Mar 9, 2026

ACH Rules and Nacha Audit Compliance Overview

By Fraxtional LLC

Summarize the blog with AI

The ACH Network has become one of the most critical payment rails in the United States, processing more than 33.6 billion payments valued at over $86.2 trillion in 2024, and that volume is still growing.

At the same time, payment fraud remains a reality. In 2024, nearly 79% of organizations attempted or successfully experienced payment fraud attacks, bringing our attention to the need for strong controls across all payment channels, including ACH.

For businesses, fintech firms, and financial institutions that rely on ACH, this means compliance is foundational to operational integrity.

In this blog, we’ll unpack how NACHA audits work, who must conduct them, what the core requirements entail, common compliance gaps, and what strong audit readiness actually looks like in practice.

Key Takeaways

- A NACHA audit is a mandatory annual review that confirms whether ACH operations comply with the NACHA Operating Rules in practice.

- The audit evaluates documented controls, governance oversight, and whether institutions can prove compliance through retained records and clear processes.

- Key areas reviewed include ACH authorizations, exposure limits, return rate thresholds, third-party oversight, IAT handling, and fraud monitoring controls.

- Many audit findings occur because of governance gaps such as outdated policies, undocumented reviews, or inconsistent compliance oversight.

- For organizations scaling ACH operations, Fraxtional provides fractional compliance leadership to strengthen governance frameworks, prepare for NACHA audits, and establish defensible oversight without hiring a full-time executive team.

What A Nacha Audit Actually Examines?

A Nacha audit is a formal evaluation of whether your institution is complying with the Nacha Operating Rules in practice, with supporting evidence.

Under the Rules, every Participating DFI must conduct an annual ACH compliance audit. That audit must assess adherence to the Operating Rules and confirm that internal audit controls are functioning as designed. For fintechs operating under sponsor banks, similar expectations are typically imposed contractually.

This means auditors are looking for documented controls, testable processes, and defensible oversight.

New NACHA Rules Impacting ACH Compliance

The 2026 NACHA rule amendments expand how ACH participants must manage fraud risk, transaction classification, and payment processing timelines.

These updates shift the focus from limited fraud detection controls to a network-wide risk management framework that requires documented monitoring processes and clearer transaction transparency.

Expanded Fraud Monitoring Requirements

One of the most significant changes is the expansion of fraud monitoring obligations across the ACH network.

Previously, fraud detection requirements applied mainly to certain WEB debit transactions and micro-entries, with little guidance on how monitoring systems should operate. The 2026 update introduces clearer expectations and applies them to a broader group of participants.

Under the new rule:

- All non-consumer Originators, ODFIs, TPSPs, and TPSs must implement risk-based fraud monitoring processes.

- Monitoring must address both debit and credit transactions, not just debits.

- Organizations must establish documented monitoring procedures using tools such as anomaly detection, velocity checks, and pattern recognition.

- Fraud monitoring programs must also be reviewed annually.

These changes reflect the growing threat of credit-push fraud, including scams involving social engineering, payroll diversion, and vendor impersonation.

Phased Implementation Timeline

NACHA is rolling out the fraud monitoring rules in two phases based on transaction volume.

Phase 1: March 20, 2026

Applies to:

- Originators with 6 million or more ACH originations in 2023

- Third-Party Service Providers (TPSPs)

- Third-Party Senders (TPSs)

During this phase:

- ODFIs must strengthen fraud monitoring programs.

- Large RDFIs must implement ACH credit monitoring controls.

Phase 2: June 22, 2026

The same monitoring requirements expand to all remaining Originators, ODFIs, TPSPs, TPSs, and RDFIs.

Updated Definition of International ACH Transactions (IAT)

The definition of International ACH Transactions (IAT) has been clarified.

An ACH transaction must now be classified as an IAT if any part of the payment flow involves a financial institution outside the United States, including intermediary institutions.

This clarification improves cross-border payment transparency and ensures proper OFAC screening and regulatory compliance.

If your organization is scaling ACH volume and needs stronger audit defensibility, structured governance, and documented compliance alignment with the Nacha Operating Rules, Fraxtional provides fractional compliance leadership to formalize oversight, strengthen documentation frameworks, and establish a disciplined operating cadence.

Who Must Conduct A Nacha Compliance Audit?

The audit must evaluate whether the institution’s ACH operations comply with the current Operating Rules and whether internal procedures align with how the institution actually processes entries.

How that responsibility applies varies depending on the role an entity plays within the ACH ecosystem:

To better understand how NACHA rules apply in practice, it helps to look at the types of transactions that move through the ACH network and fall under these regulatory standards.

What Types of Transactions Do NACHA Rules Cover?

NACHA rules govern payments that move through the Automated Clearing House (ACH) network, one of the primary systems used to transfer funds electronically in the United States.

Because ACH is widely used for both consumer and business payments, the rules apply to a broad range of transaction types. Here are some of the most common categories covered under the NACHA framework:

Once the range of ACH transactions covered by NACHA rules is clear, the focus shifts to how organizations prove compliance during a NACHA audit.

NACHA Audit Requirements And Checklist

At a minimum, the audit must confirm three things:

- Your ACH operations comply with applicable Nacha requirements.

- Controls are documented, tested, and functioning.

- Governance and oversight mechanisms are active and defensible.

Below is a structured breakdown of what the Rules require, how audits are expected to be conducted, and what documentation examiners typically request.

Annual Audit Requirement Under The Operating Rules

Each Participating DFI must complete an audit of its ACH activities at least once every calendar year.

The audit must:

- Be completed within the calendar year

- Address compliance with applicable Operating Rules

- Be documented in writing

- Identify any deficiencies

- Include corrective action tracking

Completion alone is not sufficient. Institutions must retain evidence that the audit occurred, what was reviewed, who performed it, and what findings were identified.

Failure to complete an annual audit is itself a rule violation, regardless of operational performance.

Independence And Audit Governance Standards

The Rules do not mandate a specific framework, but they do require objectivity.

The audit must be conducted by qualified personnel who are independent from daily ACH processing activities. This may include:

- An internal audit department

- A compliance function with structural independence

- An external independent examiner

Independence is evaluated based on reporting lines and decision-making authority. Personnel directly responsible for ACH file processing or monitoring should not audit their own work.

In institutions with formal governance structures, audit results should be reported to:

- Senior management

- Risk committees

- Audit committees

- The board, where applicable

Documentation of this reporting is part of defensible governance.

Required Audit Documentation And Record Retention

The audit must generate tangible records.

At minimum, institutions should maintain:

- Audit scope documentation

- Testing methodology and sampling rationale

- Identified findings

- Management responses

- Remediation timelines

- Final audit report

Industry practice commonly aligns audit file retention with broader compliance recordkeeping standards, often up to six years. While the Rules do not prescribe a specific number, regulators and sponsor banks frequently expect multi-year retention.

Institutions should be prepared to produce audit records upon request.

Data Security Validation Requirements

Where ACH participants store deposit account information electronically, enhanced data security standards apply.

Audits should confirm:

- Stored account data is rendered unreadable

- Encryption or tokenization controls are implemented

- Access permissions are restricted and reviewed

- Administrative privileges are monitored

- Security testing is performed periodically

For high-volume originators, third-party service providers, and fintech platforms, this area often receives elevated scrutiny.

The audit must validate that data protection measures are operational, not theoretical.

Third-Party And Outsourced Function Evidence

Outsourcing ACH functions does not eliminate audit responsibility.

Where ACH services are delegated to:

- Third-Party Service Providers

- Technology vendors

- Processing platforms

The institution must maintain evidence of oversight.

This typically includes:

- Contracts incorporating rule compliance obligations

- Independent audit reports, such as SOC examinations

- Ongoing monitoring documentation

- Issue remediation tracking

Auditors will expect to see proof that vendor controls are reviewed and evaluated on a recurring basis.

The following checklist summarizes the key documentation and control evidence institutions typically prepare during a NACHA compliance audit:

Even when institutions complete annual audits, recurring weaknesses continue to surface. Identifying these patterns provides practical insight into where compliance programs often fall short.

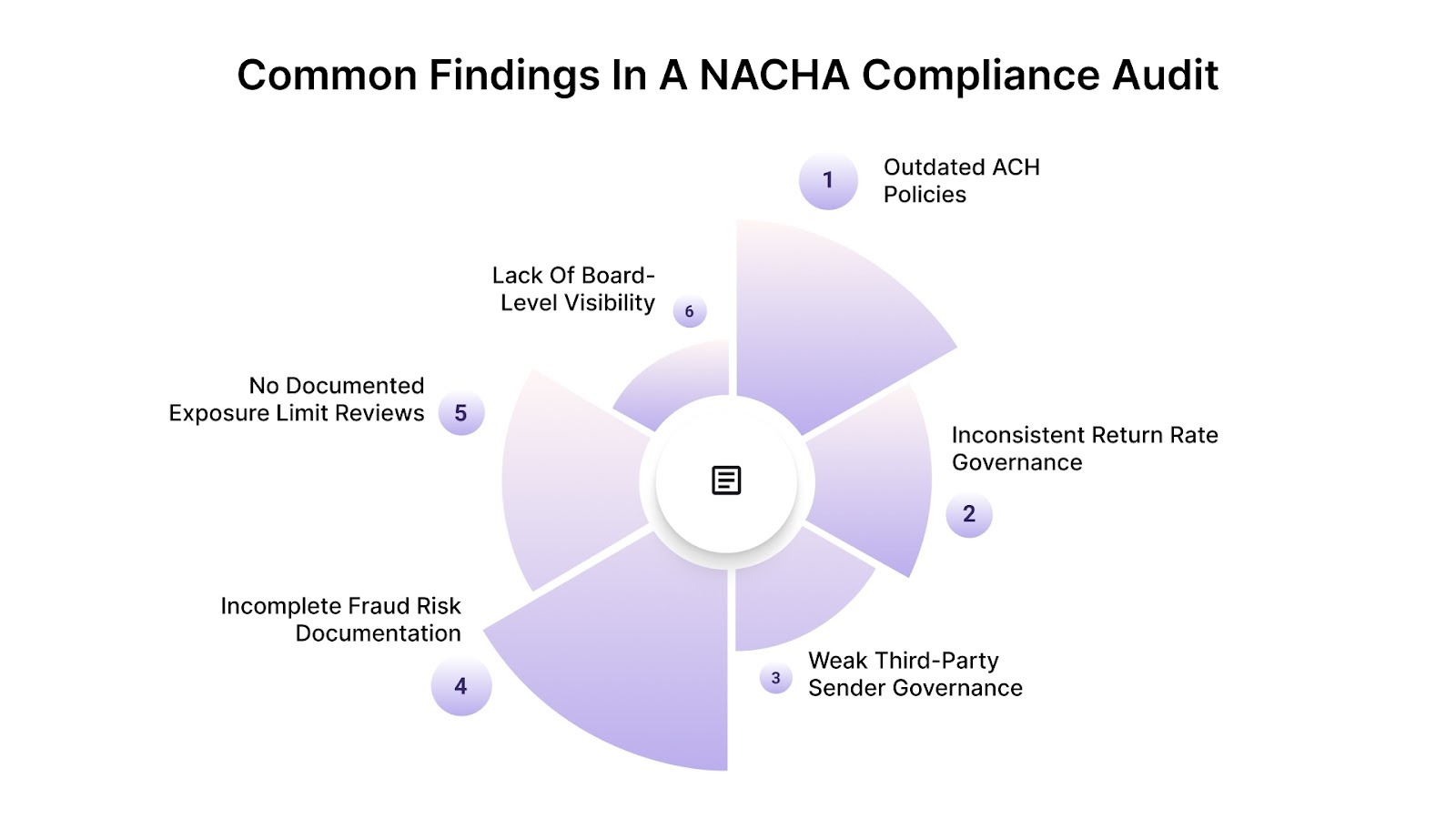

Common Findings In A NACHA Compliance Audit

Most NACHA audit findings are not caused by ignorance of the Rules. They stem from structural gaps between written intent, operational execution, and governance visibility.

Below are the weaknesses that frequently emerge and how to address them before they escalate.

Outdated ACH Policies

An outdated policy usually signals that compliance ownership is unclear.

This gap often appears when:

- Policies are reviewed reactively instead of on a defined cadence

- Rule updates are implemented operationally but not reflected in writing

- Policy approval history is inconsistent

Over time, this creates misalignment between operational teams and governance oversight.

How to reduce the risk: Establish a defined annual policy review cycle with named ownership. Maintain a revision log that captures what changed and why. Treat policy updates as a governance exercise, not an administrative task.

Inconsistent Return Rate Governance

Inconsistency in return monitoring reflects a breakdown in structured oversight. Data may exist, but escalation thresholds, trend analysis, and executive awareness may not be formalized.

This weakness often surfaces when:

- Monitoring depends on one individual rather than a defined process

- Reporting cadence shifts during busy periods

- No documented decision-making framework exists when metrics change

It signals operational fragility rather than noncompliance.

How to reduce the risk: Formalize ownership of monitoring metrics. Define reporting intervals, escalation triggers, and documentation standards. Monitoring should operate on a schedule, not discretion.

Weak Third-Party Sender Governance

This weakness typically indicates that risk management is decentralized. Business teams may onboard partners for speed, while compliance documentation lags behind.

It shows up when:

- Risk assessments are incomplete or outdated

- Contracts lack updated compliance language

- Oversight responsibilities are unclear

The underlying issue is governance fragmentation.

How to reduce the risk: Centralize third-party oversight under a structured framework. Assign accountability for onboarding documentation, periodic reviews, and remediation tracking. Vendor compliance should follow a calendar, not a crisis.

Incomplete Fraud Risk Documentation

Fraud controls may exist operationally, but without documented risk logic, they appear arbitrary. This gap often reflects informal decision-making.

It becomes visible when:

- Thresholds are set without written justification

- Risk categories are undefined

- Control intensity does not clearly match risk level

This weakens defensibility, even if controls are functioning.

How to reduce the risk: Document the reasoning behind fraud controls. Link risk categories to specific monitoring strategies. Update the assessment when transaction volume or business models change.

No Documented Exposure Limit Reviews

Exposure limits often get established during onboarding and then remain static. The weakness is not the limit itself, but the absence of periodic validation.

This usually appears when:

- Growth outpaces initial assumptions

- Limit reviews are informal conversations rather than documented approvals

- Credit or risk committees are not involved consistently

It signals a governance lag relative to business expansion.

How to reduce the risk: Institute a formal review cadence tied to transaction growth or revenue milestones. Document reaffirmations, not just changes. Stability should be evidenced, not assumed.

Lack Of Board-Level Visibility

When ACH oversight does not reach leadership, compliance becomes siloed. This creates strategic blind spots.

It often shows up as:

- No documented reporting of ACH risk metrics

- Audit findings handled operationally without executive review

- Remediation tracked internally but not escalated

The organization may be compliant operationally, yet governance appears weak.

How to reduce the risk: Integrate ACH risk summaries into regular executive or board reporting. Even a concise dashboard with key indicators reinforces accountability and demonstrates oversight maturity.

These weaknesses share a common theme: compliance processes exist, but they are not structured, documented, or governed at a leadership level.

Let’s now explore how Fraxtional’s expertise can assist your organization through the procedure and ensure further compliance.

Strengthen Your NACHA Audit Readiness With Fractional Compliance Leadership

Passing a NACHA audit is not about scrambling before year-end. It is about building a compliance structure that stands up to scrutiny every day of the year.

That requires leadership, not just policies.

Fraxtional works with fintech companies, sponsor banks, and financial institutions that need executive-level compliance oversight without committing to a full-time hire. Instead of reacting to audit findings, you build a defensible program from the top down.

Here’s how Fraxtional supports ACH compliance maturity:

- Fractional Executive Oversight: Gain access to experienced compliance leaders such as CCOs, CROs, and AML specialists who provide strategic direction, governance structure, and audit accountability on a flexible basis.

- Audit Readiness And Mock Reviews: Identify documentation gaps, governance weaknesses, and structural risks before they become formal findings. Fraxtional helps you operationalize compliance expectations into measurable controls.

- Sponsor Bank And Board-Level Alignment: Ensure reporting, oversight, and remediation processes are structured in a way that strengthens sponsor bank confidence and satisfies board governance expectations.

- Ongoing Regulatory Infrastructure: Build scalable compliance frameworks that evolve with transaction growth, new product lines, and increased regulatory scrutiny.

A NACHA audit should validate your structure.

If your organization needs compliance leadership without expanding executive payroll, fractional support can provide the governance discipline required to operate confidently in the ACH ecosystem.

Final Thoughts

ACH now sits at the center of how businesses move money. With trillions flowing through the network each year, even small control gaps carry real consequences. A NACHA audit tests whether your governance structure can hold up under scrutiny.

Organizations that treat ACH compliance as an annual task often react to findings instead of preventing them. Strong programs build leadership accountability, document decisions, and formalize oversight at the executive level.

If you need seasoned compliance leadership without hiring a full-time executive, Fraxtional provides fractional CCO, CRO, and AML expertise to strengthen governance, documentation, and reporting. The goal is simple: ensure your next NACHA audit confirms control, not exposes gaps. Let's talk!

FAQs

Yes. Sponsor banks often impose enhanced compliance and documentation requirements that go beyond the minimum NACHA Operating Rules, especially for fintech partners operating at scale.

No. NACHA does not mandate a particular audit framework. However, institutions may align their methodology with established internal audit standards to ensure objectivity and defensibility.

Institutions should document a formal remediation plan with defined ownership, timelines, and interim risk controls. Transparent tracking is often more important than immediate closure.

Fintechs are typically reviewed through their sponsoring ODFI. However, contractual agreements often require fintechs to maintain audit-ready controls that mirror NACHA standards.

Rapid growth increases scrutiny around exposure governance, monitoring cadence, and documentation maturity. Controls that worked at lower volumes may require recalibration as scale increases.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.