learning, or anomaly detection to balance coverage and efficiency.

- Often prioritises or clusters alerts so investigators spend time on the most meaningful signals.

If your transaction monitoring creates more alerts than answers, that noise can quietly put sponsor bank relationships at risk. Fraxtional helps you turn monitoring into a risk signal regulators actually trust. Reach out to us to strengthen your compliance oversight before it becomes a growth blocker.

Knowing what transaction monitoring is across different models sets the stage for understanding how regulators evaluate its effectiveness.

What Regulators Look for When Assessing Transaction Monitoring

Regulators don’t judge your transaction monitoring program by brand name or tool choice; they judge it by effectiveness, risk alignment, and documented decision quality. When examiners or sponsor banks review your monitoring, they are essentially asking:

Does your monitoring actually find real risk, and can you prove it? Here’s how they see it.

- Alignment with Risk Assessment: Your monitoring must be directly informed by your risk assessment. If your risk profile says high-risk customers or products need extra scrutiny, your monitoring rules and thresholds should reflect that, not be generic. Regulators expect monitoring to follow your documented risk logic.

- Coverage of Products and Geographies: Transaction monitoring should encompass all relevant business lines, product types, and country exposures. Gaps here raise red flags because they create blind spots for illicit activity.

- Quality and Relevance of Alerts: Alerts must be meaningful. Too many false positives with no prioritization tells regulators you are generating noise, not insight. They want to see alerts tied to real risk scenarios and reviewed in a disciplined way.

- Quality of Documentation: Examiners want clear narratives: why this alert was raised, what steps were taken, and how final decisions were reached. Poor documentation is often where good monitoring fails audits.

Now, it’s important to understand how transaction monitoring operates specifically under U.S. regulations and what examiners expect from financial institutions.

Transaction Monitoring in the U.S. Regulatory Context

In the U.S., transaction monitoring isn’t a nice-to-have; it’s a legal expectation rooted in the Bank Secrecy Act (BSA). Regulators want to see that your monitoring actually helps detect, investigate, and report suspicious activity, not just produce dashboards.

Here’s how U.S. regulators think about it:

What the Bank Secrecy Act Requires

- Under the BSA, financial institutions must establish and maintain compliance programs that detect, monitor, and report suspicious activity, including maintaining transaction records and reporting transactions exceeding set thresholds to government authorities.

- Monitoring must be risk-based and ongoing so that institutions genuinely understand customer behavior and can identify unusual patterns.

SAR Filing Obligations Through FinCEN

- When your monitoring identifies activity that you know, suspect, or have reason to suspect could indicate money laundering or other illicit conduct, you are required to file a Suspicious Activity Report (SAR) with the Financial Crimes Enforcement Network.

- SARs generally must be filed within specified timeframes (e.g., within 30 calendar days of detection in many cases).

What Examiners Focus On

- Monitoring Design: Examiners expect your system to be tailored to your risk profile, including products, geographies, and customer segments, rather than cookie-cutter rules.

- Alert Handling: Alerts should be triaged, investigated, and documented with clear reasoning that links to risk indicators and escalation workflows.

- Sar Rationale and Timeliness: When a SAR is filed, the narrative should explain why the activity is suspicious and demonstrate a logical monitoring → investigation → SAR decision chain.

Also Read: Fractional CRO vs CFO: Key Differences in Risk Management

Examining the U.S. rules sets the stage for understanding approaches taken by regulators around the world.

How Other Global Regulators Approach Transaction Monitoring

Below, we explore how the UK, the EU, and global standards view monitoring, helping you anticipate what global examiners and partners will ask of you.

UK: Money Laundering Regulations 2017 (MLR 2017)

- Continuous monitoring, not limited to onboarding or periodic checks

- Align transactions with customer risk profiles, including the source of funds

- Focus resources on higher-risk relationships

- Document investigations and reporting for regulatory review

EU: PSD2 and AML/CFT Frameworks

- Real-time or near-real-time monitoring for fraud and suspicious activity

- Integrate monitoring with customer authentication and risk scoring

- Align AML monitoring with reporting obligations under EU directives

- Protect the payment ecosystem while ensuring compliance

Global: FATF Guidance

- Apply a risk-based approach proportional to ML/TF risk, not one-size-fits-all

- Continuously monitor transactions relative to risk profiles

- Update controls as risks, products, or customer behavior changes

- Ensure monitoring is dynamic, defensible, and evidence-based

While these global frameworks inform the wider regulatory scene, U.S. rules under the BSA and SAR obligations remain the primary benchmark for transaction monitoring expectations in many multinational fintech and banking relationships.

Now, understanding global expectations helps highlight the practical scenarios that often draw regulatory scrutiny.

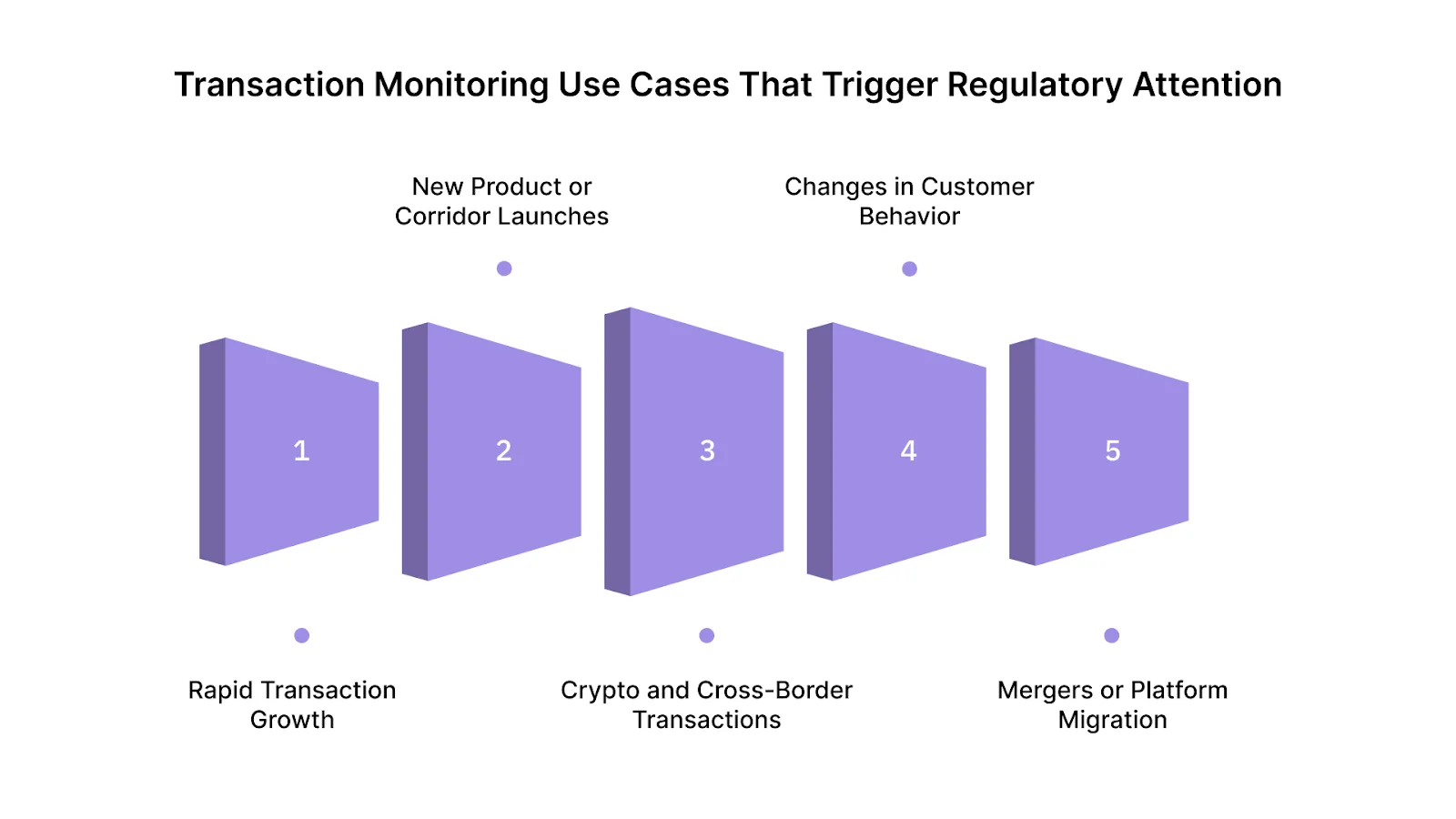

Common Transaction Monitoring Use Cases That Trigger Regulatory Attention

Certain business events can reveal gaps in transaction monitoring, attracting scrutiny from regulators and sponsor banks. Key scenarios include:

- Rapid Transaction Growth: Surges in volume can make old thresholds ineffective, creating anomalies that regulators expect you to manage.

- New Product or Corridor Launches: Expanding products or markets changes risk profiles, exposing blind spots if monitoring isn’t updated.

- Crypto and Cross-Border Transactions: Virtual assets, mixers, and high-risk jurisdictions require extra scrutiny beyond basic rules.

- Changes in Customer Behavior: Unusual activity from long-standing customers must be detected, investigated, and documented.

- Mergers or Platform Migrations: System transitions can disrupt monitoring and alert logic, highlighting coverage gaps.

Recognizing the high-risk scenarios makes it clear why many organizations struggle to keep monitoring both effective and manageable.

What Challenges Organizations Face With Transaction Monitoring

Here are the common challenges and practical fixes that experienced compliance leaders rely on:

- Alert Overload and Reviewer Fatigue: Compliance systems often generate too many alerts, many of which turn out to be harmless, because rules cast wide nets to avoid missing real risk.

- Fix: Prioritize alerts using risk-based scoring, refine rules regularly, and introduce tiered escalation so only meaningful signals reach senior reviewers.

- Poor Data Quality: Inaccurate, incomplete, or inconsistent transaction and customer data weakens monitoring logic, increases false positives, and undermines decision quality.

- Fix: Strengthen data governance with standardized formats, regular cleansing, and real-time integration across systems.

- Inherited Vendor Configurations: Legacy vendor settings rarely fit your risk profile and often accumulate “factory defaults” that weren’t tuned for your business.

- Fix: Reevaluate configurations with your risk assessment, remove irrelevant rules, and adjust thresholds to your product portfolio.

- Inconsistent Escalation Logic: Without clear escalation criteria, similar alerts get different treatments, and SAR decisions lack defensible consistency.

- Fix: Build documented escalation paths with decision trees tied to risk tiers and SAR criteria.

Many teams know what regulators expect but struggle to implement it consistently with limited senior oversight. Fraxtional provides compliance leadership to align monitoring, governance, and documentation with regulatory standards. Contact us to partner on building a regulator-ready program.

Understanding these common challenges helps frame why regulators and sponsor banks place such emphasis on clear, well-executed best practices.

Best Practices Regulators and Sponsor Banks Expect to See

Below are the key practices that indicate a program is functioning as intended:

- Monitoring Tied Directly to Risk Assessment: Monitoring logic should flow directly from your documented risk assessment. High-risk customers, products, and geographies should receive proportionate oversight, and your alerting logic should reflect that prioritization.

- Clear and Documented Rule Logic: Rules should be documented so that their purpose, parameters, and expected outcomes are clear to regulators. This allows examiners to understand why certain alerts are generated and how they relate to your specific risk scene.

- Regular Tuning and Validation: Static rules become stale quickly. Validators should regularly adjust thresholds and scenarios based on emerging trends, internal risk shifts, and external typologies.

- Independent Testing and Review: Periodic independent testing, internal audit, or third-party review shows that oversight extends beyond operations and ensures your program is performing effectively, and not just existing on paper.

- Senior Leadership Oversight: Senior compliance and risk leadership should be actively involved. Regulators expect clear accountability at leadership levels, with issues escalated and resolved transparently across governance structures.

To ensure monitoring is not only operational but defensible under scrutiny, many organizations turn to expert guidance, like Fraxtional, to integrate regulator-ready oversight.

How Fraxtional Supports Regulator-Ready Transaction Monitoring

Transaction monitoring is only as strong as the leadership, design, and accountability behind it. Effective systems don’t just generate alerts; they integrate risk, governance, documentation, and regulator alignment.

That’s where Fraxtional steps in, integrating seasoned compliance leadership into your business so your monitoring program is not just compliant on paper, but defensible.

Here’s how Fraxtional can help you build and maintain transaction monitoring that satisfies both regulators and sponsor banks:

- Compliance Leadership: Fraxtional provides experienced leaders (e.g., CCO, CAMLO, BSA Officer) who integrate seamlessly into your team, offering the judgment and oversight that automated tools alone cannot provide.

- Monitoring Framework Design and Review: Fraxtional works with you to design or refine your transaction monitoring logic, aligning rules, thresholds, and escalation flows to your specific risk profile. With clear and documented logic, your program becomes easier for regulators and sponsor banks to understand and trust.

- Sponsor Bank and Regulator Readiness: Sponsor banks and examiners evaluate monitoring as part of broader risk programs. Fraxtional’s guidance ensures that your monitoring aligns with expectations, especially when onboarding new partners or preparing for exams.

- Independent, Regulator-Aligned Perspective: Beyond internal reviews, Fraxtional offers independent audits and validation of your compliance program, a practice regulators increasingly expect. This objective viewpoint helps identify blind spots and strengthens confidence with stakeholders.

Also Read: The Rise of Fractional C-Suite Executives in Crypto

With the right expertise in place, companies can turn strong transaction monitoring into a strategic advantage rather than just a compliance obligation.

Final Thoughts

Understanding what is transaction monitoring goes far beyond knowing how alerts are generated. For regulators and sponsor banks, it is the clearest signal of whether you truly understand your risk as it changes in real time. Strong transaction monitoring connects customer behavior, business growth, and regulatory accountability into one defensible control.

This is where Fraxtional plays a critical role. By integrating compliance leadership into your organization, Fraxtional helps you design, review, and operate transaction monitoring programs that regulators and sponsor banks can trust. Fraxtional supports compliance maturity without the burden of full-time executive hires.

If you want to assess whether your transaction monitoring can stand up to regulatory or sponsor bank scrutiny, reach out to Fraxtional to speak with an experienced compliance leader and take the next step toward regulator-ready oversight.

FAQs

Yes. Under the Bank Secrecy Act, U.S. financial institutions are required to maintain systems reasonably designed to detect and report suspicious activity. While the law doesn’t prescribe exact tools, regulators expect effective transaction monitoring proportional to the institution’s size, products, and risk profile.

No. Regulators and sponsor banks expect transaction monitoring to be in place from early stages, even if volumes are low. Delaying implementation creates compliance debt and often becomes a blocker during sponsor bank onboarding, audits, or fundraising diligence.

There is no fixed timeline, but regulators expect rules to be reviewed whenever risk changes. This includes new products, new geographies, significant growth, or emerging typologies. Many mature programs review and tune rules at least quarterly or semi-annually.

Missing suspicious activity can lead to regulatory findings, enforcement actions, civil penalties, and strained sponsor bank relationships. Regulators focus not only on whether issues occurred, but also on whether your monitoring was reasonably designed and whether gaps were identified and corrected promptly.

Not always. Regulators care less about real-time versus batch processing and more about effectiveness. What matters is whether suspicious activity is detected, investigated, and reported in a timely manner based on the institution’s risk, transaction volume, and product complexity.

blogs

Don’t miss these

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.

Now Accepting:

BTC

ETH

USDC

USDP