Mar 9, 2026

NACHA Violations: Risks, Penalties, and Prevention

By Fraxtional LLC

Summarize the blog with AI

What happens when your ACH return rates quietly cross NACHA thresholds and your sponsor bank notices before you do?

For fintech companies and payment processors, a NACHA violation is not just a technical error. It can trigger fines, mandatory corrective action, increased bank scrutiny, and reputational damage that extends beyond operations.

As ACH volumes scale across digital lending, embedded finance, payroll, and subscription platforms, compliance oversight becomes critical. Understanding what constitutes a NACHA violation and how to prevent one is essential for protecting your payment infrastructure and banking relationships.

Overview

- A NACHA violation typically arises when unauthorized, administrative, or overall ACH return rates exceed established thresholds under the NACHA Operating Rules.

- Enforcement can escalate through the National System of Fines, with egregious Class 3 violations carrying penalties of up to $500,000 per occurrence and possible suspension directives.

- Repeated violations can trigger corrective action plans, intensified sponsor bank oversight, and broader regulatory scrutiny.

- Effective prevention requires structured authorization controls, real-time return monitoring, formal ACH risk assessments, and executive-level accountability.

- Fractional compliance leadership can strengthen ACH governance and reduce escalation risk without requiring a full-time executive hire.

What Constitutes a NACHA Violation Under the Operating Rules?

A NACHA violation occurs when a participant in the ACH Network fails to comply with the NACHA Operating Rules. These rules govern how ACH transactions are originated, authorized, processed, and returned.

Violations commonly relate to return rate thresholds. NACHA sets limits for:

- Unauthorized return rate (e.g., transactions returned as unauthorized by consumers)

- Administrative return rate (e.g., incorrect account number, closed account)

- Overall return rate

Exceeding these thresholds can trigger enforcement under NACHA’s National System of Fines. Enforcement may involve warnings, monitoring, and escalating financial penalties.

Additionally, violations may arise from improper authorization practices, weak data security controls, or failure to comply with rule updates. Depository Financial Institutions (ODFIs and RDFIs) play a central role in reporting and correcting violations, often within strict timeframes.

Understanding the technical definition is only the starting point. To manage risk effectively, it is equally important to examine why these violations occur, particularly in high-growth fintech environments.

Why NACHA Violations Occur in Fintech and High-Growth Payment Programs

NACHA violations rarely stem from a single processing error. In most fintech environments, they reflect structural weaknesses in ACH oversight, authorization controls, and compliance governance. As transaction volumes increase, small gaps in monitoring or accountability can escalate quickly.

Several recurring issues tend to drive threshold breaches:

- Excessive Unauthorized Returns: Often caused by unclear consumer consent processes, weak identity verification, or aggressive payment retry logic. When authorization controls are insufficient, unauthorized return rates rise rapidly.

- High Administrative Return Rates: Triggered by inaccurate account details, insufficient onboarding verification, or weak file validation processes.

- Rapid Transaction Growth Without Scaled Monitoring: When ACH volumes expand faster than compliance infrastructure, monitoring frameworks may lag behind operational growth.

- Fragmented Compliance Ownership: Operations teams track returns, product teams manage customer experience, and compliance oversight remains reactive. Without centralized accountability, breaches may go unnoticed until sponsor banks intervene.

These issues are operational on the surface, but they often signal deeper governance gaps, which is why understanding the regulatory and banking consequences of a NACHA violation is critical.

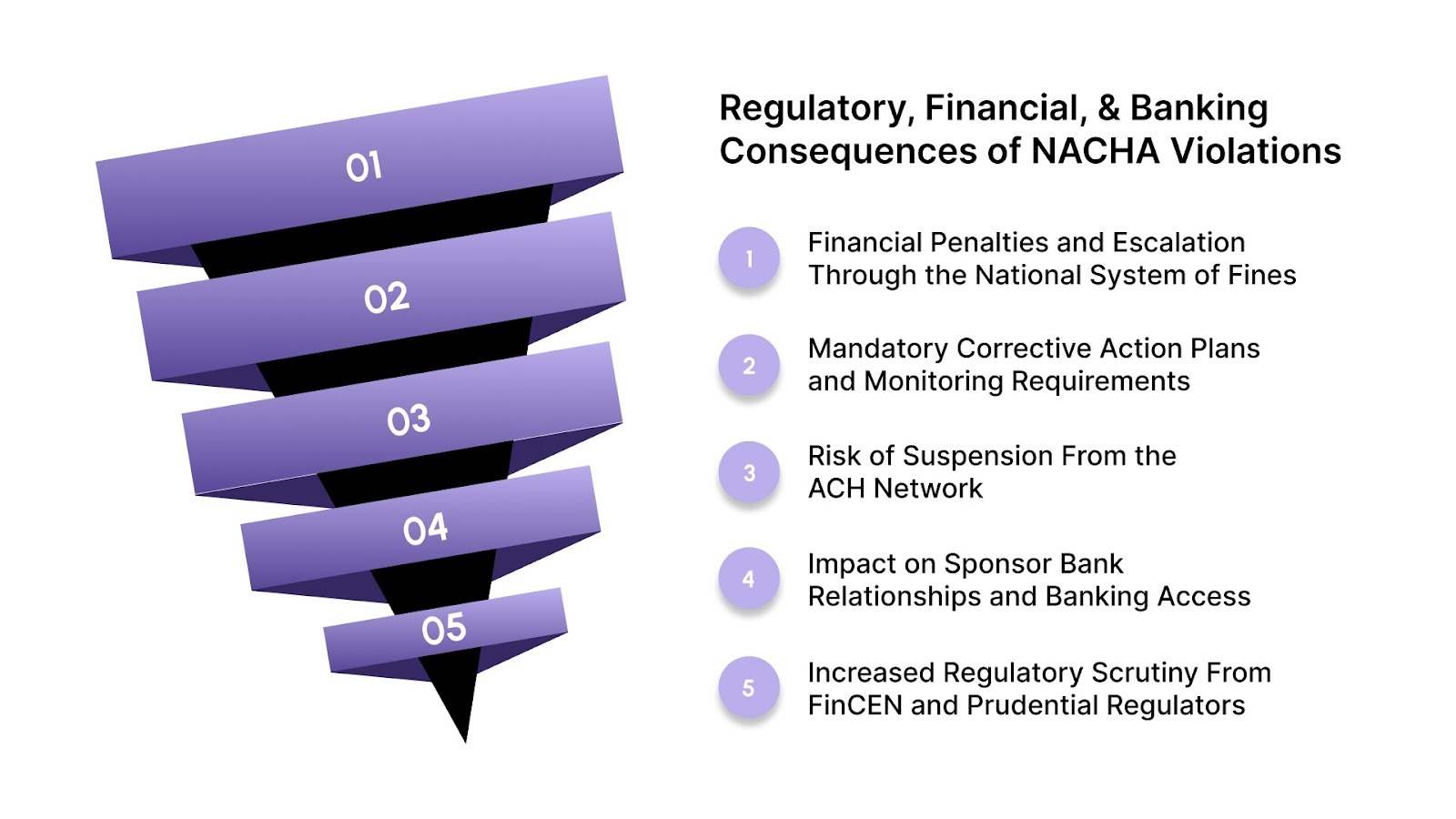

Regulatory, Financial, and Banking Consequences of NACHA Violations

A NACHA violation can escalate quickly depending on severity and scale. Under the National System of Fines and updated enforcement rules, violations are categorized and sanctioned based on impact and intent.

Understanding how enforcement escalates is critical for fintech leaders managing ACH exposure.

1. Financial Penalties and Escalation Through the National System of Fines

NACHA classifies violations into tiers, with more serious infractions resulting in stronger sanctions.

A violation may be considered “egregious” if it:

- Involves a willful or reckless action, and

- Affects at least 500 ACH entries, or

- Involves multiple entries totalling at least $500,000 in aggregate

The ACH Rules Enforcement Panel determines whether a violation qualifies as egregious and whether it should be categorized as a Class 2 or Class 3 violation.

For Class 3 violations, sanctions may include:

- Financial penalties of up to $500,000 per occurrence

- A directive requiring the ODFI to suspend the Originator or Third-Party Sender

- Formal reporting of the violation to ACH Operators and industry regulators

At this level, the issue is no longer operational; it becomes a material compliance event.

Escalation through these categories signals to banking partners that governance controls may require structural remediation.

2. Mandatory Corrective Action Plans and Monitoring Requirements

Even before violations reach egregious classification, NACHA may require:

- Formal corrective action plans

- Documented root cause analysis

- Ongoing reporting and monitoring

- Demonstrated reduction in return thresholds

Sponsor banks typically monitor remediation efforts closely. Failure to demonstrate measurable improvement can result in increased oversight or contractual restrictions.

Corrective oversight becomes significantly more complex if compliance ownership is unclear or fragmented.

3. Risk of Suspension From the ACH Network

For severe or repeated Class 3 violations, NACHA may direct an ODFI to suspend an Originator or Third-Party Sender from originating ACH transactions.

For fintech companies reliant on ACH processing, suspension could:

- Interrupt customer payments

- Disrupt lending or payroll flows

- Impact revenue continuity

- Damage investor confidence

While such enforcement is reserved for serious cases, the operational impact can be substantial.

This level of risk makes proactive governance far more effective than reactive remediation.

As ACH volumes grow, structured compliance leadership becomes essential. Fraxtional provides CCO and CRO oversight to help fintech and financial institutions strengthen ACH governance and monitor return rate risks. This leadership support helps identify compliance gaps early and reduce the likelihood of NACHA enforcement escalation.

4. Impact on Sponsor Bank Relationships and Banking Access

Sponsor banks are accountable for the ACH activity of fintech originators. When return thresholds are breached or violations escalate, banks may:

- Increase transaction-level monitoring

- Require independent compliance reviews

- Impose transaction limits

- Reconsider the relationship entirely

In practice, repeated violations often trigger bank-level risk reviews long before NACHA enforcement reaches its highest tier.

Strong ACH governance, therefore protects both compliance posture and long-term banking access.

5. Increased Regulatory Scrutiny From FinCEN and Prudential Regulators

Class 3 violations may be reported to ACH Operators and industry regulators. This expands visibility beyond NACHA enforcement alone.

Persistent violations may raise broader questions regarding:

- Risk management maturity

- BSA/AML oversight

- Consumer authorization practices

- Executive compliance accountability

For growth-stage fintechs preparing for audits, fundraising, or regulatory exams, these signals can delay strategic milestones and increase due diligence scrutiny.

Because the consequences extend well beyond financial penalties, effective prevention requires structured executive oversight, not just threshold monitoring.

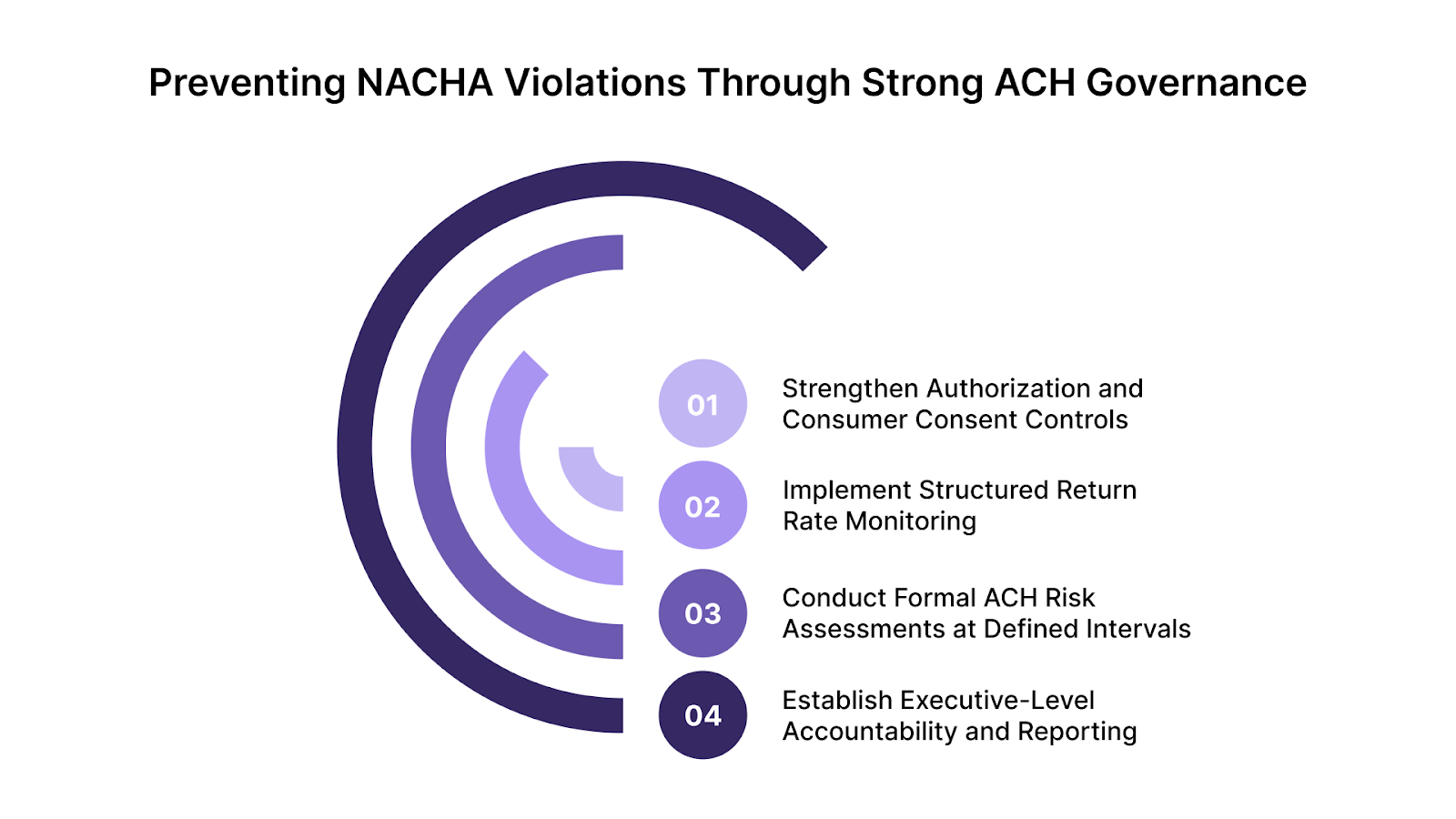

How to Prevent NACHA Violations Through Strong ACH Governance

Preventing NACHA violations requires more than monitoring return rates. It requires structured controls across authorization, monitoring, risk assessment, and executive accountability.

Below is a governance-driven prevention framework:

1. Strengthen Authorization and Consumer Consent Controls

Unauthorized return rates are one of the most common triggers of NACHA violations. Prevention begins at origination.

Key control measures include:

- Clear and documented consumer authorization language

- Retention of authorization records in accordance with NACHA requirements

- Strong identity verification procedures before initiating debits

- Controlled retry logic to prevent excessive resubmissions

- Periodic internal audits of authorization documentation

When authorization controls are defensible and well-documented, organizations reduce exposure during sponsor bank reviews or enforcement inquiries.

2. Implement Structured Return Rate Monitoring and Escalation Protocols

Monitoring must be continuous and threshold-based, not retrospective.

Effective oversight includes:

- Tracking unauthorized, administrative, and overall return rates against NACHA limits

- Setting internal alert triggers below NACHA maximum thresholds

- Assigning a compliance owner responsible for monitoring

- Establishing formal escalation procedures when thresholds approach risk levels

- Documenting corrective actions taken

Monitoring without defined escalation often results in delayed remediation. Clear ownership and response timelines prevent threshold breaches from compounding.

3. Conduct Formal ACH Risk Assessments at Defined Intervals

ACH risk assessments should not occur only after violations. They should be proactive and scheduled.

A structured ACH risk review typically evaluates:

- Customer onboarding controls

- Authorization practices

- File validation and formatting controls

- Vendor or Third-Party Sender oversight

- Return trend analysis

- Governance and reporting structures

Regular risk assessments demonstrate maturity to sponsor banks and regulators, particularly during audits or licensing reviews.

4. Establish Executive-Level Accountability and Reporting

ACH compliance should be integrated into broader risk governance.

Strong oversight includes:

- Periodic ACH return reporting to executive leadership

- Defined compliance ownership (CCO, CRO, or equivalent)

- Board-level visibility for material threshold trends

- Documented policies for corrective action implementation

- Clear coordination between operations, compliance, and risk functions

When ACH oversight remains siloed within operations, governance gaps emerge. Executive accountability reduces the likelihood that violations escalate unnoticed.

For growth-stage fintech companies, establishing this level of oversight may require structured compliance leadership support.

Strengthening ACH Compliance With Fraxtional Risk and Compliance Leadership

Fraxtional is a global provider of fractional risk and compliance services serving fintech companies, crypto platforms, banks, and private equity firms. The firm delivers senior-level compliance leadership without requiring companies to hire full-time executives.

Its model is designed to help regulated financial businesses strengthen governance while scaling responsibly.

- Fractional Chief Compliance Officer (CCO) and Chief Risk Officer (CRO) leadership to oversee ACH governance, manage return rate thresholds, and integrate ACH exposure into enterprise-wide risk management frameworks while maintaining regulatory alignment.

- AML and BSA compliance oversight aligned with broader financial crime controls.

- Compliance framework development and policy design tailored to fintech and payment operations.

- Regulatory readiness and licensing support, including preparation for sponsor bank reviews.

- SOC 2 readiness and audit coordination to strengthen internal control environments.

- Independent compliance program assessments to identify structural gaps before enforcement escalates.

By embedding experienced compliance leadership into growing organizations, Fraxtional helps fintech companies move from reactive monitoring to structured governance.

Wrapping Up

NACHA violations signal weaknesses in authorization controls, return monitoring, and governance oversight. Left unaddressed, they can escalate into fines, corrective action plans, and sponsor bank scrutiny. Strong ACH governance is essential to protect payment stability and banking relationships.

Fraxtional provides fractional compliance and risk leadership to fintech, crypto, and financial institutions managing ACH exposure. By embedding experienced CCO and CRO oversight, the firm strengthens governance without requiring a full-time executive hire.

If your ACH program needs structured compliance leadership, contact Fraxtional to reduce risk before violations escalate.

FAQs

NACHA does not publish a public database of violations. However, enforcement history may remain part of internal compliance records and sponsor bank oversight reviews. Repeated violations over time can influence future monitoring and risk evaluations.

No. Individual ACH returns are common in payment processing. A violation typically occurs when return rates exceed NACHA thresholds or when rules are breached in a material or repeated manner.

Organizations should immediately conduct a root cause analysis, document corrective measures, and engage their sponsor bank proactively. Timely remediation and clear communication often prevent escalation to higher enforcement levels.

NACHA enforcement actions are generally directed at participating financial institutions and originators. However, significant compliance failures may lead to internal accountability reviews at the executive level.

Not necessarily. NACHA enforcement typically follows a structured process that may begin with warnings or corrective action requirements. Persistent or egregious breaches are more likely to result in financial penalties.

blogs

Don’t miss these

.jpg)

Let’s Get Started

Ready to Strengthen Your Compliance Program?

Take the next step towards expert compliance solutions. Connect with us today.